Asia week ahead: Gleaning the trade impact

- 6 March 2020

- Asia week ahead

The plummeting Chinese PMIs don't bode for well for hard activity indicators out next week. Trade figures from several Asian countries should provide a glimpse of the pain Covid-19 is inflicting. Things are likely to get worse before they get better

China

A sharp plunge in China’s manufacturing and non-manufacturing purchasing manager indexes in February means hard activity data is set to reveal the impact of Covid-19 on the economy starting with trade figures over the weekend, followed by inflation and monetary indicators over the course of next week.

We agree with the consensus of a double-digit trade contraction in the first two months of the year in comparison to the same period last year, and inflation above 5%. Meanwhile, market expectations of a sharp slowdown in new yuan loans and aggregate financing in February stems from virtually stalled economic activity, though we're not ruling out the risk of these indicators surprising on the upside as a result of the recent monetary stimulus.

The rate of new infections is abating and factories are gradually re-opening, which is good news for the economy. However, markets are unlikely to relax just yet, as the data might show recent exceptional weakness in economic activity persists for months before it gets better.

Taiwan, Korea, Malaysia and India

Trade reports also are due in Taiwan and the Philippines, while Korea releases its jobs report and Malaysia its manufacturing data – all will be under scrutiny for the Covid-19 impact. However, data may not provide a good sense of the impact as the epidemic rapidly began to spread beyond China only in the second half of February.

Lastly, India’s elevated consumer price inflation above 7% will continue to be the main headwind for central bank easing amid the rising threat of the virus to GDP growth. Making matters worse is the latest acceleration currency depreciation, which saw the Indian rupee weakening above 74 against the US dollar this week.

It’s going to be a challenge for Governor Shaktikanta Das as he struck a dovish chord after the Fed's surprise rate cut.

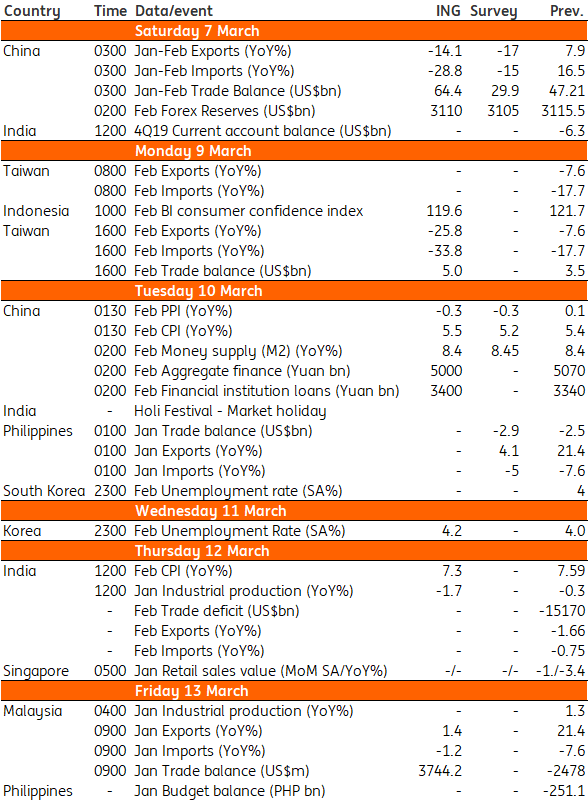

Asia Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 9 March 2020

- This bundle contains 7 Articles