Rob Carnell: Asia rebound could be weaker and later

For most of the Asia region, we forecast 2023 as a year of slowdown but with a recovery picking up in the second half of the year. The risk is that this comes later and is much weaker than we anticipate

Guarded optimism

For Asia including China, 2023 was a year which mixed optimism with caution. On the one hand, we have economies belatedly opening up, such as China and Japan, which are reaping the benefits of greater mobility and economic interaction. On the other hand, for this very trade-focused region, the slowdowns happening in the US and Europe threaten to undermine the export contribution, which is important for jobs as well as GDP.

On top of that, the downturn in the semiconductor cycle, a hugely important factor for North Asia, but also of great importance across the region, is also worrying, though one that many analysts including ourselves have touted as troughing in the second half of the year.

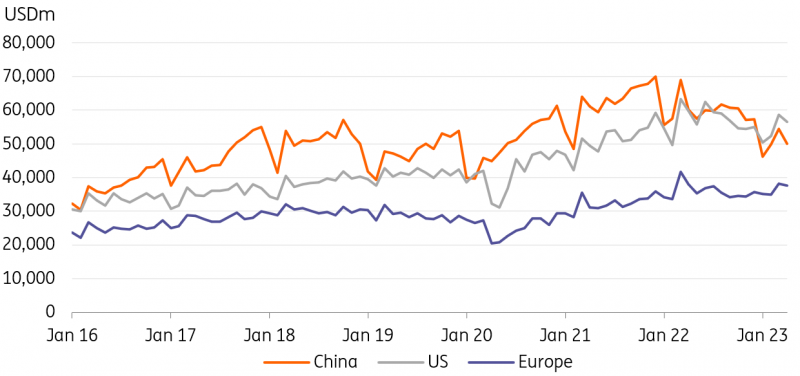

Asia's exports to major trading partners

Korea, Taiwan, India, Indonesia, Japan, Malaysia, Philippines, Singapore, Thailand, Vietnam

What's causing us to worry?

The risks to our cautious optimism about this year, and the better growth trajectory it implies for 2024, come from a variety of sources:

- The US / European slowdown hasn’t properly got going, could be harder and last longer than we expected. If we consider just the US, the main problem currently isn’t economic weakness, it is that large parts of the economy seem to be holding up much better than many thought, prompting worries about Federal Reserve rates staying higher for longer. The chart above shows Asian exports to China falling much more rapidly than to either the US or Europe. But the second half of the year could be the glide path down to much weaker US activity, and also for the eurozone as the ECB tightens the monetary thumbscrews. For Asia, that suggests exports weakening right up to the year-end, and the subsequent forecast bounce is beginning to feel a bit like wishful thinking.

- China’s rebound is looking spotty: while this isn’t necessarily bad news on a global scale, as it takes some pressure off commodity prices, and provides a more benign price backdrop as economies struggle with high inflation, it is certainly not helping the Asian export story. Although exports to the US and Europe are important, China’s own consumption of finished goods these days makes it an important end-consumer of a lot of consumer and capital goods. A consumer/catering-focused rebound isn’t doing a lot for the rest of Asia.

- Looking at the geographical direction of Asia’s export growth, the fact is that until very recently, exports from much of the region to the US and Europe were holding up fairly well. Exports to China were the standout weak spot. And with China, the single-largest export market for most of Asia, that isn’t good news. The cause of this is not completely clear, but it looks tied to the semiconductor slump and is probably at least in part a reflection of tighter restrictions on exports of hi-tech capital equipment to China, and restrictions on imports of Chinese technology goods to the US and its allies. This regulatory pushback is gathering momentum, not easing back, with Japan now also limiting what it will export to China. Calling a trough in the semiconductor cycle in the second half of 2023 may be optimistic. Looking for a rebound in 2024 may also be unrealistic.

While it is still too early to start chopping our growth forecasts for the region, the risks are skewed to the downside, and to any eventual recovery and upturn taking place later, and possibly being slower than we have currently pencilled in.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article

1 June 2023

ING Monthly: We’re only human This bundle contains 9 Articles