Asia week ahead: Central banks decide on policy next week

- 18 May 2023

- Asia week ahead China Indonesia

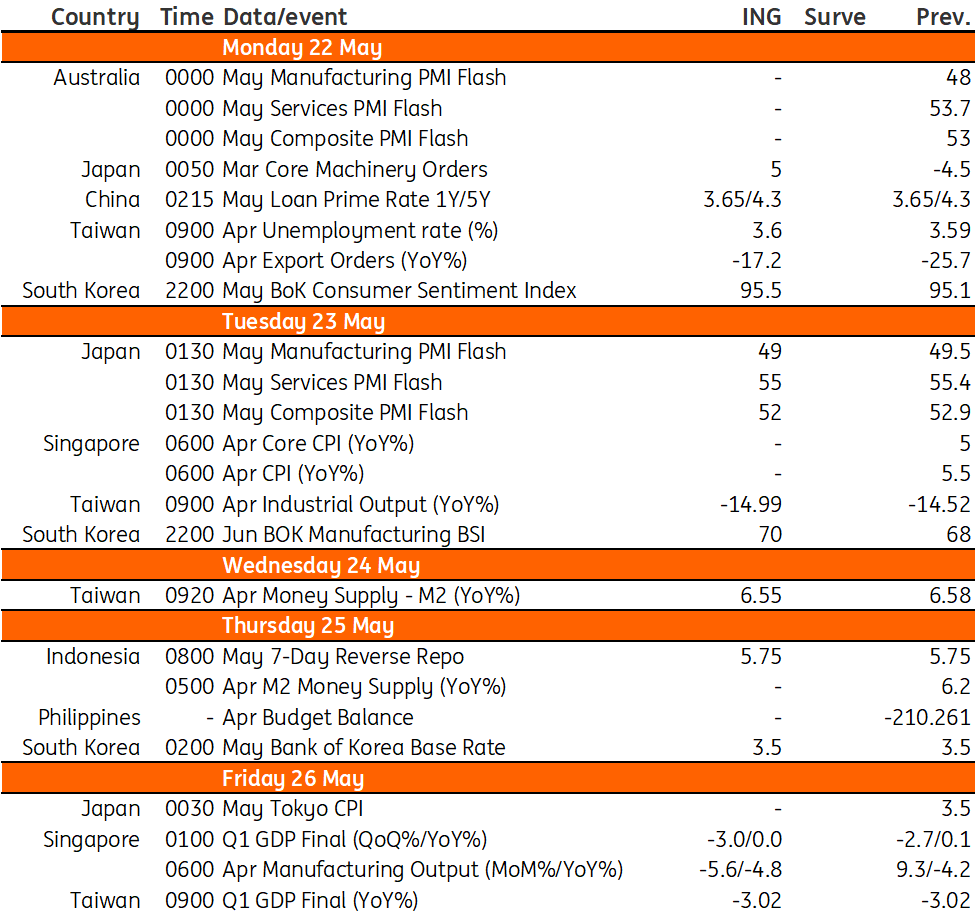

Next week’s data calendar features policy rate decisions from Korea and Indonesia plus key data from Taiwan and Singapore

Service led growth to remain robust in Japan

Flash PMI and core machinery orders data will confirm that service-led growth is continuing in Japan despite weak manufacturing activity. This trend should also be reflected in prices, with core inflation excluding food and energy rising faster than headline inflation.

Sentiment to remain sluggish in Korea

Consumer and business surveys are expected to show that sentiment has improved from the recent dip, but overall sentiment indices should remain sluggish. Meanwhile, the Bank of Korea will meet next Thursday but no action is expected as inflation continues to slow.

Chinese banks to keep Loan Prime Rates unchanged

Chinese banks should decide to maintain both the 1Y and 5Y Loan Prime Rates on Monday, which are currently at 3.65% and 4.3%, respectively. We expect banks to hold because the People's Bank of China (PBoC) has opted to maintain policy rates. The PBoC has also said that we could see higher CPI inflation in the near term.

Weak demand for semiconductor chips to weigh on Taiwan’s economy

Taiwan export orders and industrial production should show a more than 10% year-on-year contraction in April given the still weak demand for semiconductor chips. The current situation might not improve materially until demand for new models of US smartphones exceeds current production expectations. This is quite unlikely as the US economy is weakening.

Bank Indonesia set to extend pause

Bank Indonesia will likely keep policy rates untouched next week. Fading price pressures have allowed the central bank to extend its pause, keeping rates at 5.75% since January. Renewed pressure on the Indonesian rupiah, however, could mean that the central bank will need to hold off on rate hikes for now to ensure FX stability.

Soft industrial production in Singapore

Industrial production will be reported next week, and we expect sluggish exports to weigh on output for at least another month. Industrial production has largely tracked the downturn in non-oil domestic exports and the sustained slump for electronics and petrochemicals should result in another month of soft industrial production as well.

Key events in Asia next week

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles