Asia week ahead: New month, new week, new risks

- 28 May 2020

There will be plenty of economic data next week to mull over and scrutinise as to which Asian economy responded best to the Covid-19 crisis. But US-China tensions will continue to rule market sentiment as the new trading month kicks off

From policy to reality

Economic policies have been dominating headlines since the start of China’s 'two sessions' last week bringing in some fresh stimulus for the economy. This was followed by a spike in US-China tensions over Hong Kong's autonomy and potential sanctions against the territory. Singapore also stepped up its Covid-19 stimulus with the fourth package to preserve jobs, and the Bank of Korea went on with another policy rate cut.

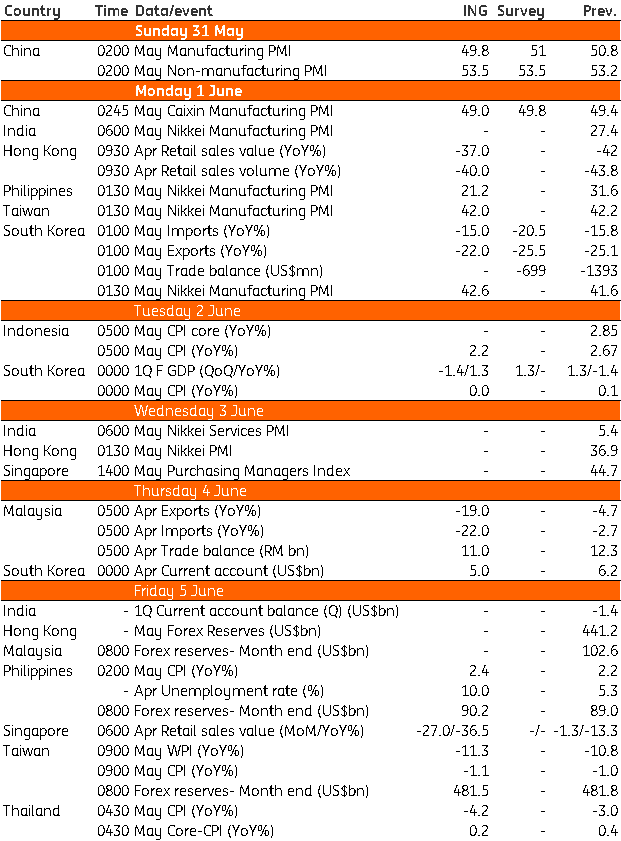

Setting the tone for markets next week will be China's purchasing managers index for May arriving over the weekend

The US-China row will continue to rule market sentiment next week, but there is plenty of data in the pipeline for investors to mull over and analyse how regional economies have been coping with Covid-19 restrictions.

Setting the tone for markets next week will be China's purchasing managers index for May arriving over the weekend (31 May) and the consensus expects a slight rise in manufacturing and non-manufacturing PMIs, which should be positive for markets. Likewise, PMIs from the rest of the region should show some recovery from their record lows in April. After all, PMIs are soft data, subject to respondents’ sentiment at the time of the survey, and surprises on either side are likely.

Hard data like exports, retail sales and inflation should help to assess the real impact, and, there are lots of those on the calendar next week. Korea’s trade figures for May are out on 1 June - the first trade numbers for the month from the region and probably the world should serve as a leading indicator of global demand. We expect a continued steep fall in exports in excess of 20% YoY. We aren’t alone; that’s also the consensus view.

Korea’s trade figures for May are out on 1 June - the first trade numbers for the month from the region and probably the world should serve as a leading indicator of global demand

April retail sales from Hong Kong and Singapore will be interesting for what they say about domestic consumption in the month when the Covid-19 restrictions were at their tightest ever. We anticipate the worse, as much as a 37% plunge in sales from a year ago, led largely by non-essential buying. A surge in online sales may have picked up some slack but it’s unlikely to come as any meaningful support in an environment of depressed economic confidence. Online sales in Singapore gained some traction in recent months, though at 8.5% of total sales in March, they are far too small.

Weak demand should be further reflected by falling inflation. We are seeing steeper fall in CPI inflation in most countries reporting May data next week (Korea, Taiwan, Indonesia, Philippines, and Thailand). Thailand has been leading the way down with a further fall from -3.0% YoY in April to -4.2% in May.

Anything on the policy side?

The next policy event in the pipeline is the Reserve Bank of Australia’s policy decision, but it will likely pass as a non-event. With the worst of Australia's Covid-19 spread behind us, the economy should be on a recovery path. We see the RBA keeping its policy rate unchanged at 0.25%, which is already the lowest it has ever been.

With a record stimulus already released, we think fiscal and monetary policies around the region and globally have nearly reached their limits. All that seems to be left now is the wait for the disease to die its own death and confidence to return before the unprecedented policy loosening starts to bear fruits.

This means increasing attention on economic activity data in the weeks and months ahead for signs of bottoming of the downturn.

Asia Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Our view on next week’s key events

- This bundle contains 3 Articles