A year of tough decisions for the UK

- 5 January 2018

- United Kingdom

Several challenges lie ahead for Brexit, leaving the Bank of England with a conundrum

December's breakthrough helps unlock a transition period agreement

As a turbulent 2017 finally drew to a close, politicians on both sides of the channel were finally able to breathe a sigh of relief. After months of deadlock, an agreement was reached on the UK’s financial liabilities, citizens’ rights, and ultimately most contentiously, the Irish border.

December’s breakthrough means that a transition period looks set to be agreed by the end of the first quarter. Admittedly such an agreement won’t be legally binding until the full exit treaty is ratified later this year. But a firm commitment by both sides that there will be a ‘status quo’ transition period until late 2020/early 2021 should be enough to prevent firms enacting their ‘no deal’ contingency plans.

Plenty of challenges to overcome - and the clock is ticking

Firms could remain cautious when it comes to investment

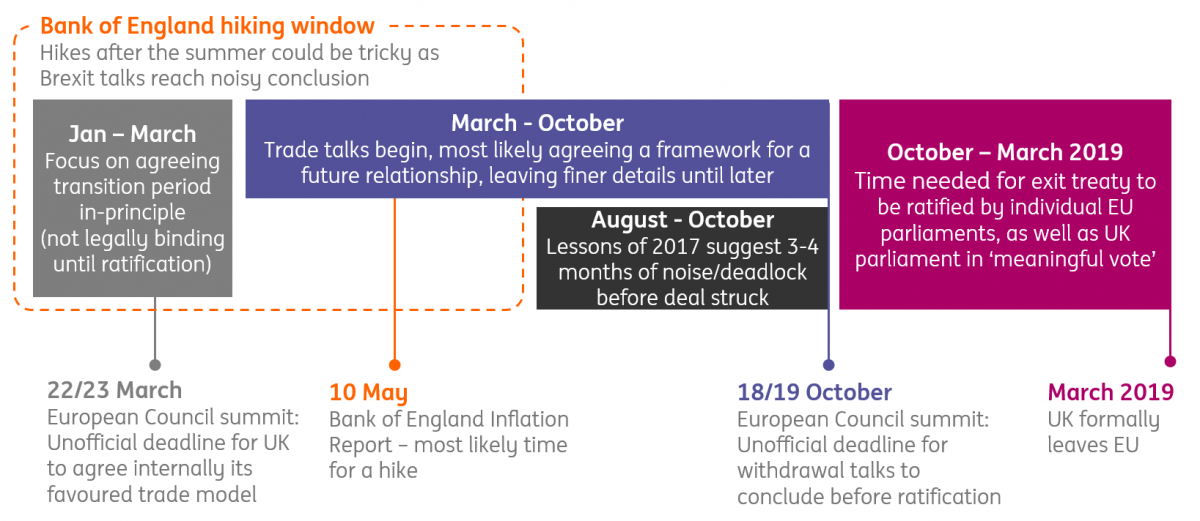

Of course, there are still plenty of challenges looming this year – perhaps the biggest of which is whether a trade deal can actually be agreed in full before March 2019. Trade talks are unlikely to begin before March, before which time the UK will internally agree on the trade model it’s aiming for. The talks will need to be wrapped up by October’s European Council summit, to allow time for each member state to ratify a deal as well as for the UK parliament to hold it’s ‘meaningful’ yes/no vote on what is agreed.

That leaves an extremely narrow six-month timeframe for trade negotiations, which makes it more likely that only the broad framework of a trade deal will be agreed before the UK exits the EU. This implies that the finer details would then be thrashed out during the transition phase.

This raises the question of whether a two-year transition period will be long enough for businesses, or indeed the customs infrastructure, to adjust to the new relationship. It’s also possible that, without knowing the finer details of the UK’s future trading relationship, firms could remain cautious when it comes to investment (particularly that with a longer-term horizon).

2018 Brexit timline

The odds of a rate hike rely a lot on wage growth

This is one reason why economic growth is likely to remain reasonably sluggish this year. Consumer spending is also set to remain under pressure, with disposable incomes likely to be (at best) flat. This will limit growth to around 1.4% this year, giving the Bank of England a conundrum when it comes to deciding whether to hike rates again this year.

Wage growth may not take-off quite as much as the Bank of England hopes

Ultimately, wage growth will be pivotal to the decision. There has been some slightly better news on this front, with signs that skill shortages in certain sectors are prompting firms to boost salaries to retain staff. To take one example, the shortage of UK lorry drivers increased by 49%[1] in 2017 as the pool of talent shrinks, which led to firms to offer up to 20% premiums on hourly rates.

That said, with the cost of raw materials and energy picking up, and demand still fairly anaemic in many sectors, some firms are likely to take a more conservative approach with an eye on maintaining margins. The Bank of England is optimistic about wage growth, although we still feel it may not take-off quite to the extent its forecasts assume.

[1] According to Manpower/Freight Transport Association

A rate hike this year isn't guaranteed

So with growth likely to remain sluggish and uncertainty over the path of wage growth, we still think a rate hike this year cannot be guaranteed, though this is increasingly a close call. But whatever policymakers decide, we think they have a fairly narrow window before the summer if they want to squeeze in another rate rise. The lessons of the past few months tell us that, before some deal being struck in October, there could be 3-4 months of deadlock and noisy negotiations. This leaves February, or more likely May, as possible candidates for another rate hike this year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Where next for Europe in 2018?

- This bundle contains 5 Articles