The US braces for a harder landing

- 5 April 2023

- United States

Banking stresses mean much tighter lending conditions, which in an environment of rising borrowing costs, soft business sentiment and a rapidly weakening housing market, makes a hard landing for the economy look all the more likely. Inflation will slow even more quickly in this environment, opening the door to interest rate cuts later this year

Recession risks mount as credit is curtailed

Even before the recent banking turmoil we had been concerned about the possibility of a recession in the US this year. The harder and faster a central bank moves monetary policy into restrictive territory, and this has been the fastest most aggressive period of rate hikes for 40 years, the less control you have over the outcome. We were concerned about economic stresses, but it is the financial stresses revealed by the failure of Signature Bank and Silicon Valley Bank that have come to the fore first.

There are around 4,200 banks in the US and most of them are classified as small – less than $250bn in assets. These “small” banks account for around 43% of all commercial bank lending in the US and are particularly important in the commercial and residential real estate markets. The deposit flight they have experienced in the wake of recent banking failures leaves them with less scope to lend, even if they wanted to. Regulators will be paying much closer attention to what each bank has been up to and with the prospect of much tougher regulations to come, banks will be wanting to tidy up their balances sheets as quickly as possible. We doubt big banks will be able to fill the gap, so credit flow will be heavily disrupted.

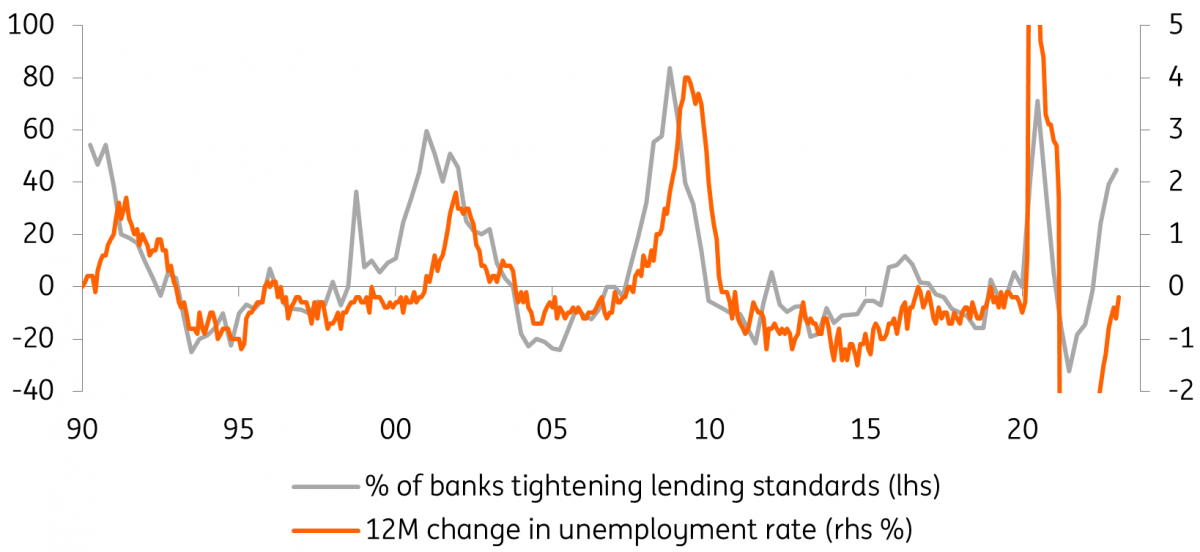

Banks stepping back, default risks and student loan angst

The Federal Reserve’s Senior Loan Officer’s survey had already indicated that banks had become far more cautious in their lending practices through the second half of this year – the orange line in the chart below jumping higher to be on a par with the Global Financial Crisis and the pandemic. This will become more pronounced through the first half of this year and will be a major headwind to economic activity. The chart below shows that when banks step back the economy suffers, with unemployment jumping higher. The most obvious transmission mechanism is struggling firms are more likely to be forced out of business if their banks no longer extend credit to them.

Tighter lending conditions always result in higher unemployment

Adding to our nervousness about the growth outlook is the lack of movement on the government debt ceiling. Failure to agree on a deal to raise this could result in a government shutdown and hundreds of thousands of workers furloughed with a potential technical default in the third quarter. On top of this, the Supreme Court is currently weighing President Biden’s plans on student debt forgiveness. Federal student loan payments have been on hold for the past three years and the President had hoped to cancel up to $20,000 in debt for up to 40 million Americans. If the Supreme Court rules against the President, typical monthly payments of $300-400 could restart from September, acting as another major brake on the economy.

A reversal of Fed rate hikes is coming

Yet despite all these negatives, the Federal Reserve seems intent on raising interest rates further with a 25bp hike more likely than not at the May FOMC meeting. Inflation continues to run hot for now, but with job lay-off announcements on the rise and the headwinds for the economy intensifying, the Fed’s concerns should gradually recede over the summer. Indeed, the composition of the inflation basket (high shelter and vehicle weighting where prices are coming under downward pressure) and surveys indicating that competitive pressures are making businesses more reluctant to raise prices means inflation will drop below 3% by year-end.

The tightening of lending conditions combined with rising borrowing costs, plunging business sentiment and a rapidly weakening property market mean a hard landing looks increasingly probable. With unemployment likely to rise, wage pressures will be dampened and inflation will slow even more quickly. This should open the door to 100bp of rate cuts in the fourth quarter with the Fed funds rate set to head down to 3% by mid-2024.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

ING Monthly: Everything, everywhere, almost all at once

- This bundle contains 16 Articles