A Dovish, but cautious shift from the Fed

- 19 June 2019

- United States

The Fed has opened the door to rate cuts, but it may not be as aggressive as the market expects. For now, we're sticking to our recently revised forecast for rate cuts in September and December, but if the data deteriorates and President Trump and President Xi's meeting next week goes badly, we're open to moving that to July and September

The Federal Reserve has opted to leave monetary policy unchanged, but as widely expected (and forewarned by Fed Chair Jerome Powell), has adopted a more dovish stance today. James Bullard, the St Louis Fed President, went further and voted for an immediate 25bp rate cut.

The market has taken this as a signal that a July 25bp rate cut is virtually a done deal with three more to come, but we are not so sure. The path of trade talks is critical and if there are some positive messages, if not actions, and the activity data holds up, the market will be disappointed. Moreover, the “dot” diagram of forecasters has a median of NO cuts this year and only one next year.

While the news in the near term is likely to get worse before it gets better, we think there are decent fundamentals. More importantly, we think President Trump’s desire to win re-election means that he will be wary of pushing too far for too long on trade, thereby damaging his own chances. We continue to look for two rate cuts in 2H19 and favour September and December.

A clear shift in language,

The big change in the accompanying statement is the dropping of the description of the Fed's stance as being “patient”. Instead, the Fed believes “uncertainties about the outlook have increased” which mean the FOMC will be “closely monitoring the implications of incoming information… and will act as appropriate to sustain the expansion”.

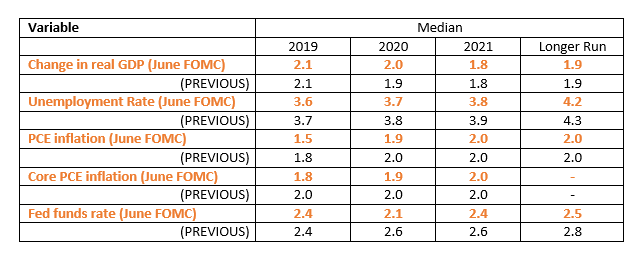

The current economic situation has also been downgraded from one that was “solid” in May to one that is “moderate” today. This is largely down to “soft” business investment, which is enough to offset the fact consumer spending “appears to have picked up”. Yet they have actually revised up their 2020 GDP growth forecast to 2% and lowered their prediction for unemployment. Meanwhile, market-based measures of inflation “have declined” and they have lowered their near-term forecast profile, but have headline and core inflation returning to target next year.

But not in forecasts...

The tone of this statement is clearly suggesting that rate cuts are in the offing and markets are increasingly confident that the first move will be in July with three more probable over the next year. Yet the “dot” diagram of predictions from Fed officials warns markets they perhaps shouldn’t get too far ahead of themselves. The median forecast is for NO rate change this year. Seven officials are looking for two 25bp rate cuts and one is looking for a single 25bp move. Eight expect no change while one individual is actually still penciling in a rate hike!

For end 2020, Fed officials are suggesting they may only need one rate cut thanks to the fact that one additional official is now looking for a single 25bp next year - no-one is looking for more than two rate cuts in total over the forecast period. The median then suggests that one cut is reversed in 2021 - returning the Fed funds target rate to its current level - with the longer run forecast for where the Fed funds rate settles has been lowered from 2.8% to 2.5%.

As such it’s dovish, but certainly not that dovish.

Federal Reserve median forecasts

All to play for

The press conference has allowed Fed Chair Powell to put a bit more colour on the situation, suggesting that the Fed will learn a lot in the near term - next week's G20 and associated trade discussions - and that the Fed should not overreact to individual data points. Nonetheless, even those officials that are forecasting no rate cuts acknowledge the case for action has strengthened.

We are sticking to our recently revised forecast for now, but if the data deteriorates further and President Trump and President Xi's meeting next week goes badly, we are open to moving that to July and September

We recently switched to a view that the Fed would cut rates twice this year – once in September and once in December on the basis that trade tensions are likely to get worse before they get better. This will weigh on sentiment, which could see firms pull back on investment and hiring, thereby threatening a broader economic slowdown and justifying precautionary policy easing.

We are sticking with this for now, but should the data deteriorate and next week’s meeting between President Trump and President Xi go badly, we are open to moving that to July and September. Should payrolls rebound to 250k next month, and trade discussions offer signals for encouragement it is the market that will have to move.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

What’s happening in Australia and the rest of the world?

- This bundle contains 8 Articles