Asia: Central banks still focused on growth

- 4 February 2022

- Australia China

There have been some notable tweaks to policy accommodation in recent weeks, but central banks in Asia-Pacific are still favouring growth over inflation concerns

Growth vs Inflation

The last few weeks have seen inflation figures in Asia ticking higher on average, and a couple of central banks have even tightened policy rates. Most notably, the region’s most hawkish central bank, the Bank of Korea (BoK) raised policy rates for a third time to 1.25%. And the Monetary Authority of Singapore (MAS) has also surprised markets with an unscheduled adjustment to its exchange rate policy.

But compared to other parts of the world, in particular, Central and Eastern Europe, policy rates in Asia are barely moving. Most central banks in the region are hanging on to their growth-supportive monetary stances, and rates in China are actually being cut.

The main reason for this difference in central bank behaviour is inflation. It’s not that there is no inflation in Asia. Inflation rates on average have edged higher. But inflation has not shot up as fast or as far as it has in Europe or the US, requiring less pushback from the region's central banks. The most recent upticks in inflation came from Australia, where the headline number has now reached 3.5%YoY. But that's only half what it is in America And inflation in Singapore and Korea, where policy has been tightened, is no higher than 4%. And of course, China bucks the trend again with inflation actually falling recently.

So why is inflation so much better behaved in the Asia-Pacific region? There is no one reason, and we've written about it extensively here, but below we list some of the key contenders:

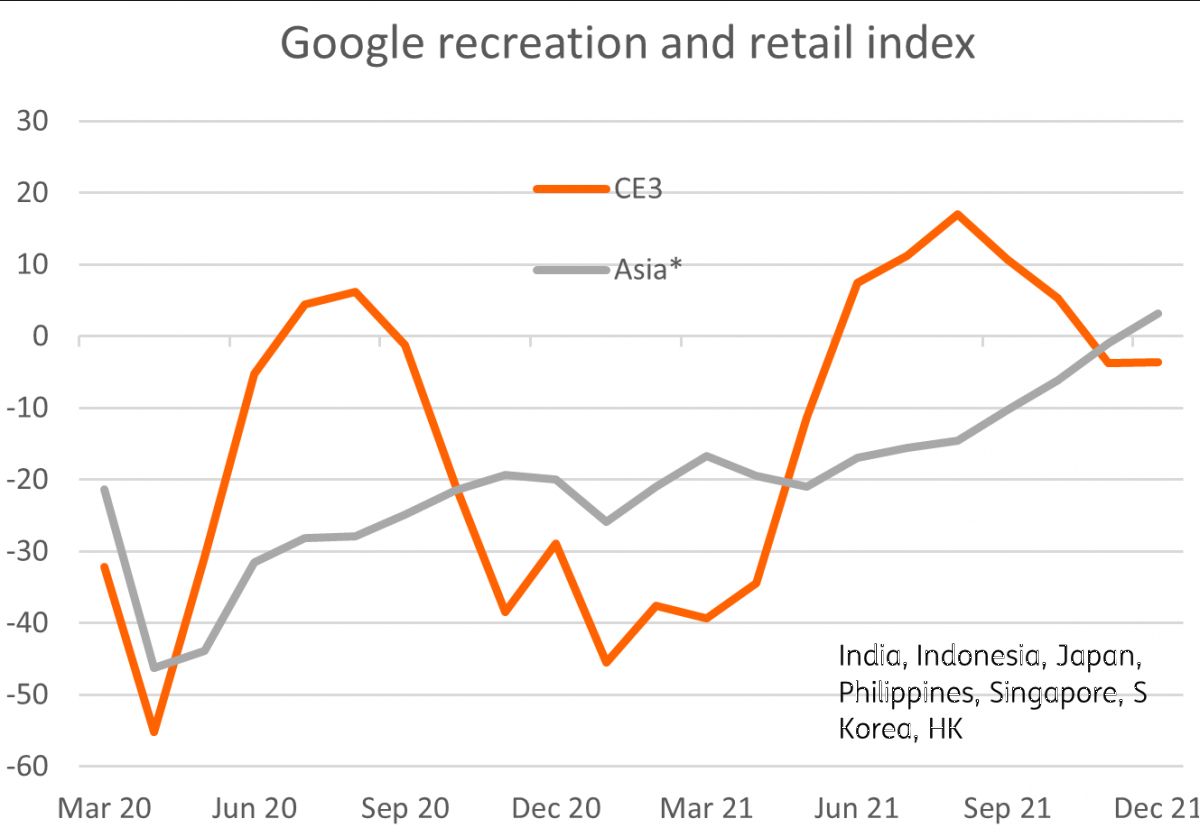

Asian gradualism vs all-or-nothing approach to lockdowns of CE3

Google retail and recreation index

4 reasons why Asian inflation is behaving better than elsewhere

- Gradual re-opening. When you compare the Google retail and recreation indices for the CE3 (see chart above) with the average for Asia, you can see that from the initial movement restrictions imposed in response to the initial Covid wave, the re-opening in Asia has been quite steady and gradual. The shift in demand to goods that distinguished the lockdown, and then the swing back to demand for services as economies have re-opened has been far more gradual in Asia, arguably resulting in less intense bottlenecks in supply.

- Supply constraints: These have been a feature of price rises in Western Economies, in particular, though not exclusively for semiconductors. Production of semiconductors is concentrated in Asia. And it seems that at the moment, much of this production goes to satisfy markets in the region, rather than far-flung export destinations.

- Logistics: A secondary factor magnifying this supply constrain effect is logistics. It is still up to nine times more expensive to ship goods from Asia to Europe or the US than it is to import them from the US or Europe to Asia. These pass-on costs are therefore much smaller in Asia.

- EM vs DM: Where we do see inflation in Asia, it seems to be more of a developed-market phenomenon: Interestingly, and although there is some elevated inflation in some Emerging Asia, the greatest pick-up in inflation (from admittedly very low pre-pandemic rates) in Asia seems to have been in the more developed economies. A lot of this is energy (wrapped up in transport components) but these economies will also have a higher weight from services in their basket, which might also be a reopening factor.

Inflation may have a little further to go in Asia, and we also haven’t yet seen the full impact of Omicron, which may exacerbate supply constraints further. But even though policy rates will likely rise further this year to offset this inflation, we aren’t expecting aggressive hikes from Asian central banks this year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: The masks, and the gloves, are coming off

- This bundle contains 15 Articles