Asia FX Talking: Prospects of monetary easing weigh on renminbi

- 12 June 2023

- FX Talking

USD/CNH remains well bid as a strong dollar meets prospects of Chinese monetary easing in the quarter ahead. USD/CNH may not lead USD/Asia lower this year. However, if we are right with our call for Fed easing and a weaker dollar, then we can continue to see demand come through for TWD and KRW - as investors try to ride the AI boom-driven demand for semiconductors

Source: Shutterstock

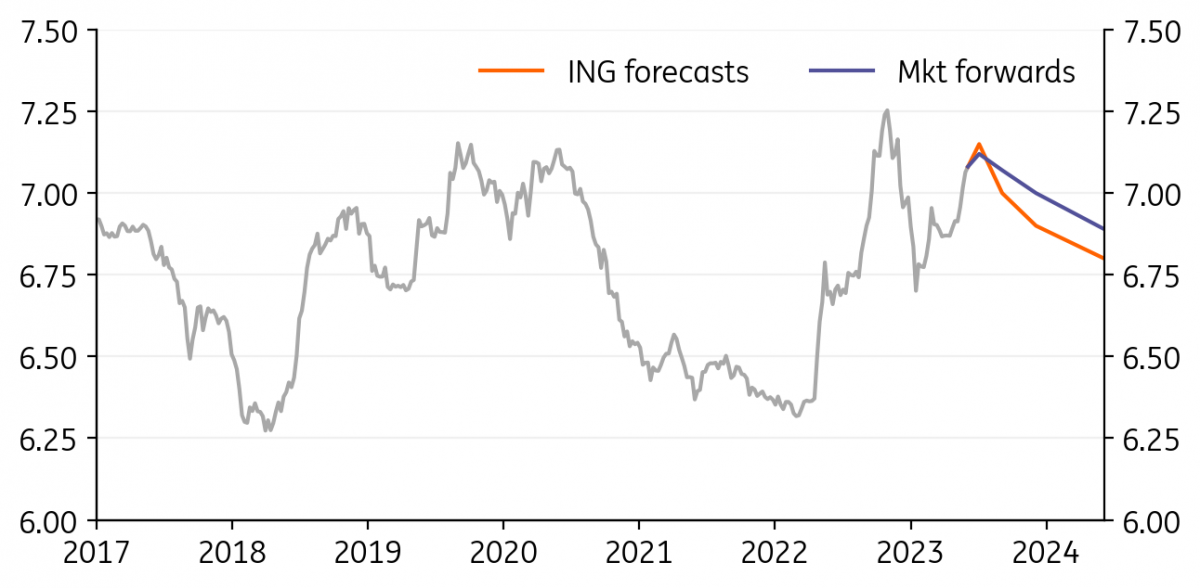

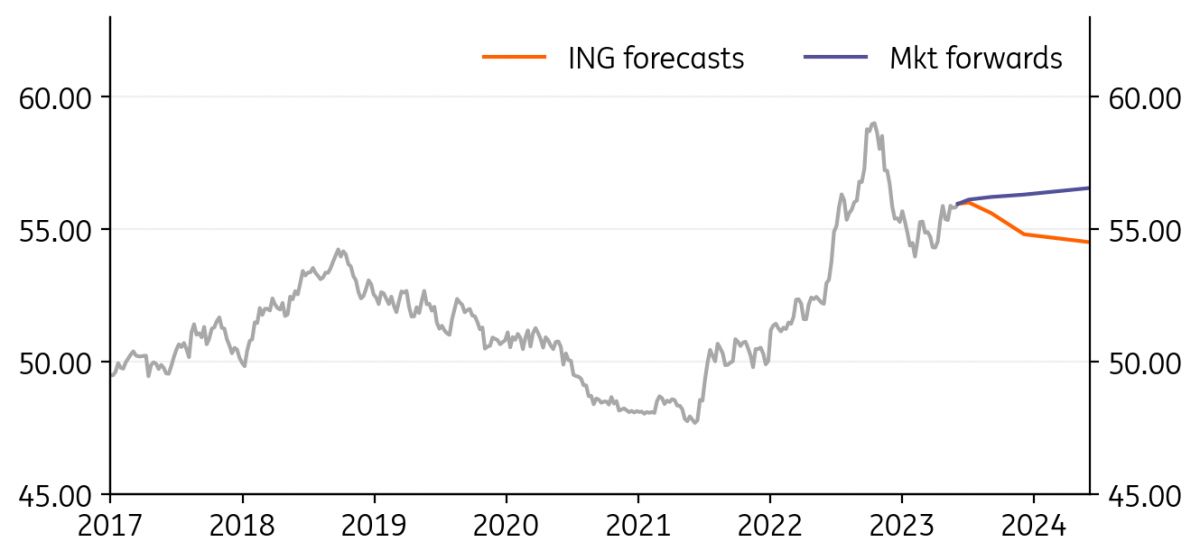

USD/CNY: Disappointing reopening weighing on CNY

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CNY

7.1415

|

Neutral | 7.15 | 7.00 | 6.90 | 6.80 |

- China’s disappointing economic reopening has taken its toll on the Chinese yuan, which has lost almost 3% over the last month, putting it towards the bottom of the Asia pack.

