A languishing eurozone economy

- 6 July 2023

The latest data show that eurozone growth is not picking up, with services now also losing steam. While it’s not all downhill from here, subdued growth is the best we can hope for. Inflation is now clearly coming down, but the European Central Bank is still set for two more rate hikes

(Overly?) optimistic ECB growth outlook

After negative growth over the winter quarters, the ECB’s staff forecasts pencil in a gradual acceleration of eurozone GDP growth to 0.3%, both in the second and third quarters of this year, and 0.4% from the fourth quarter onward. However, eyeballing the most recent data, it doesn’t look as if the eurozone economy is accelerating – on the contrary.

The first real indicators for the second quarter, such as retail sales and industrial production, actually came out below the average of the first quarter. And sentiment indicators for May and June rather point to further deterioration. The €-coin indicator, a monthly tracker of GDP growth, averaged -0.3% for April and May. In that regard, we fear that second-quarter growth will be close to 0%, with a non-negligible probability of negative growth.

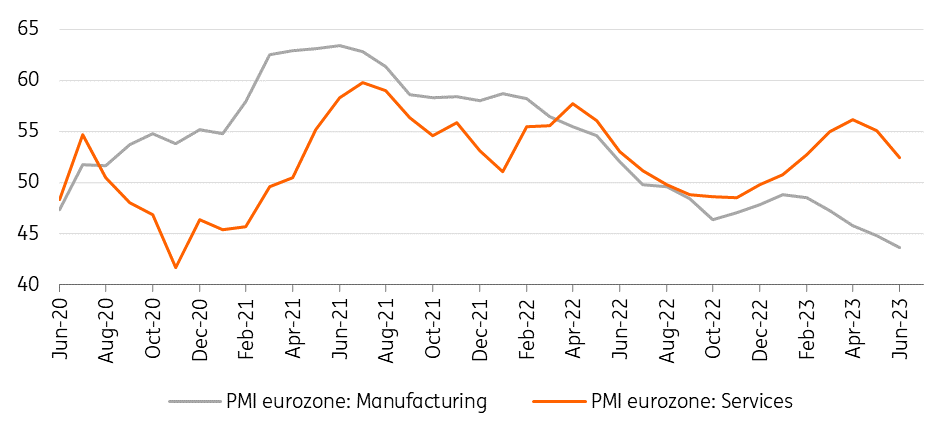

Manufacturing in recession and services is slowing

Services are now also slowing

We certainly don’t deny that the pick-up in wage growth, in combination with lower energy prices, is boosting consumers’ purchasing power, supporting consumption growth over the coming quarters. But at the same time, some increase in the savings ratio looks likely as the economic outlook has become more uncertain (in some member states unemployment has started to increase).

All sectors are now signalling a deceleration in incoming orders, while inventories in industry and retail are at a very high level. Even services, which held up well despite the recessionary environment in manufacturing, are losing steam. The services confidence indicator fell in June below its long-term average. That doesn’t necessarily mean that the only way is down – we still expect a strong summer holiday season, supporting third-quarter growth. But after that things might become shakier again, as the US economy is expected to have fallen into recession by then.

The bottom line is that we now only expect 0.4% growth in 2023. Subsequently, on the back of the low carry-over effect, we pencil in a 0.5% GDP expansion for 2024.

Downward trend in inflation continues

The flash headline inflation estimate for June came out at 5.5%, while core inflation increased slightly to 5.4%. However, the increase in core inflation is entirely due to a base effect in Germany that will disappear in September. The growth pace of core prices, measured as the three-month-on-three-month annualised change in prices, now stands at 4.4%. That is still too high, but the trend is clearly downwards.

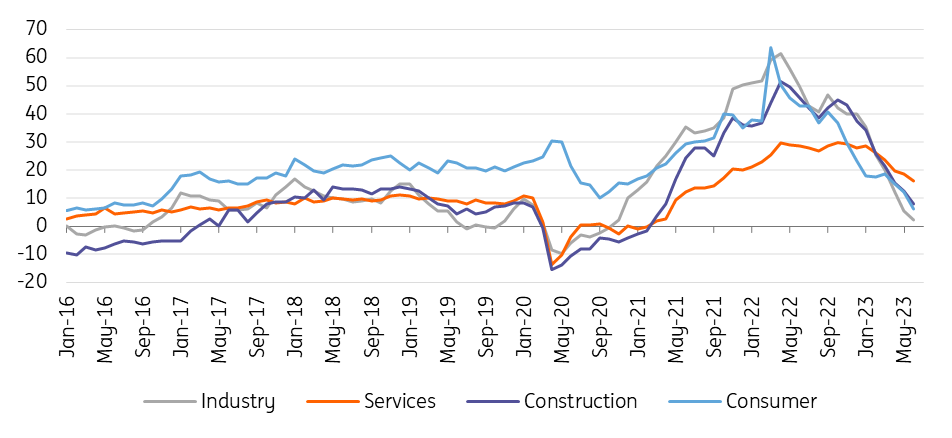

The inventory overhang is leading to falling prices for goods. In the European Commission’s survey, selling price expectations softened again in all sectors, while the expected price trends in the consumers’ survey fell to the lowest level since 2016. It, therefore, doesn’t come as a surprise that we expect the downward trend in inflation to continue, with both headline and core inflation likely to be below 3% by the first quarter of 2024.

(Selling) price expectations are coming down across the board

Two additional rate hikes

As the ECB has seemingly lost faith in its forecasting models (the staff is expecting 2.2% in 2025), it has been basing monetary policy increasingly on current inflation figures. No wonder that it still believes there is a need to tighten further.

In a rather hawkish speech in Sintra last month, ECB President Christine Lagarde reiterated that a rate hike in July looks like a done deal and at the same time she said that “under these conditions, it is unlikely that in the near future the central bank will be able to state with full confidence that peak rates have been reached”.

Board member Isabel Schnabel added in a recent interview that “given high uncertainty about the persistence of inflation, the costs of doing too little continue to be greater than the costs of doing too much”. That all points to (at least) two additional 25 basis point rate hikes. That would bring the deposit rate to 4% in September. Rates will probably remain at that level until the summer of 2024 when lower inflation is likely to open the door for some cautious easing.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: The economic twilight zone

- This bundle contains 13 Articles