Asia week ahead: 3Q GDP season kicks off

- 15 October 2020

- Asia week ahead

China GDP numbers will be the highlight next week but we'll also be keeping an eye out for trade numbers from Japan and Thailand to see if they confirm the export-led recovery story

China 3Q report card

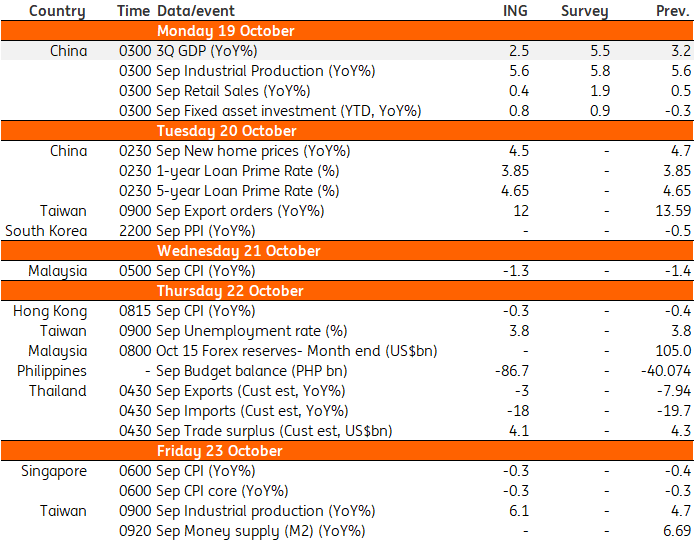

China’s 3Q20 GDP report will be the highlight of next week. GDP will be out on Monday alongside September activity data on industrial production, retail sales, fixed-asset investment. The Peoples Bank of China also reviews its one- and five-year loan prime rates next week.

Higher manufacturing PMI in September heralded firmer industrial production, while strong industrial profits growth in recent months likely pulled fixed-asset investment growth back into positive territory in September. A surge in spending ahead of the long National Day holiday and the government’s drive to promote cross-provincial tourism should support retail sales too. While there was ample banking sector liquidity supporting the domestic economic activity, external demand also continued to improve, as data earlier this week showed.

All this suggests that the third-quarter GDP performance should be better than that of the second quarter, imparting upside risk to our house forecast of 2.5% YoY GDP growth in the last quarter (3.2% in 2Q). We don’t see any reason why the PBOC should alter the current monetary policy setting.

Export-led recovery

September CPI inflation and external trade figures crowd the calendar for the rest of the region. We don’t think anybody cares about inflation, which has been negative or close to zero in much of the region, especially in the reporting countries next week -- Japan, Hong Kong, Malaysia and Singapore.

Japan and Thailand will release trade figures for September. We take a cue from firmer exports elsewhere in the region and look for the same in these two countries, though their export growths are yet to turn the corner into positive territory.

Taiwan’s export orders will be a key indicator of electronics-led recovery coming into the final quarter of the year.

Asia Economic Calendar

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Our view on next week’s events

- This bundle contains 3 Articles