Asia FX Talking: North Asia continues to outperform

- 8 August 2025

- FX Talking

North Asian currencies backed by stronger external positions should continue to outperform. Trade deals with the US are not seen as catastrophic, and the dominant theme should be lower US rates and a weaker dollar. India's rupee looks set to stay under pressure on geopolitical challenges

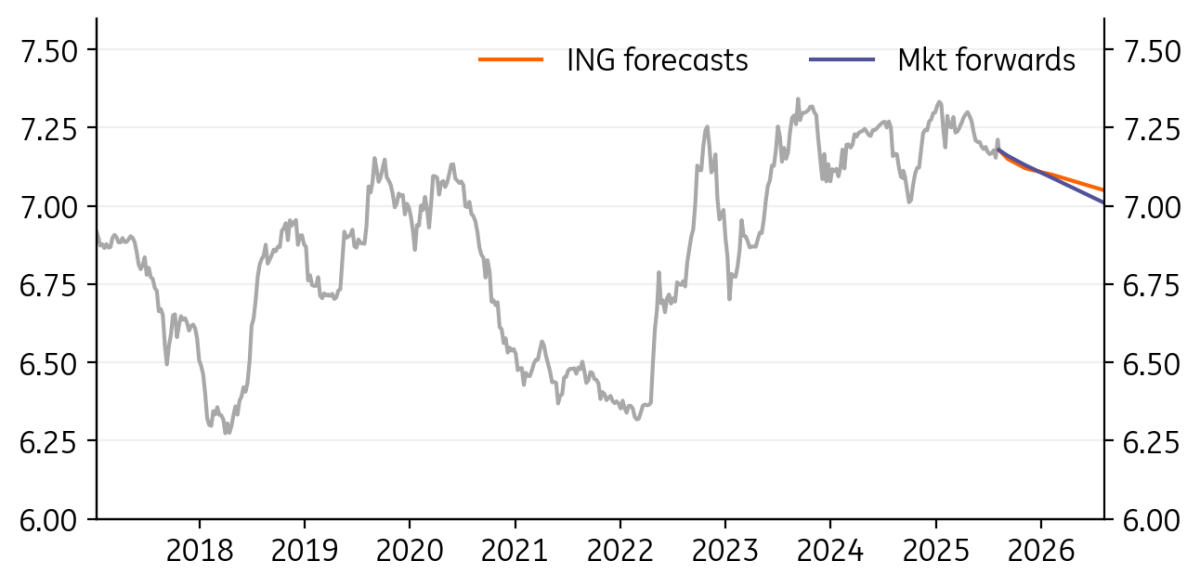

USD/CNY: CNY’s steady nature allowed outperformance in July

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/CNY

7.1788

|

Mildly Bearish | 7.15 | 7.12 | 7.10 | 7.05 |

- USD/CNY remained one of the most stable currency pairs against the dollar, with last month’s trading range only slightly expanding to 7.15-7.20.

- After two months at broadly neutral levels, the People’s Bank of China's countercyclical factor moved towards pushing back against depreciation in the past month. US-China yield spreads narrowed after jobs data pushed US yields lower while Chinese yields rose.

- The CNY remains one of the lowest volatility currencies against the dollar this year, and this is unlikely to change in the near term. We continue to hold our call for a 7.00-7.40 fluctuation band for the year. Moving forward, we expect the CNY to enter a gradual appreciation trend as yield spreads narrow further.

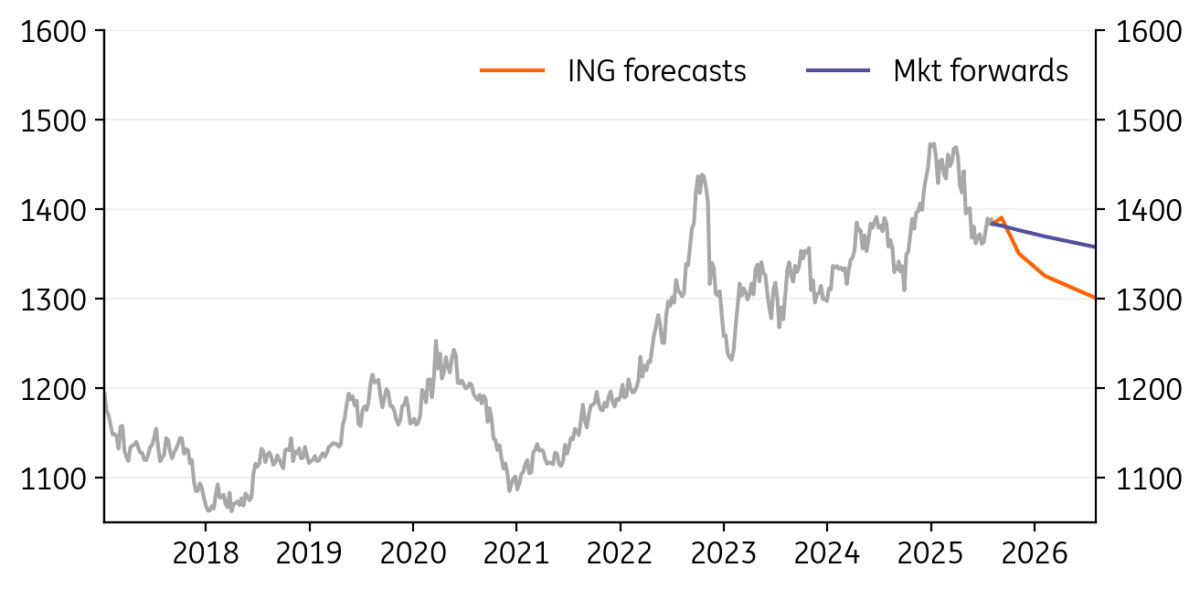

USD/KRW: Temporary weakness in KRW is expected

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/KRW

1383.10

|

Neutral | 1390.00 | 1350.00 | 1325.00 | 1300.00 |

- After the Korea-US trade agreement, markets initially improved but reacted negatively to the government's equity tax proposal, causing the KOSPI to drop over 5%. Investors are watching for potential changes to the tax plan; this may limit KRW gains.

- The Bank of Korea is expected to stand pat in August. Housing prices appear to be stabilising, but it is still too early to tell.

- Rising concerns over the US recession may also put further pressure on the KRW. We expect a weaker won temporarily until there are clearer signs of a Federal Reserve cut in September.