- With even the service sector likely to see growth moderating in the near-term, we don’t believe we have yet seen the top for USD/CNY.

- However, it seems unlikely that this will be allowed to continue indefinitely without some policy support. Targeted RRR cuts, housing support and subsidies on E-vehicles, for example, may be in the pipeline, and possibly policy rate cuts, too.

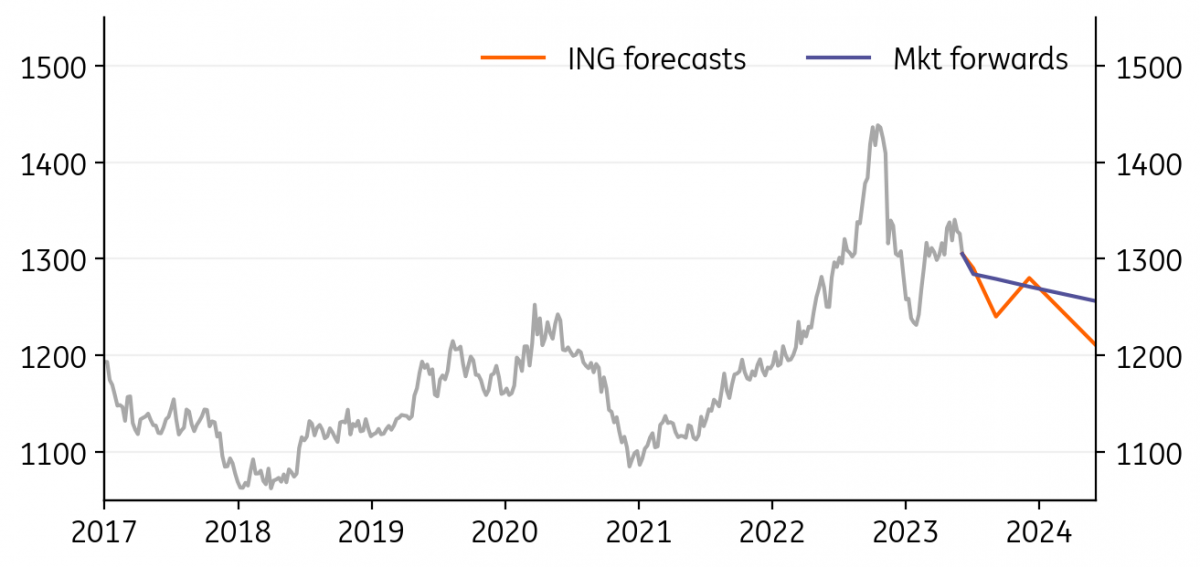

USD/KRW: Equity-led appreciation on chip hype

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/KRW

1286.40

|

Neutral | 1290.00 | 1240.00 | 1280.00 | 1210.00 |

- The Korean won has been the Asian region’s best performing currency over the last month, and one of the only ones to register an appreciation against the US dollar over this period,

- Like Taiwan, Korea has benefited from its position as one of the world’s pre-eminent semiconductor-producing economies amid the hype over AI chip demand, and has seen both the KOSPI and KOSDAQ picking up as capital inflows to equities recovered.

- The export sector remains in sharp decline, though, and that is before we have even seen the US slow significantly. That, and the disappointing Chinese economic reopening, could delay and temper any further KRW appreciation.

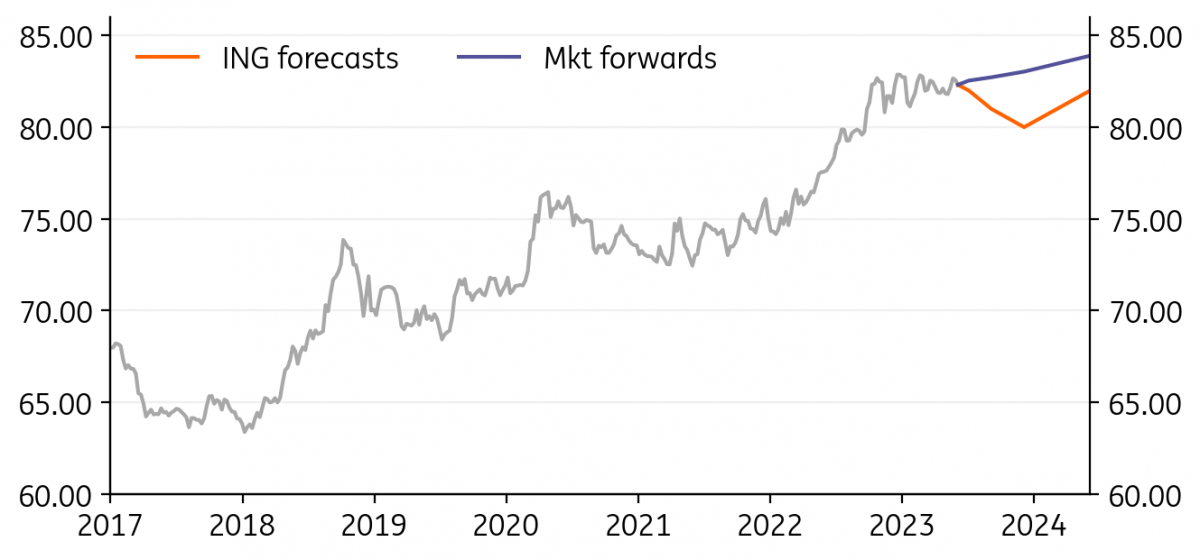

USD/INR: Still range-trading

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/INR

82.449

|

Neutral | 82.00 | 81.00 | 80.00 | 82.00 |

- Since October last year, the Indian rupee has traded very narrowly between about 81 and 83 and is currently towards the weaker end of that range.

- Over the last month, all Asian FX has softened against the USD, but the INR has lost less ground than many of its peers and is only down a little over 1% over this period.

- Looking ahead, India’s impressive reduction in inflation should provide near-term support to the INR, though in due course, a reversal of central bank tightening could see the currency reverting to a depreciating trend.

