Asia FX Talking: PBoC happy to guide renminbi higher

- 10 February

- FX Talking

Given heavy weights in EM benchmarks, strong inflows into emerging markets are naturally helping Asian currencies. Here, the People's Bank of China seems very happy to embrace a stronger renminbi – both to position it as a major reserve currency and to help domestic demand. Elsewhere, new trade deals for India mean that USD/INR may have finally peaked

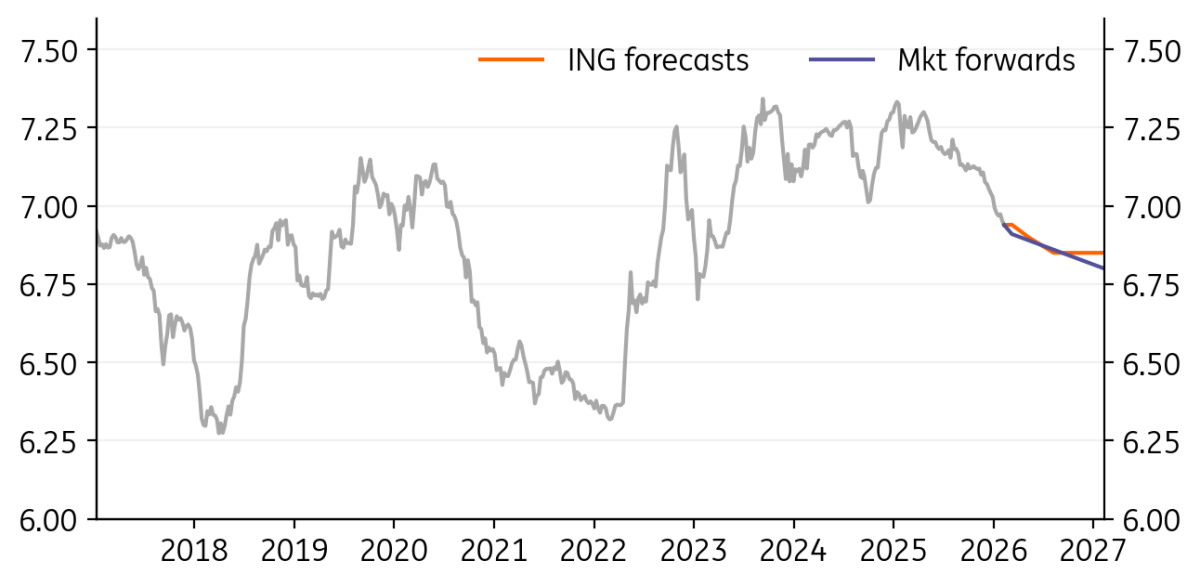

USD/CNY: CNY appreciation momentum continues amid internationalisation focus

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CNY

6.94

|

Neutral | 6.94 | 6.90 | 6.85 | 6.85 |

- The CNY continued its run of appreciation over the past month, with the USD/CNY grinding lower from around 6.99 at the start of the year down towards 6.93.

- The PBOC's fixings have continued to move lower as well, showing the PBOC is on board with this controlled pace of CNY appreciation. US-China yield spreads have reversed, widening slightly over the past month, as US yields rose while Chinese yields fell. China seeks to advance RMB internationalisation and use of the CNY, which suggests that further appreciation could be tolerated. The wildcard will be if the currency stability objective is softened in 2026.

- We are holding our 2026 fluctuation band forecast of 6.85-7.25 for now. Risks still look balanced towards CNY appreciation given the recent policy communications, and as the current account surplus remains quite high.

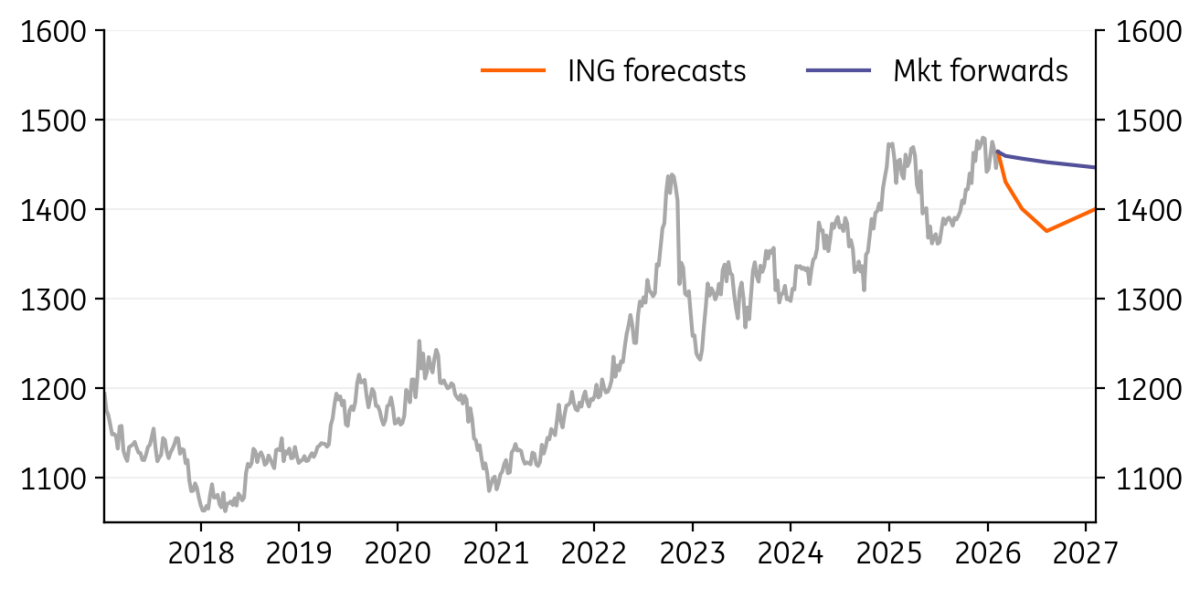

USD/KRW: A trend towards KRW appreciation

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/KRW

1463.00

|

Bearish | 1430.00 | 1400.00 | 1375.00 | 1400.00 |

- Despite USD/KRW recently returning back to the 1,460 level, we expect KRW to stay on a gradual appreciating trend.

- Capital inflows are likely to continue, supported by the AI boom and Kospi’s attractive valuations and robust earnings. The National Pension Service’s shift towards domestic assets and the introduction of a “Reshoring Investment Account” for retail investors may also change flow trends.

- The Bank of Korea is likely to keep its policy rate at 2.5% for an extended period while the Fed is expected to deliver cuts from June, supporting a USD/KRW move down to 1,425.

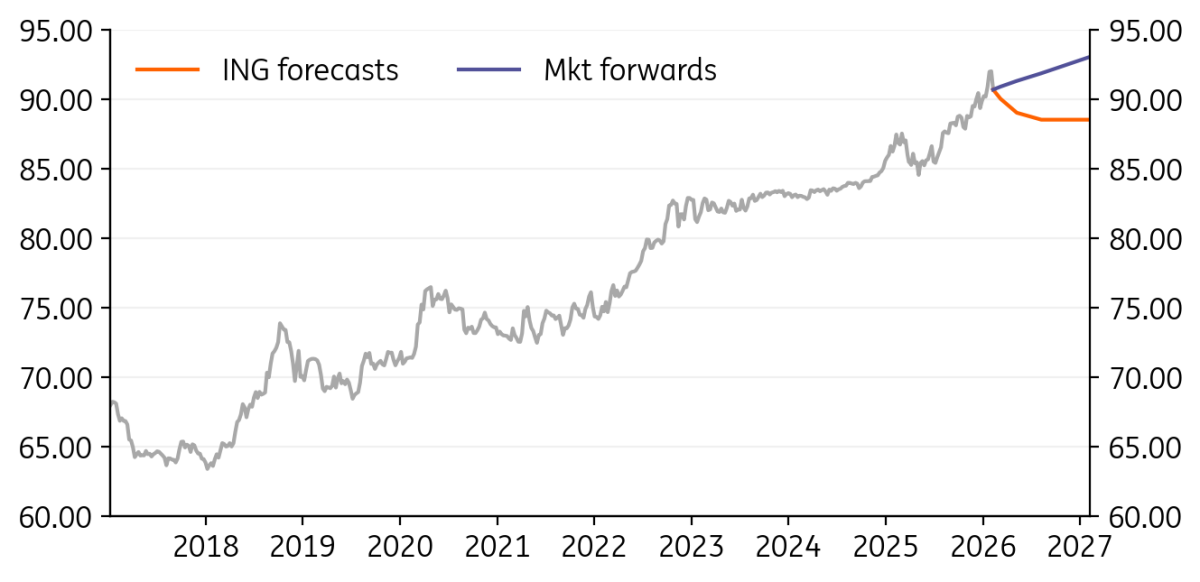

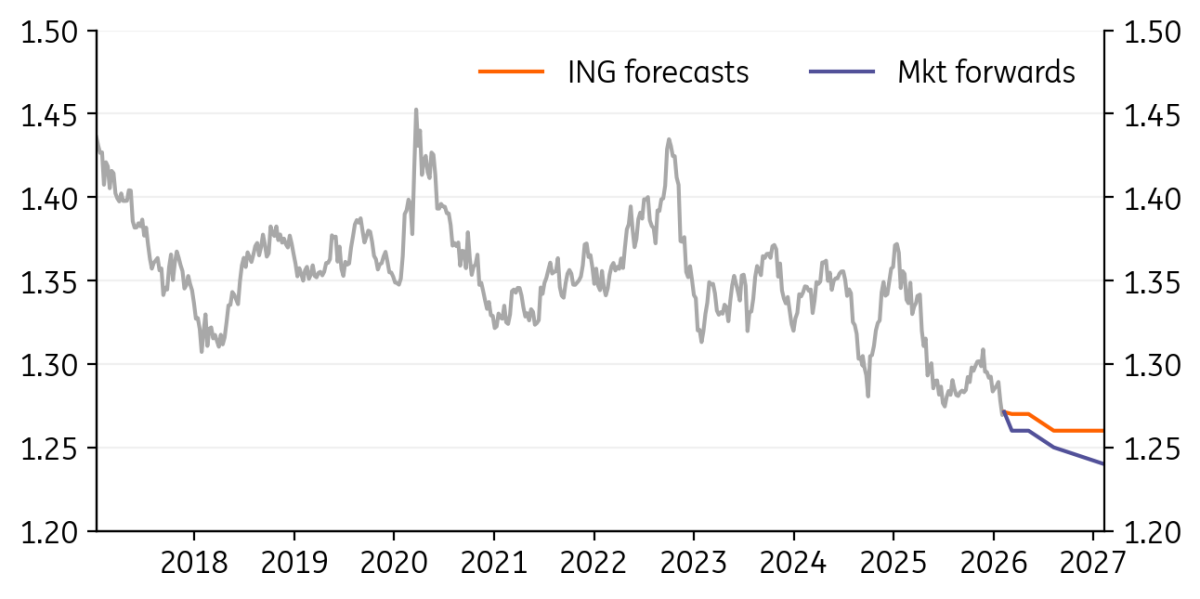

USD/INR: Sharp fall in REER should limit further downside

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/INR

90.60

|

Bearish | 90.00 | 89.00 | 88.50 | 88.50 |

- The INR finally got a boost from the long-anticipated trade deal with the US and the EU and appreciated in line with our anti-consensus call. Export diversification and integration into long-term supply chains is positive for long term growth.

- The RBI left its policy rate unchanged at 5.25% this week. Overall, the RBI’s assessment of the growth-inflation trade-off aligns with ours, suggesting that we are nearing the end of the rate cutting cycle, with possibly one last rate cut in 2Q.

- We think we have seen the peak of USD/INR in 2026, and INR should trade with an appreciation bias for the rest of 2026. Given the recent softening in net FDI inflows, the India-EU FTA should help revive investment momentum. From a valuation standpoint, the sharp decline in INR’s REER should also limit downside.