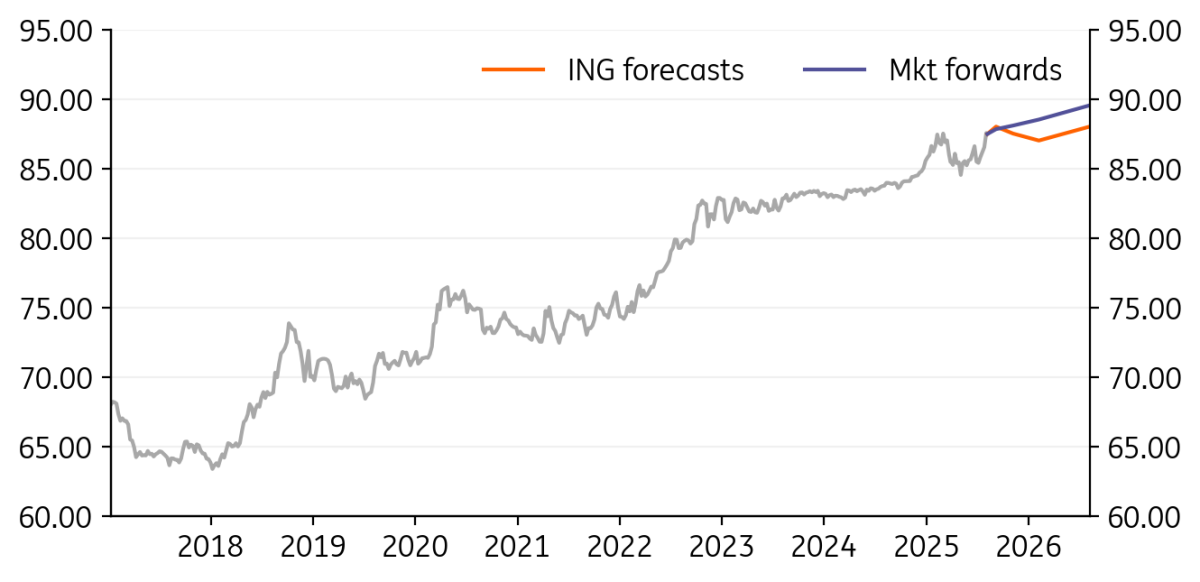

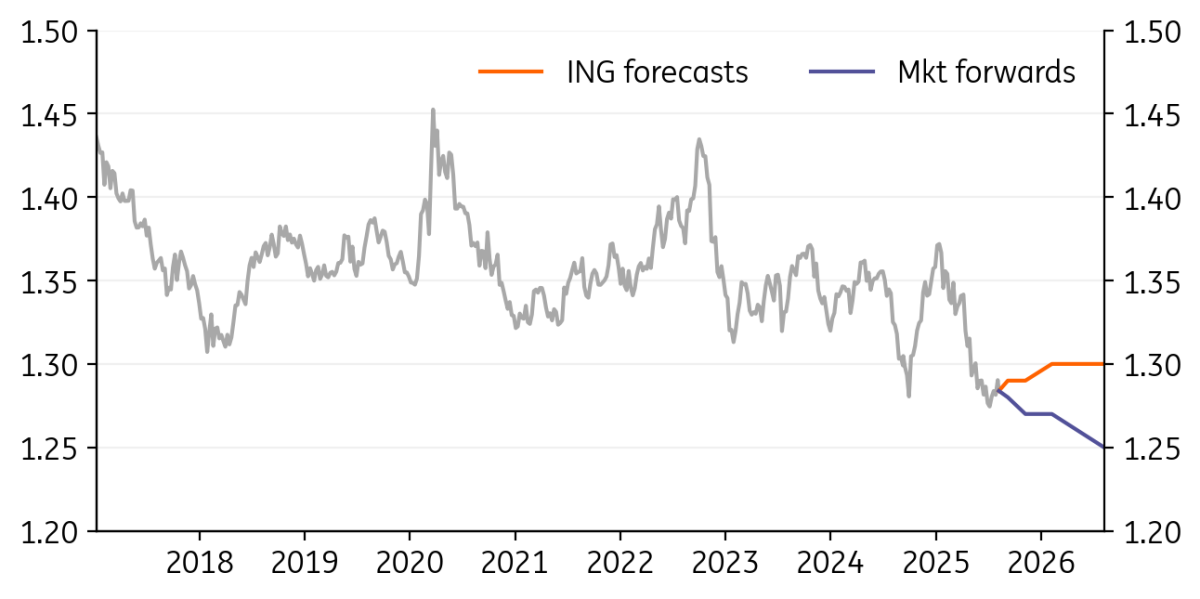

USD/INR: INR could continue to underperform on trade uncertainty

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/INR

87.47

|

Mildly Bullish | 88.00 | 87.50 | 87.00 | 88.00 |

- INR was the worst performer in the region last month, weighed down by volatile oil prices and the lack of a trade deal with the US that was largely expected to be in favour of India. Instead, India received the highest tariff rate of 25% in the region.

- Given that the US accounts for almost 18% of India's exports, the 25% tariff rate could have a meaningful impact on GDP growth. However, we think it’s likely that both nations will continue the negotiations, using levers such as reducing imports from Russia.

- In the interim, uncertainty could weaken investor sentiment, as also reflected in FII outflows in July. REER undervaluation and RBI intervention should limit the damage to INR.

