A future solution to the inflation conundrum

- 1 November 2017

Could digital currencies be a game-changer for the low inflation puzzle?

On 1 November, ING hosts the launch of the 19th edition of the Geneva Reports on the World Economy, a joint effort by the Centre for Economic Policy Research and the International Center for Monetary and Banking Studies. This year the report will investigate the main drivers behind low inflation and the immediate consequences for economic research. In this article, we emphasize the potential role that central bank digital currency may play into the debate in the coming years.

Low inflation despite economic recovery

Why is core inflation not picking up despite increasing evidence of synchronized global growth? One thing to look at here are Philips Curves. These economic models examine the relationship between spare capacity in the labour market and inflationary pressures. Our eurozone team already highlights how different measures of domestic slack could explain different Philips Curve slopes.

Furthermore, there are clearly other global factors playing into the story here. Claudio Borio, the head of the Monetary and Economic Department at the Bank for International Settlement, emphasized the importance of globalisation. In a speech at the 87th Annual General Meeting, he said that global factors have risen in importance relative to domestic factors. To quote the economist, Charles Goodhart:: '...in an age of globalisation, migration and out-sourcing, why are economists still running country-specific Phillips curves?', in effect suggesting economists should be thinking on a much bigger scale when explaining the Phillips curve conundrum.

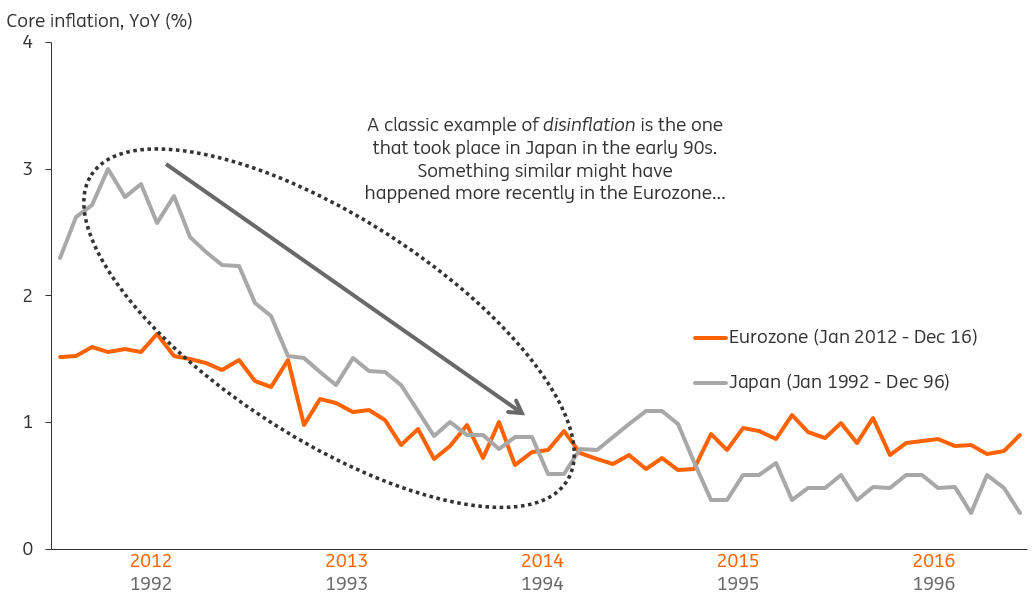

Disinflation similarities

A strong pick up in inflation is usually associated with a cyclical upswing in economic growth, while weak inflation is generally symptomatic of softness in economic activity. As an economy grows above potential, the demand for goods and services outstrips supply and producers can extract higher prices. Rising inflation can be particularly detrimental, especially for fixed income investments, as their coupon typically stays the same until maturity and the value of the principal remains fixed.

One way to protect against inflation is buying inflation-linked bonds. Equally, equities typically tend to rise with inflation in the very long run as higher prices often feed into higher revenues and profits, therefore helping equity valuations. Conversely, when the economy is running below potential, the same demand for goods and services eases relative to supply and firms adjust prices accordingly. The latter is known as disinflation. A classic example of disinflation is the one that took place in Japan in the early 90s. Something similar might have happened more recently in the Eurozone.

Does history repeat itself?

A classic example of disinflation that happened in Japan in the early 90s, and perhaps the eurozone more recently.

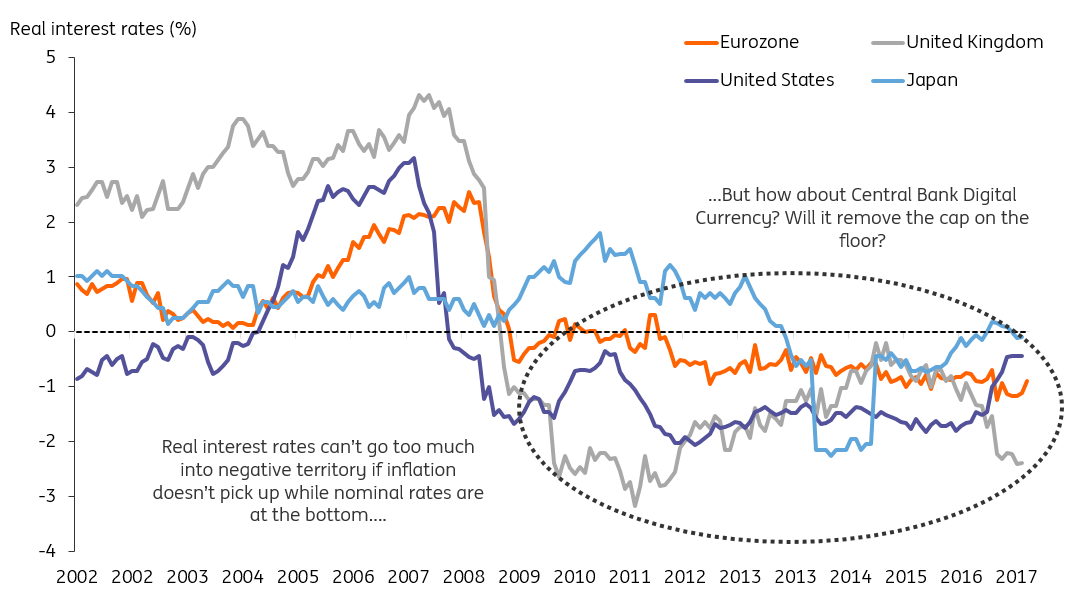

The zero-lower-bound and low inflation: a conundrum?

Typically, real interest rates struggle to move into negative territory with low structural inflation and a lower bound on nominal rates, therefore failing to provide sufficient expansionary stimulus to fight negative demand shocks. Hence, the reliance of central banks on unconventional monetary policies, such as negative marginal interest on reserves and quantitative easing. But with digital currencies, this could all be set to change.

Ben Broadbent, Deputy Governor at the Bank of England, stressed the importance of Central Bank Digital Currency (CBDC) for instance. In one of his speeches, he shows how CBDC may have the potential to reshape the financial system in its entirety, especially if it becomes a substitute for existing deposits. All this could have profound implications for the broader financial industry, including banks' maturity transformation, namely borrowing money short-term and lending long-term. Equally, Willem Buiter mentioned the abolishment of cash as one way to overcome the zero-lower-bound issue, since this allows banks to charge fees on accounts (negative interest rates) as electronic cash can't be hoarded under your bed.

Real rates struggle to move into negative territory with low inflation

Recent evidence suggests real rates went negative in the aftermath of the financial crisis, but the bigger question is: did they go far enough?

Looking ahead

As we already emphasized in our cryptocoaster note, in our view cryptocurrencies could tick all the boxes to replace existing money in the future, although it’s still far too early to map out all the immediate implications for the broader economy. Ultimately, the first step is to establish what are the consequences for inflation, price stability, regulation and monetary policy. Perhaps Central Bank Digital Currency could become the big theme of an upcoming Geneva Report in the near future.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more