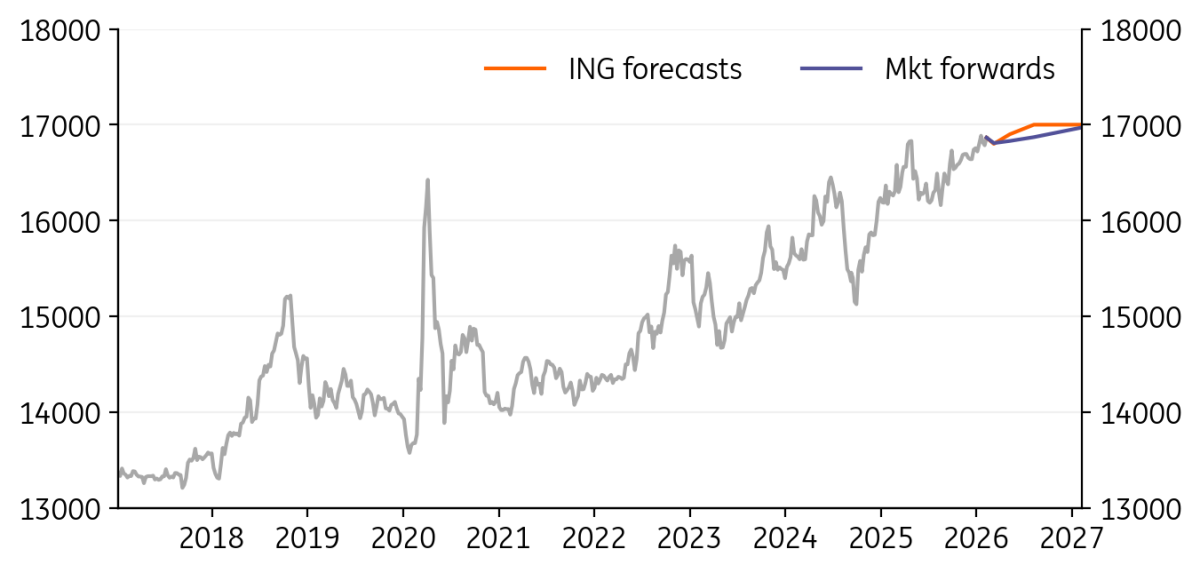

USD/IDR: Fiscal concerns could keep IDR under pressure

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/IDR

16865.00

|

Neutral | 16800.00 | 16900.00 | 17000.00 | 17000.00 |

- Moody’s lowered Indonesia’s credit rating outlook to negative from stable, citing rising uncertainty in policy direction. The move followed MSCI’s earlier comments on transparency shortcomings, which had already triggered a sharp equity market sell‑off and heightened investor sensitivity.

- Concerns around fiscal sustainability remain prominent, with recent policy unpredictability and weaker communication further unsettling foreign investors. These developments have amplified doubts about Indonesia’s commitment to fiscal discipline at a time when market confidence is already fragile.

- With soft growth and weak revenues weighing on the rupiah, we expect additional IDR depreciation as investor caution keeps FII inflows muted.

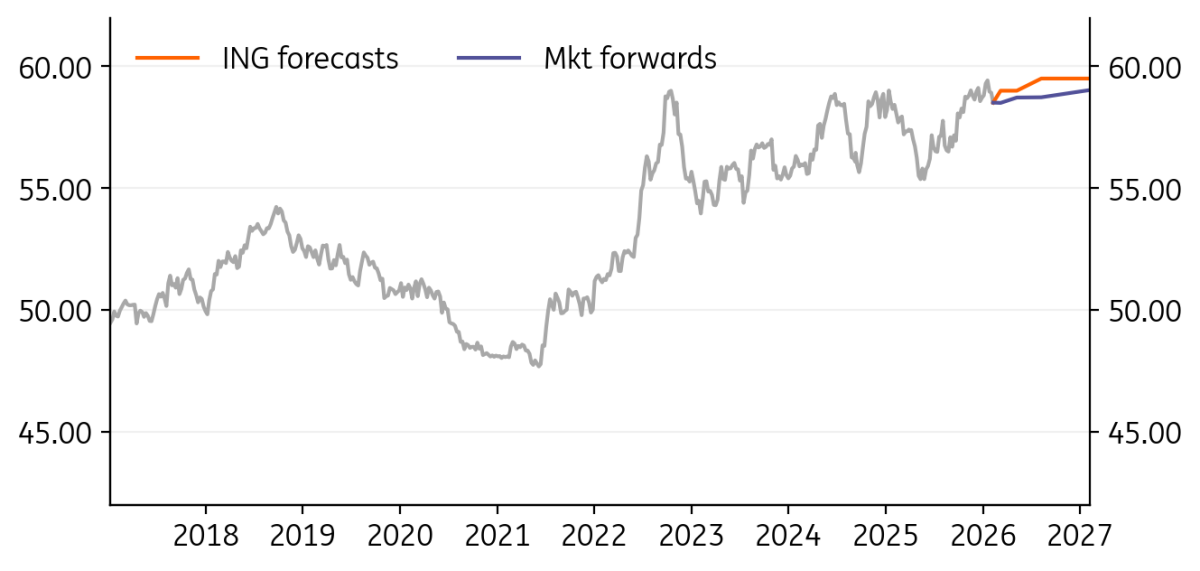

USD/PHP: Growth concerns to keep PHP weaker

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/PHP

58.57

|

Mildly Bullish | 59.00 | 59.00 | 59.50 | 59.50 |

- The 4Q GDP data confirmed that soft government spending has become a more persistent drag, weighing not only on fiscal outlays but also on business and household sentiment. We expect this pressure to continue at least through 1H26, as the ongoing political uncertainty continue to dampen confidence.