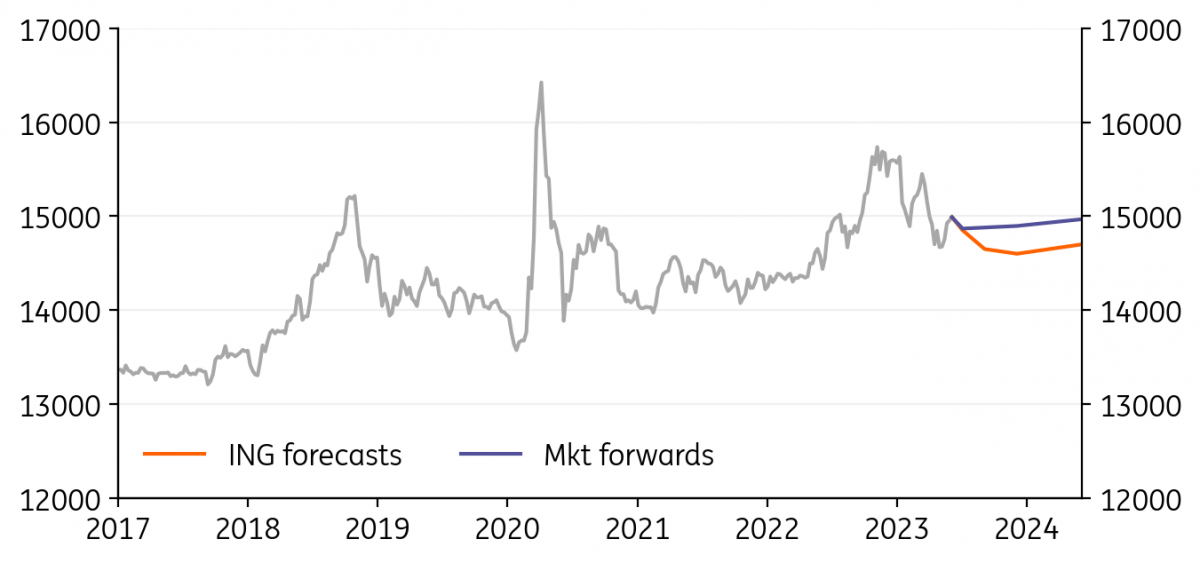

USD/IDR: IDR falters as foreign investors exit the bond market

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/IDR

14862.00

|

Neutral | 14850.00 | 14650.00 | 14600.00 | 14700.00 |

- The Indonesian rupiah slid as foreign investors exited from the local bond market. Meanwhile, Indonesia’s trade surplus continues to fall short of the highs recorded in 2022, raising concerns about the current account balance.

- Bank Indonesia Governor Perry Warjiyo indicated that BI was not likely to hike rates anymore but also clarified that they would not be in a rush to cut policy rates soon.

- We expect the IDR be pressured in the near term with the BI pledging to keep rates untouched to support the domestic recovery.

USD/PHP: PHP retreats as BSP signals rate hikes are over

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/PHP

56.06

|

Neutral | 56.00 | 55.60 | 54.80 | 54.50 |

- The Philippine peso slipped in May after foreign investors exited from the local equity market, with the PSE down roughly 2.9% for the month. Meanwhile, trade data reported during the month also showed the trade deficit swelling to $4.9bn, indicating strong corporate demand for the dollar.

- Bangko Sentral ng Pilipinas (BSP) Governor Felipe Medalla opted to keep rates unchanged at 6.25% and telegraphed he was done hiking rates.

- The PHP faces additional pressure to weaken as the BSP takes on a more dovish stance.

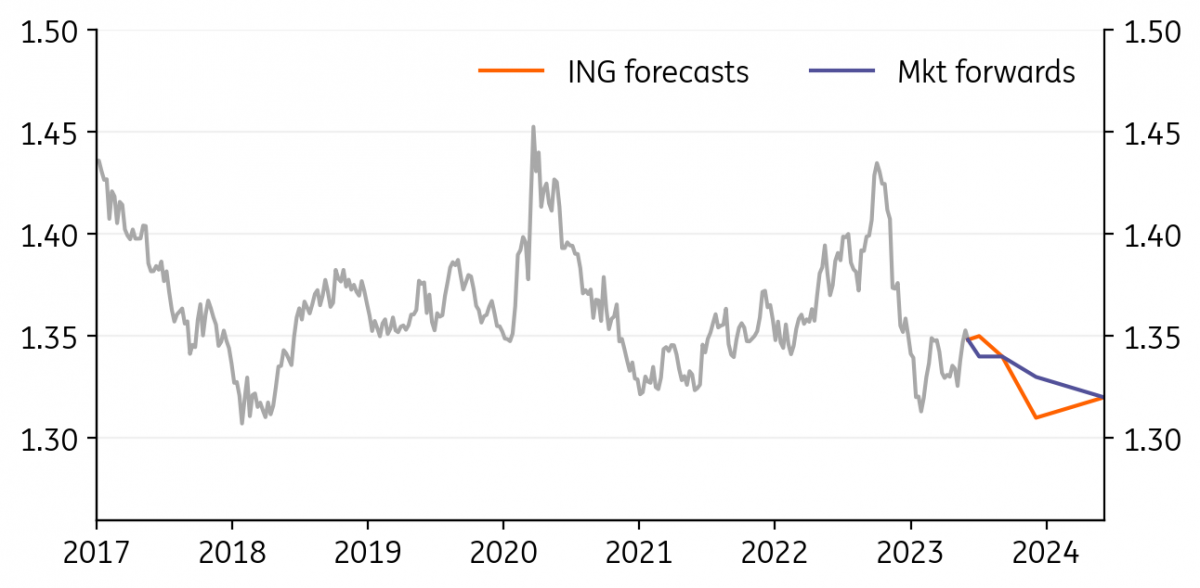

USD/SGD: SGD was pressured after inflation surprised on the upside

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/SGD

1.3416

|

Neutral | 1.35 | 1.34 | 1.31 | 1.32 |

- The Singapore dollar weakened, tracking most regional currencies on heightened anxiety over the US debt ceiling issue and the outlook for Fed policy.

- Non-oil domestic exports remained in negative territory on soft demand while inflation surprised on the upside with both core and headline beating expectations. The SGD NEER was steady over the past month.

- We expect the SGD to move sideways with the MAS retaining its current hawkish stance given the upside surprise in the most recent inflation report.

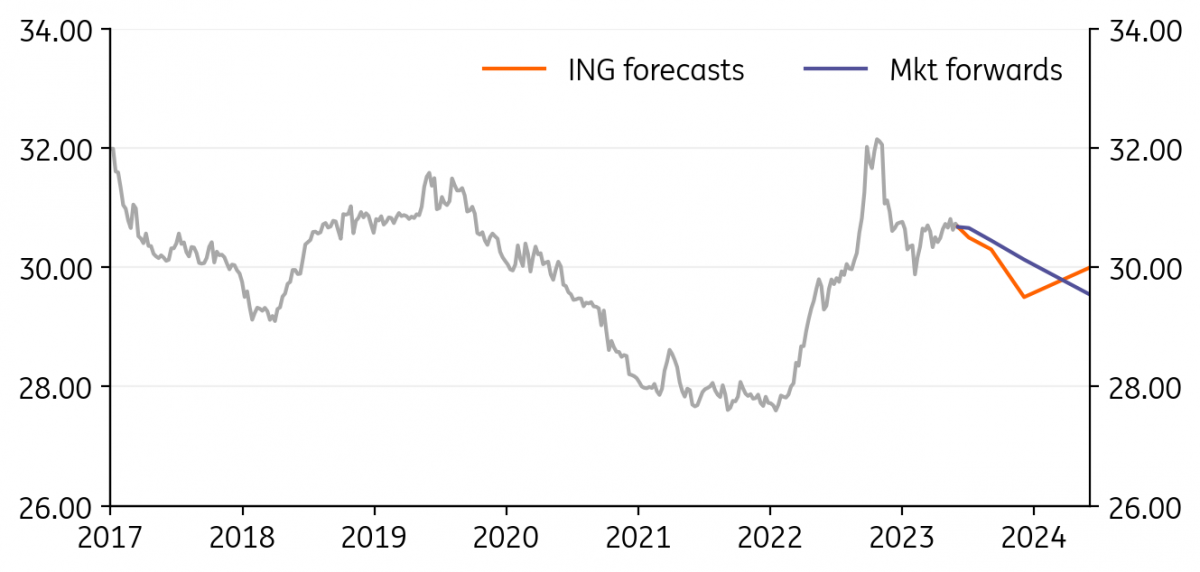

USD/TWD: TWD supported by AI excitement

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TWD

30.768

|

Neutral | 30.50 | 30.30 | 29.50 | 30.00 |

- Despite the ongoing geopolitical tensions, domestic recession and semiconductor cycle downturn, the Taiwan dollar has held very steady over the last month.

- Improving sentiment about future semiconductor demand stemming from AI demand is helping to boost related equities, and portfolio capital inflows into Taiwan’s equity market have helped support the currency over the last month.

- Some further recovery in Mainland China could provide a further boost to Taiwan's economy and the TWD, though the very near-term doesn’t look too promising.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more