Asia week ahead: A big data pipeline

- 6 May 2020

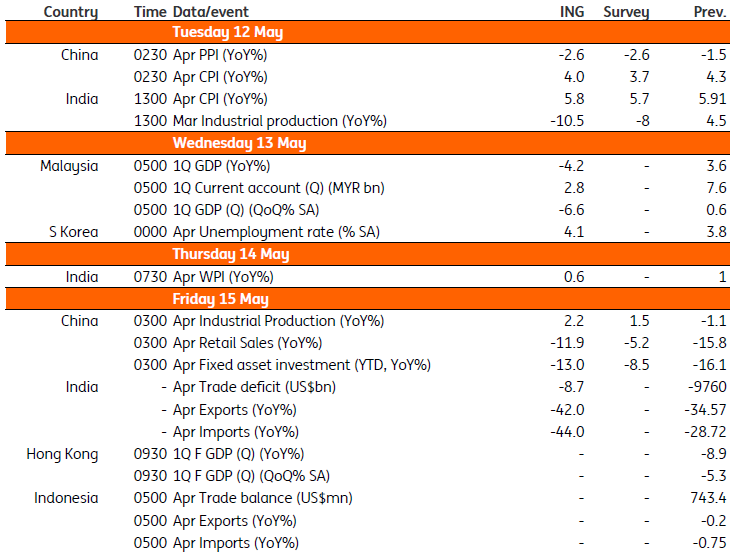

- Asia week ahead

Economic releases from China and India crowd the Asian calendar, as India heads for its worst economic slump while Malaysia's 1Q20 GDP report card is set to show a contraction of more than 4%. But noise about the origin of the Covid-19 virus and a potential tariff war may become the dominating theme

China: Has the slowdown troughed?

China’s monthly data for April will continue to dominate the headlines. We got PMI data last week, followed by trade figures this week. Next week will see inflation (CPI and PPI), monetary (aggregate finance, new loans, and M2), and real economic monetary indicators - industrial production, fixed assets investment, and retail sales.

The forthcoming data may shed light on the post-Covid-19 economic recovery coming into the second quarter. However, before we even think of recovery, we don’t know if we are at the trough. Maybe not yet, with global demand destruction weighing on exports and caution exercised on domestic spending throughout most of this year. That said, our Greater China Economist, Iris Pang, is hopeful of industrial production returning to growth and investment and retail sales posting moderate declines in April compared to March.

More than data though, noise about the origin of the Covid-19 virus and a potential resumption of the tariff war may remain the dominating theme for markets.

India headed for worst economic slump

China may have passed the worst of its Covid-19 outbreak but India is still suffering and the economy is already feeling the pain if the single-digit composite PMI in April are anything to go by, which according to the data compiler (IHS Markit) corresponds to an annual 15% GDP contraction. All seems to be coming crashing down except inflation, as the data should show next week.

No points for guessing that a 35% YoY plunge in exports in March coupled with weak domestic demand was associated with the sharp fall in output. We forecast over 10% YoY fall in industrial production in March. But it's going to be much worse in April based on our forecast of over 40% export fall that month.

And, consumer prices are likely to show persistently high inflation, close to the top end of the Reserve Bank of India’s 2-6% policy target. As I gather from my conversation with friends and relatives in India, all are feeling the pinch of supply shortages and food items are becoming acutely expensive.

The bottom line is that India is headed for its worst economic slump ahead.

Malaysia's GDP to contract by more than 4%

Malaysia’s 1Q20 GDP report arrives next Wednesday on 13 May. It won't be pretty as can be gauged from Bank Negara Malaysia’s double-barrel, 50 basis point rate cut this week. We estimate over 4% YoY GDP contraction - a sharp swing from 3.6% growth in the previous quarter and the worst since the global financial crisis.

Malaysia's had a turbulent few months. First, the political turmoil overthrowing the Mahathir Muhammad government in late February depressed economic confidence. Just as the Muhyiddin administration assumed power, Covid-19 movement restrictions in mid-March came into play stalling economic activity for the remainder of the quarter. Even so, exports and manufacturing held ground with almost flat growth over a year ago. But, services including retail, transport, tourism, etc. took a strong beating. On the spending side, it’s an across-the-board weakness in all GDP components including consumption, investment, and net trade.

Of course, the 1Q data doesn't capture the full impact of the pandemic. That's for the current quarter when the additional hit from a slump in the global oil prices to the net oil exporter economy will cause a much steeper GDP fall. This is why we have added another 50bp rate cut to our forecast in this cycle.

Key events

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Good MornING Asia - 8 May 2020

- This bundle contains 8 Articles