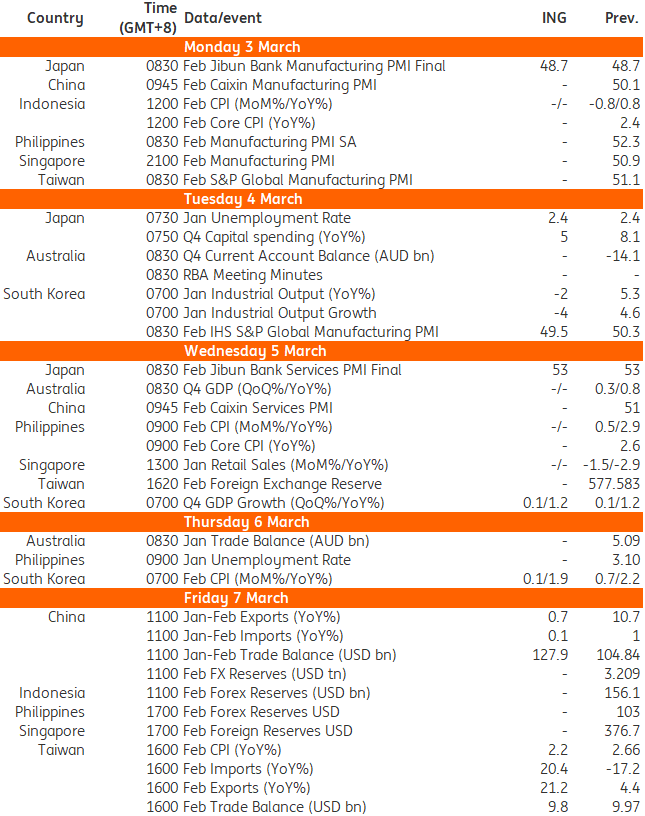

Asia week ahead: China’s Two Sessions grabs the spotlight

Next week, China's Two Sessions takes centre stage. Premier Li delivers the Government Work Report, detailing growth targets and priorities. We’ll also get PMI readings for China and Taiwan and inflation data for Taiwan and South Korea

China: Two Sessions to set this year's growth target and policy priorities

Next week’s main event is China’s Two Sessions meeting. Markets will pay close attention to the Government Work Report, to be delivered by Premier Li Qiang on 5 March. It will announce China’s 2025 growth target and detail top-level policy priorities. We expect China to stick with its “around 5.0%” GDP goal, the same as 2024, while providing much-anticipated details on the direction of fiscal and monetary policies. On the data front, China's official purchasing managers’ index (PMI) for February is scheduled for Saturday morning. We expect a return to expansion at 50.1. The Caixin PMI follows on Monday. On Friday, we will get our first look at trade data in the first two months of 2025 from China Customs.

Taiwan: PMI and CPI data in focus

Taiwan’s PMI data is set for release on Monday. On Friday, Taiwan releases February inflation data. We expect the consumer price index (CPI) to cool to around 2.2% year-on-year after a hotter-than-expected January gain of 2.6% YoY. Also, Taiwan’s February trade data is scheduled for Friday afternoon. The Lunar New Year effect may cause a rebound to double-digit growth for YoY trade.

Korea: activity data likely to point to a sluggish start

Monthly activity data will be released on Tuesday. We expect industrial production to drop sharply by 4.0% month on month, seasonally adjusted, (vs 4.6% in December) partly due to the longer-than-usual Lunar New Year holiday. Yet, retail sales may rebound thanks to government shopping voucher programmes. Overall, activity data will likely show a sluggish start to the year, with output and investment falling as political turmoil dampens sentiment. Meanwhile, consumer price inflation is expected to ease to 1.9% YoY in February. Gasoline prices declined from the middle of the month, while food costs stabilised after the LNY holiday.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article