USD/IDR: IDR is stabilising, helped by foreign inflows

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/IDR

16290.00

|

Mildly Bullish | 16400.00 | 16500.00 | 16600.00 | 16800.00 |

- Real rate differentials between Indonesia and the US remain one of the key drivers of the currency pair, and that has been coming down as IDR 10-year real rates have corrected. Weakness in the rupiah could persist, given high sensitivity to the rate differential.

- While Indonesia remains less exposed to tariffs in general because of its low value-added exposure to exports to the US, its commitment to import large amounts of energy and agricultural goods from the US will add to the current deficit widening. At the same time, FDI inflows have also remained soft.

- What's been helping IDR stabilise is FII inflows in debt that have gained momentum, which could be sustained given Bank Indonesia’s dovish bias. That, together with IDR undervaluation on a REER basis, should mean a stable USD/IDR in the near term.

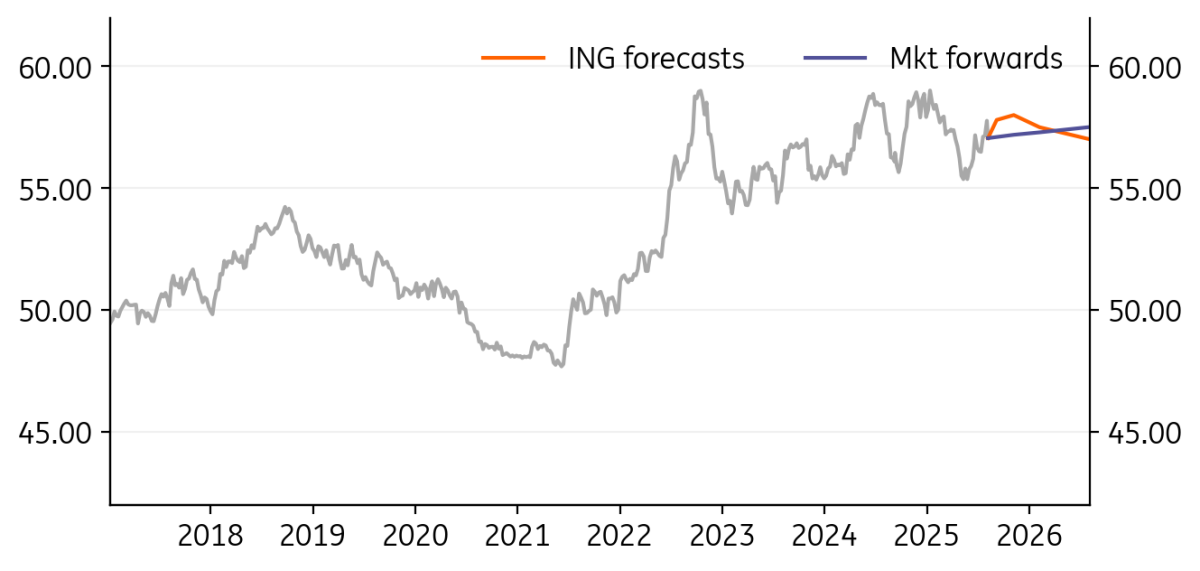

USD/PHP: Headwinds from over-valuation and wider twin deficits

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/PHP

57.05

|

Mildly Bullish | 57.80 | 58.00 | 57.50 | 57.00 |

- The tariff rate for the Philippines, set at 19%, was both higher than our expectations and higher than the announcement on ‘Liberation Day’. This has put downside risks to our 2025 GDP growth forecast of 5.5%.

- Consumer price index inflation came in at 0.9% year-on-year in July, lower than consensus expectations, driven by lower food prices. We maintain our forecast for two more 25bp rate cuts in the third and fourth quarters, ending 2025 at 4.75%, driven by softer inflation.

- REER overvaluation and twin deficit concerns will continue to be headwinds for the local currency. Given our expectations of still large rate cuts and BSP’s increasing tolerance for currency weakness, we expect PHP to trade with a weakening bias.

USD/SGD: SGD outperformance to fade gradually

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/SGD

1.2838

|

Neutral | 1.29 | 1.29 | 1.30 | 1.30 |

- The Monetary Authority of Singapore opted to keep its monetary policy unchanged, highlighting that the risk of a sharp near-term slowdown in global growth has receded. This has raised the bar for further monetary policy easing this year.

- The SGD NEER continues to hover at the top of its policy band, pushing the currency’s overvaluation to new highs. With MAS striking a less dovish tone and strong FDI inflows supporting the external balance, the SGD is likely to stay firm – unless we see a meaningful rebound in the USD (DXY).

- On the rates side, SORA has corrected notably over the past two months due to ample domestic liquidity. However, MAS’s more neutral stance suggests that the downside in SORA may now be limited, potentially establishing a floor for short-term rates.

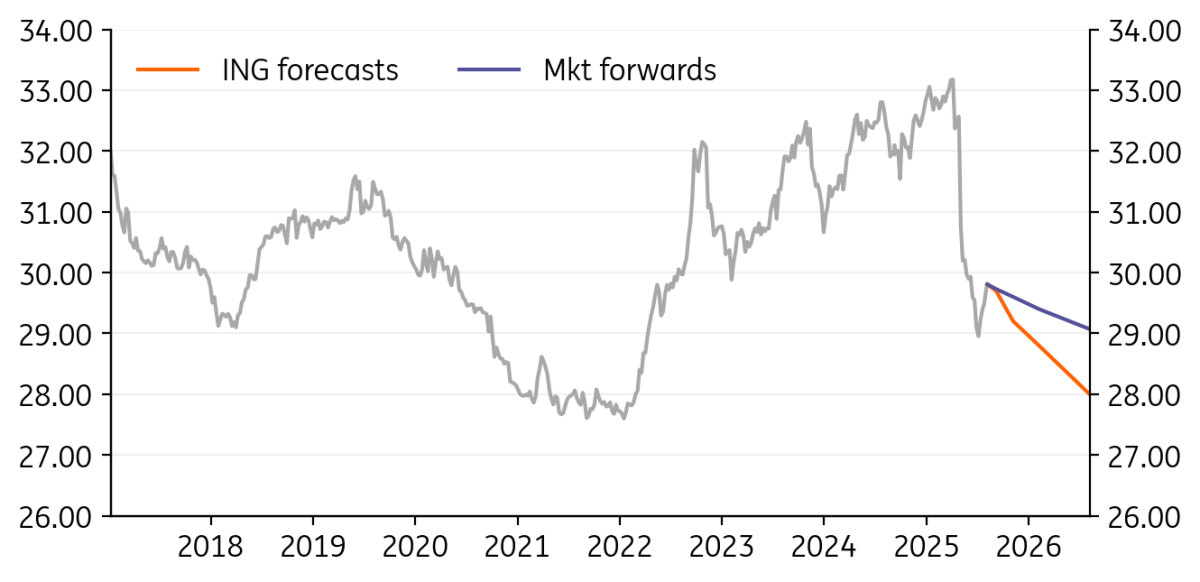

USD/TWD: TWD unwound some recent gains amid dollar rebound

|

Spot

|

One month bias | 1M | 3M | 6M | 12M |

|---|---|---|---|---|---|

|

USD/TWD

29.80

|

Mildly Bearish | 29.70 | 29.20 | 28.80 | 28.00 |

- The TWD was generally on a weakening trajectory over the past month, with the USD/TWD rising from the lows of 28.8 to briefly breaking over 30.

- Domestic drivers of the TWD were neutral to slightly positive for the currency. Equity market net inflows slowed slightly but remained well positive, and yield spreads were little changed over the past month. We had another month of strong data, which suggests that the odds of a move from the Central Bank of the Republic of China in its September meeting are low.

- At this juncture, risks once again look balanced toward TWD strengthening over the next few months, especially if we get a more dovish Fed.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Authors

Included in the following bundle

Bundle

FX Talking: Cracks in the dollar’s shield

- This bundle contains 6 Articles