Asia week ahead: Japan GDP and China inflation data

Next week’s main events are Japanese GDP and Chinese data on credit growth. Over the weekend, we’ll get readings on Chinese inflation, too

Japan: Weak GDP likely to keep the BoJ on hold

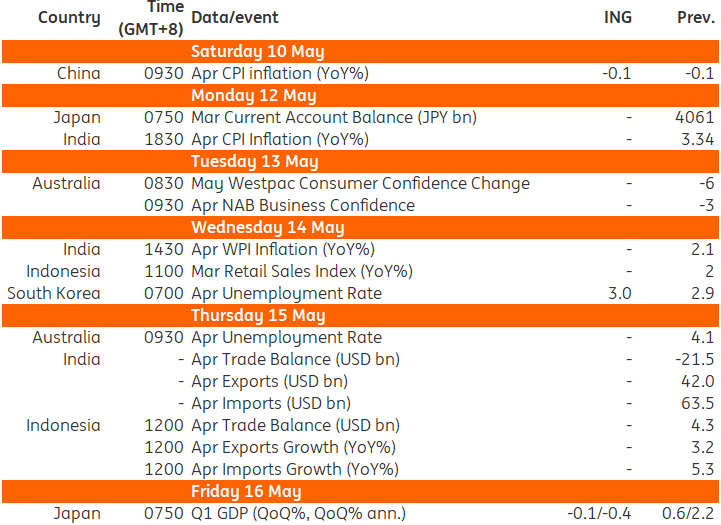

Japan’s economy is expected to contract in the first quarter by 0.1% quarter on quarter, seasonally adjusted, following a 0.6% gain in the last three months of 2024. Private consumption should grow thanks to solid household spending and the inflow of foreign tourists. Yet external demand could be the main drag. We already know that front-loading activity to beat tariffs was quite limited compared to other major exporters. Imports, meanwhile, rebounded. Weak growth is likely to keep the Bank of Japan -- and its rate-hike cycle -- on hold for now.

China: Deflationary pressures expected to deepen

China’s April inflation data is set for release over the weekend. We’re looking for consumer price inflation to stay in deflationary territory at -0.1% year-on-year, unchanged from March. Producer price inflation will likely remain in negative territory for a 31st consecutive month in April. Deflationary pressures will likely worsen thanks to tariffs, as exporters will have to sell products elsewhere. China’s credit data for April will also be published sometime in the week ahead. We’re expecting the credit growth recovery so far this year to continue. Still, the April data will not yet reflect the People’s Bank of China's most recent easing measures.

Key events in Asia next week

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article