US retailers receive a summer boost

While auto and gasoline station sales fells heavily in June, there was significant strength elsewhere that provided an equal offset. It may be that the weather has boosted retail footfall as people try to escape the heat, but there are still challenges for the sector from weak real income growth, a run down in savings levels and high borrowing costs

Retailers beat expectations in June

The June US retail sales report is certainly stronger than expected although headline sales on the month were still only flat on the month. The consensus was for a 0.3% month-on-month drop and the May figure was revised up two tenths of a percentage point to 0.3% MoM growth. The details show motor vehicle sales fell 2% MoM, which was broadly in line with the auto volume sales, which we already knew. Gasoline station sales fell 3% MoM due primarily to lower prices while sporting goods saw sales dip 0.1%.

However, all other areas were strong. Non-store (largely internet) saw sales rise 1.9% MoM, building materials jumped 1.4%, clothing and furniture both increased 0.6% with health and personal care up 0.9%. It may be that hot, sticky weather has incentivised households to spend more time in the AC controlled environments of retail stores and shopping malls and that has helped to lift sales somewhat. We will see if the weather has tempered some of the services data next week when we get the full consumer spending breakdown.

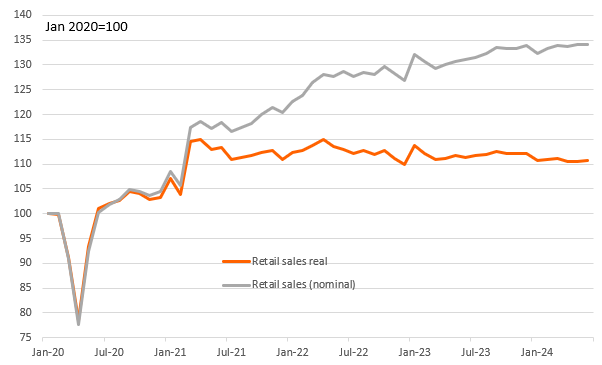

Nominal and real retail sales levels (Jan 2020 = 100)

Nonetheless, the data reflects nominal US dollar value changes. The chart above shows that real (volume) terms retail sales remain around 4 percentage points below their 2021 peak and it is volume growth that matters for GDP – the advanced second quarter estimate is released next Thursday. Moreover, retail sales as a proportion of total consumer spending is converging on the pre-pandemic trend after having spiked in 2020 and 2021.

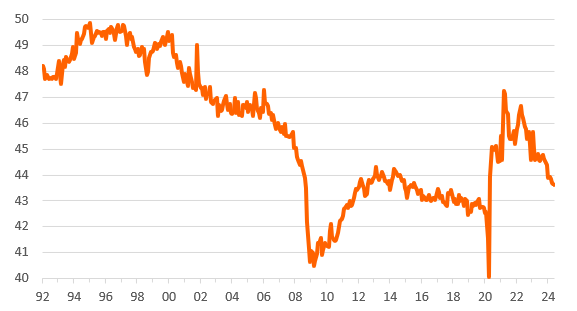

Retail sales as a % of total consumer spending

Challenges remain with spending set to revert to slowing trend

Next week’s GDP report is set to confirm that the run rate on real consumer spending growth has halved between second half 2023 and first half 2024 and we expect it to cool further through the rest of this year. Flat real household disposable incomes are constraining spending power while the exhaustion of pandemic-era accrued savings means there are fewer resources from this pot to keep spending going. High consumer credit costs make borrowing to fund spending painfully expensive too. Coupled with declining consumer confidence readings amid rising unemployment rates and it all points to a consumer sector that is becoming more cautious.

Slower consumer spending growth, moderating inflation and an upward trend in the unemployment rate are the ingredients needed to justify the Fed moving policy to a slightly less restrictive position from September.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap