Accelerating Czech wages are a pro-inflationary risk

Robust wage growth will further drive Czech household spending, prompting policymakers to consider both increased consumption and more relaxed budgetary constraints. With additional funds available for discretionary spending, consumer prices may rise in response to strong demand, particularly in the service sector

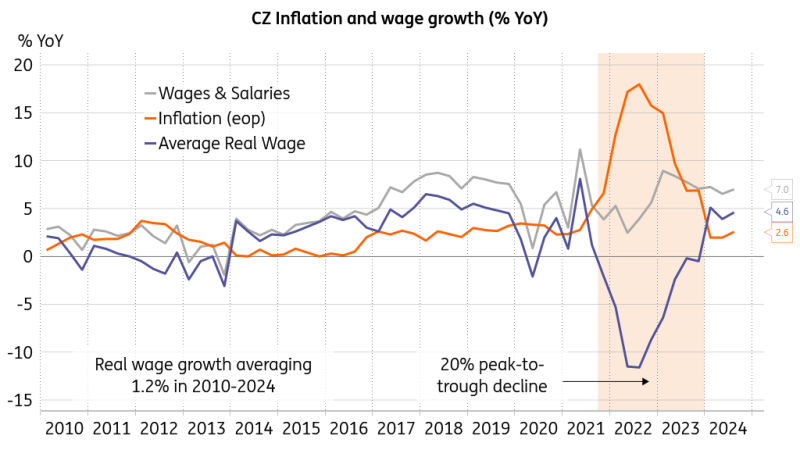

Czech wage growth provides fuel for further growth

Czech average wage growth increased in 3Q24 to 7% in nominal terms and picked up to 4.6% when adjusted for inflation. Both readings are stronger than both the market and the Czech National Bank's expectations. The volume of wages and salaries rose by 7.2% year-on-year, with the number of employees rising by 0.2% YoY. Median wages accelerated to 6.6% YoY, signalling robust wage increases even for lower-income workers. Seasonally adjusted average wages added 1.9% from the previous quarter.

Real wage growth flies high

Looking at the sectors, the strongest annual growth in average wages was recorded in real estate activities (14.4%), scientific and technical activities (10.1%), and water supply and waste management (9.3%). The lowest growth was recorded in public administration, defence, and education (3.7%).

When looking at the dynamics over 1Q-3Q24, nominal wages added 6.9% compared to the preceding year. This represents a substantial relief to household budget constraints, as annual inflation over the same period rose 2.3%. The tight labour market amid a continued economic rebound will likely support this real wage trend further, adding fuel to the consumer spending engine. Household consumption expenditure, with nominal and real wages coming in more potent than the latest CNB forecast, will exert pressure on policymakers to shift their attention towards future inflation pressures when deciding between growth support via lower borrowing costs and more caution when it comes to safeguarding price stability.

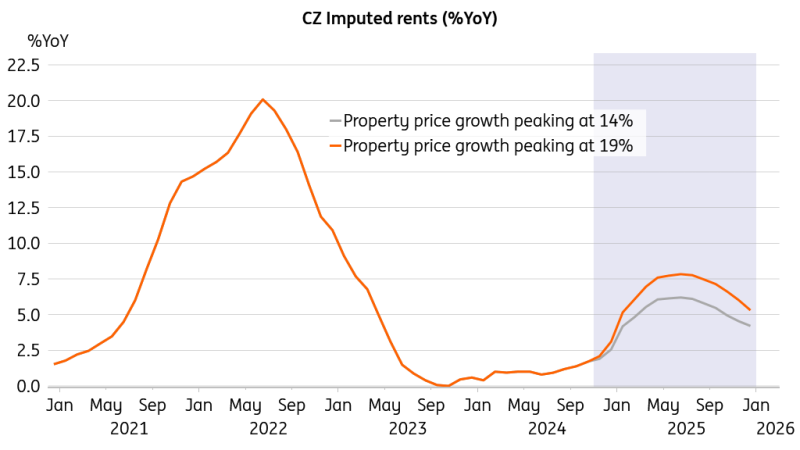

Wage growth to support rents and foster inflation

The robust wage growth will likely add pressure on the market and imputed rents in the coming months, further supported by accelerating property prices. Property prices are a crucial variable in imputed rent estimates within the CPI. The property prices are measured only on a quarterly basis, then are interpolated to the monthly frequency and plugged into the calculation of the imputed rent as per the CPI.

Rents are set to foster inflation

We mimicked such an approach, with an assumption of the residential price index annual growth peaking at some 14% in January next year and another assumption with the dynamics peaking at 19%. The following regression results suggest that annual growth in imputed rents would reach between 4.2% and 5.2% in January next year and peak between 6.2% and 7.8% mid-next year. This pro-inflationary factor would foster both core and headline inflation throughout the first half of the coming year.

No viable plan for a way out of European economic misery

The outlook for economic performance is another factor the CNB must consider when moving towards a more relaxed monetary policy stance. However, the disappointing recovery is partially linked to Europe-wide structural issues such as relatively high energy prices, cost-increasing overregulation, uphill competition against cheap Chinese imports, and an absent viable plan about the path out of the economic malaise that is suffocating investment incentives.

Non progredi est regredi

As for ameliorating economic growth opportunities in Europe, the following areas are crucial for a discussion to boost European economic prospects, reinforce investment incentives, and safeguard its prosperity.

i) Reshape the Green Deal parameters and timespan

ii) Acknowledge consumer’s preferences and rethink the campaign against the internal combustion engine

iii) Set up space in a way that ideas can compete without crippling ideology-driven interventions

iv) Support innovations with bazooka funds for the best research institutes, with merit-based resource allocation

v) Streamline regulation in personal data protection so that pharmaceutical research is retained, and AI research can lift off in Europe

vi) Propose a viable energy strategy that would provide more clarity about future energy price developments to reduce the already high uncertainty that the European industrial base is facing

vii) Rethink the CO2 allowances market, making the system more beneficial to the European industry rather than overseas competition

viii) Consider tariffs on Chinese imports for relevant reasons, such as environmentally burdensome production in China, a more CO2-intensive energy sector, state support for companies, low intellectual property protection, etc.

ix) Reduce dependence on Chinese production in critical areas such as energy production and storage, information technology, and security

x) Support the European defence and security industry, as the threat of a NATO-Russia conflict is no longer an ephemeral idea

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download article