- We revise our GDP growth forecast for 2026 lower by 20bp to 5.2% and continue to expect the BSP to cut rates by 25bp at the February meeting. If weak momentum persists, the risk tilts towards another cut in 2Q.

- Despite the recent strength in Peso largely driven by market expectations of BSP nearing the end of the rate cutting cycle after a relatively stronger inflation print, we think on balance risks are tilted towards softer growth than higher inflation. Risk of further monetary policy easing should keep Peso weaker vs the USD.

USD/SGD: Business optimism resilient

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/SGD

1.27

|

Neutral | 1.27 | 1.27 | 1.265 | 1.265 |

- The Singapore economy is expected to continue performing well. Strong growth last year (4.8%) and a manageable 10% tariff rate on exports to the US has seen the optimism extend into 2026. Whole economy business PMIs are picking up and electronic exports remain strong.

- The steady appreciation of the Chinese renminbi is a very supportive anchor for the SGD, although we think there is scope for the Monetary Authority of Singapore to ease should any signs of economic weakness show through. After all, CPI looks very contained at just above 1.00%.

- A softening US economy and a stronger renminbi present downside risks to our baseline USD/SGD profile.

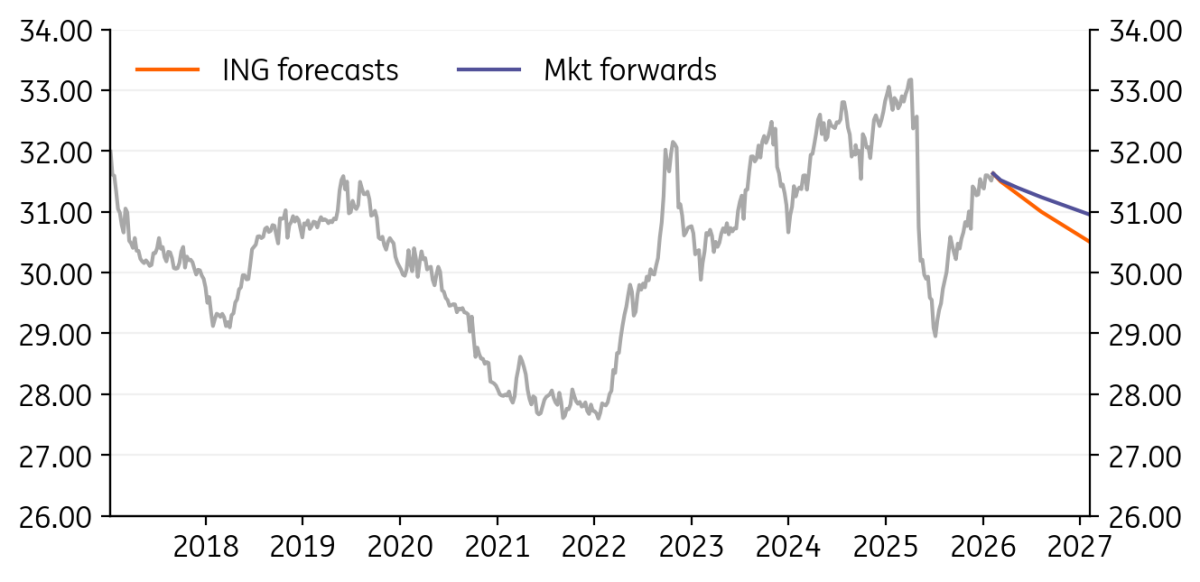

USD/TWD: Another month of stability for the TWD

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TWD

31.59

|

Mildly Bearish | 31.50 | 31.30 | 31.00 | 30.50 |

- The TWD saw another month of minimal currency fluctuation, with the USD/TWD moving within a narrow range of 31.3-31.6.

- Domestic drivers for the TWD generally favoured a stronger TWD again. The US-Taiwan yield spread slightly narrowed over the past month, as Taiwan yields rose a little faster than US yields. Equity market net inflows were positive. Taiwan’s trade data continued to drive phenomenal growth, and Taiwan’s current account surplus is likely to have further picked up.

- The current levels are likely to be comfortable for policymakers. Reports emerged over the past month that Taiwan life insurers cut the hedging ratios to the lowest levels since 2020.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

10 February

FX Talking: Dollar appetite erodes

- This bundle contains 6 Articles