US service sector price pressures cool as activity slows

The March ISM services index was weaker than predicted while price pressures moderated to four-year lows. With employment remaining in contraction territory this report should boost the case for interest rate cuts, but the breakdown in the relationship with official data means the Federal Reserve will remain wary of moving too soon

ISM reports cooling activity and inflation in the service sector

The March ISM services index is weaker than expected, falling to 51.4 from 52.6 and coming in below the 52.8 consensus. Out of the 52 forecasts submitted to Bloomberg, only one person predicted anything weaker than this outcome - remember that vehicle sales (yesterday) came in below everyone's expectations and construction spending (Monday) came in below everyone's expectations, but the strength in the ISM manufacturing survey has dominated the commentary and market direction since its release Monday morning.

The details show business activity holding steady at decent levels, but new orders cooled below the six-month average while employment remains in contraction territory as the backlog of orders fell markedly. Importantly, the prices paid component slowed meaningfully to a four-year low, although the press release noted that “respondents indicated that even with some prices stabilizing, inflation is still a concern.”

The ISM reports don't have the predictive qualities of old

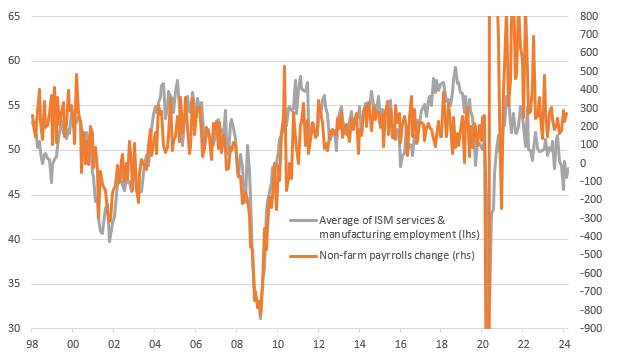

With both the manufacturing and the services ISM employment components coming in below 50 - indicating falling employment levels - this should in theory mean a soft payrolls print on Friday (the consensus is 213k), but the report has a mind of its own and doesn't correlate with anything right now. The chart below shows how the ISM employment components used to be a very good predictor of what payrolls would do, now they couldn't be further apart – we are at levels suggesting payrolls should actually be falling outright to the tune of perhaps 50k.

ISM employment components versus non-farm payrolls changes (000s)

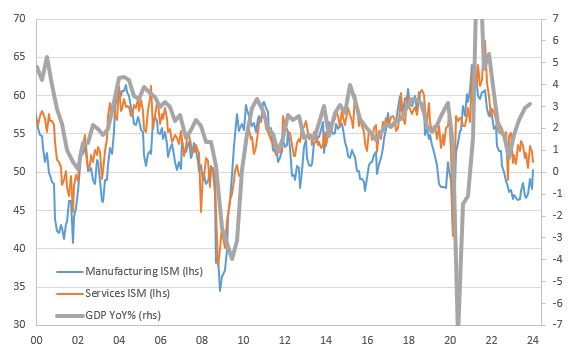

Likewise, the chart below shows how the headline indices from the ISM for manufacturing and services used to be a good indicator for where GDP growth would be heading, but again the relationship has failed since the pandemic. The ISMs are at levels historically consistent with the economy expanding at a rate below 1% year-on-year, not the 3%+ figure that official data tells us.

ISM headline indices versus GDP growth (YoY%)

The Fed needs to see cooling inflation and weaker jobs to be confident of being able to cut rates

These data discrepancies make the Federal Reserve’s job that much harder. For now, the market is leaning in the direction of things being too hot for substantial interest rate cuts with June seeing only a 60% chance of a 25bp rate cut. For the Fed to be comfortable to cut at that meeting we are likely going to need to see at least two 0.2% month-on-month core CPI prints between now and then (next week’s consensus forecast for March’s figure is 0.3%) with payrolls growth slowing towards 150k per month rather than the 236k averaged over the previous 12 months.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap