A $20 billion tax boost to corporate India

- 22 September 2019

- India

Whether this helps to kick-start the economy is still to be seen. For now, the negative consequences of derailed fiscal consolidation on India's external creditworthiness keeps a weakening pressure on local financial assets. We retain our end-2019 USD/INR forecast at 73.50

| 3.9% |

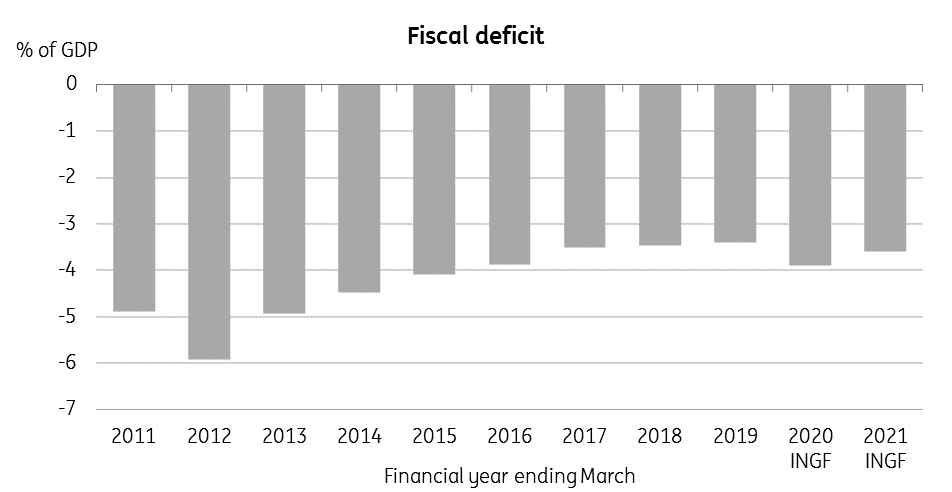

ING's fiscal deficit forecast for FY2020Revised up from 3.5% |

Unexpectedly big tax boost

In a surprise move last Friday, Finance Minister, Nirmala Sitharaman, announced a significant tax reduction for domestic companies. The move is estimated to cost about $20 billion to the government in lost revenue, includes a cut in the corporate tax rate to 22% from 30%, taking effect retrospectively from 1 April 2019, the start of the current financial year. This takes the effective tax rate after all additional levies to 25.2% from 25.9%.

In more incentives for new start-ups, for companies to be incorporated from 1 October 2019, the tax rate is set at 15%, down sharply from the existing 25%. Furthermore, reversing some of the tightening measures announced in this year’s budget, the government rolled back surcharges introduced on capital gains from the sale of securities, including derivatives, and exempted companies from share buyback taxes for buybacks before July this year. Also announced on Friday was a reduction in the Goods and Services Tax (GST) for some sectors.

Incessant stimulus

The latest round of fiscal boosts followed a slew of measures announced over the last month.

- 23 August: Withdrawal of surcharge on long and short-term capital gains tax on foreign portfolio and domestic investors; $9.8 billion (INR 700 billion) capital injection for public sector banks; lifting of curbs on new vehicle purchases by government departments.

- 29 August: Easing of foreign investment regulation for retail, manufacturing and coal mining sectors. Relaxing local sourcing norms for foreign companies selling their own brand in India. Removal of caps on investment in commercial coal mining. Up to 26% investment permitted in digital media.

- 30 August: Consolidating 10 public sector banks into four - A) Punjab National Bank, Oriental Bank of Commerce, and United Bank; B) Canara Bank and Syndicate Bank; C) Union Bank of India, Andhra Bank and Corporation Bank; and D) Allahabad Bank and Indian Bank.

- 14 September: $7 billion tax incentive for exporters. Measures to boost the real estate sector.

- 20 September: $20 billion corporate tax reduction for domestic companies (details as described at the onset). Reduction of GST on hotel rooms (18% from 28%) and catering services (5% from 18%), but a hike in that on caffeinated beverages (40% from 28%).

Near-term pain, long-term gain

The reduction in tax rate puts corporate India on par with Asian neighbours (standard rate of about 25% in most Asian countries, 17% in Singapore and Hong Kong), which is significantly positive for the economy over a longer-term.

Indeed, the latest measures should do what they are intended to – revive growth. But how quickly and effectively this will happen in the current climate of strong external risk remains to be seen. There is little that fiscal policy can do to overcome external hurdles to growth, in particular, the recent spike in global oil prices. With 80% of its energy requirement imported, India will have difficulty in keeping the oil price spike from affecting domestic fuel prices and overall inflation. On the domestic front, the still high level of personal income taxes of more than 30% and a decade-high unemployment rate are sapping the vigour of consumer spending - the key driver of GDP growth.

Where is the fiscal deficit headed?

Moreover, the aggressive stimulus adds to the economy’s long-term plight by further delaying fiscal consolidation. Certainly, the immediate implication will be a blowout of the fiscal deficit well above the government’s 3.3% of GDP projection for the current fiscal year.

The $20 billion worth of revenue loss from corporate tax measures (leaving aside other stimulus efforts announced over last one month) itself amounts to 0.7% of GDP, which on its own will swell the deficit to 4% of GDP. While some of this revenue loss will be shared by state governments and the central government may count on improved tax compliance due to lower rates as an offset, an additional whammy from slower GDP growth depressing revenue cannot be ruled out.

We are revising our deficit forecast for the current fiscal year from 3.5% to 3.9%, wiping out nearly all the deficit reduction over the last three years.

Derailed fiscal consolidation

What about financing?

There is no clarity about how the government will be financing this wider deficit. The $24 billion payouts from the RBI's coffer won’t be enough, nor can the government continue to rely on such monetization of the deficit.

The prospect of turning to global debt markets for financing remains clouded amid the prevailing uncertain market environment, more so now as the global investors will, in all likelihood, be viewing excessive fiscal loosening negatively. S&P has left no time in warning of the negative implications of recent fiscal actions. This is a further blow to the government’s plan to borrow overseas, which, in turn, means a greater strain on domestic debt markets where excessive government borrowing leads to crowding out of private investment demand – a recipe for continued sluggish GDP growth ahead. A vicious cycle could go on.

And RBI is ready to do more

The Reserve Bank of India’s (RBI) aggressive monetary easing with a total 110 basis point (bp) policy rate cuts implemented in four policy meetings so far this year has failed to arrest the growth slowdown. Last week Governor Shaktikanta Das assured markets of continued monetary stimulus for the economy through more policy interest rate cuts ahead. This makes another 25bp rate cut at the next bi-monthly policy review in early October almost certain. And there could be even more with our forecast of a further 25bp of cuts in December.

We identified growth as our highest priority in August. We have also maintained that it cannot be business usual now and the economy needs something more. Therefore, we went for 35 basis points cut in August. - RBI Governor Shaktikanta Das.

All this is potentially inflationary. But nothing matters beyond growth, at least while inflation is running below the RBI's 4% target.

Bottom line

Whether this helps to kick-start the economy is still to be seen. For now, the negative consequences of derailed fiscal consolidation on India's external creditworthiness keeps up weakening pressure on local financial assets. While more RBI easing is positive for the bond market, the negative from the supply overhang from a wider fiscal deficit is likely to outweigh this, and bond yields will remain under continued upward pressure. Last Friday’s market reaction with a strong rally in the stocks but a huge selloff of government bonds speaks for itself.

The INR did gain some ground amidst the positive swing in sentiment towards the equity market, though we don’t think this will persist given that currency will likely be undermined by weakening public finances, the renewed threat of higher oil prices leading to higher domestic inflation, and the persistently wide current account deficit.

We retain our end-2019 USD/INR forecast at 73.50 (spot 70.95).

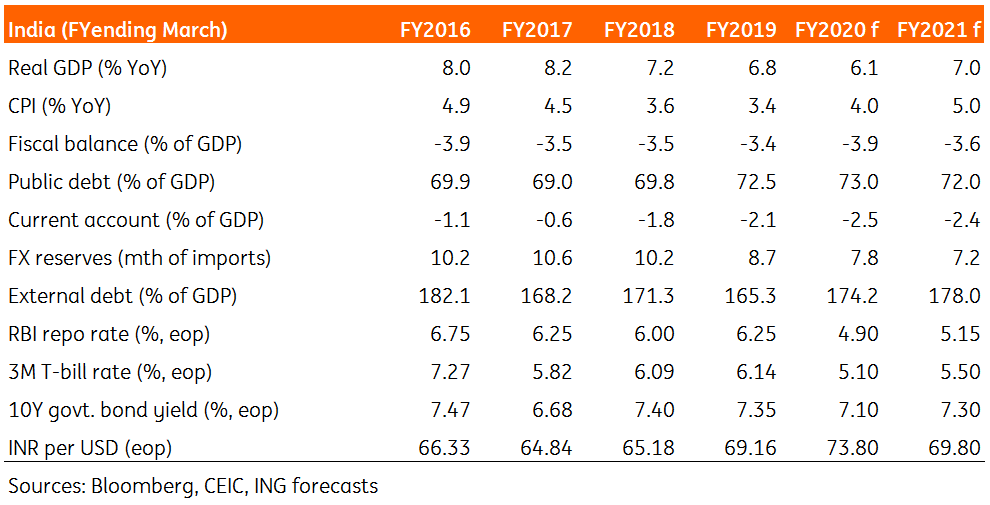

India: Key economic indicators and ING forecasts

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

In case you missed it: Two tribes go to war

- This bundle contains 7 Articles