Asia week ahead: Easing to intensify

- 12 March 2020

Central bank meetings dominate next week’s economic calendar in Asia. China has stepped forward with a targeted RRR rate cut, the real question for others is not whether they will cut rates again, but by how much

China: A rate cut is on the way

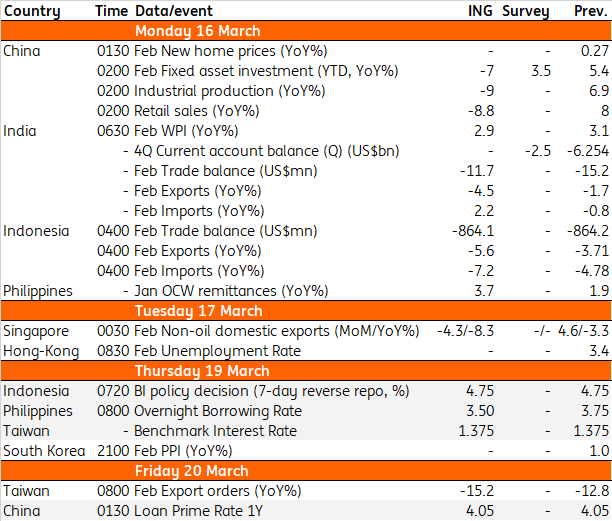

The next batch of Chinese data on industrial production, investment, retail sales and home prices will continue to be scrutinised for the economic impact of Covid-19 in the first two months of 2020. So far, the majority of economic releases have surprised on the downside and we don't think the ones coming up will be any different. But having said that, they should be more reflective of GDP growth in the first quarter. Industrial production growth is a good guide to real GDP growth and the consensus expectation of a record 3% YoY manufacturing contraction in the first two months foreshadows the worst.

The targeted RRR cut on Friday should put enough downward pressure on the interest rate, effectively reducing the chance of another rate cut in March, and banks’ interest rates for inclusive finance should be lower than lending to bigger corporates. We still think an interest rate cut is coming, though perhaps deferred to April. In total, we expect a 10 basis point cut in 7D reverse repo, 1-year medium lending facility and 1-year loan prime rate in April.

Given that cheaper bank loans do little to alleviate the damage from the coronavirus impact, we believe fiscal stimulus is the way to go.

* Updated on 13/03/20 to reflect recent PBOC moves

China: Where GDP growth is headed (%, year-on-year, quarterly data)

Intensifying central bank easing elsewhere

Elsewhere in the region, central bank meetings dominate the economic calendar. The question isn't really if they will cut rates, it's really all about by how much?

The Bank of Japan meeting will be interesting after the $10 billion fiscal stimulus by the government this week. Years of easing with negative policy interest rates have done little to revive demand and reach the 2% inflation goal. Being virtually out of policy ammunition, it’s an ongoing struggle to design effective policy moves, especially in these circumstances.

Central banks in Taiwan, Indonesia and the Philippines also meet next week. We expect all of them to be leaning towards policy easing, though our house forecasts suggest such action only by the Philippines central bank and that too by 25bp. We won’t be surprised if Indonesia's and Taiwan's central bank join the easing bandwagon and cut rates by more than 25bp.

What else? More trade data

February trade figures are due in India, Indonesia, Japan and Singapore. While these will be scrutinised for the trade impact of the virus, we won’t see the full impact just yet given the pandemic began its rapid spread outside China in late February.

Already released trade data for the month elsewhere in Asia (China, Korea, and Taiwan) is so far a mixed bag. Looking at average export growth in January and February, China’s 17% YoY export fall was worse than expected and it compares with 1.3% fall in Korea’s exports, while Taiwan’s rose by 6.5% in the same months.

We expect the forthcoming data to unfold on a softer side.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles