US: Not let up in the pace of lay-offs

US initial jobless claims rose 6.6m last week, bringing the total to 16.8m over the past three weeks. This is on its own could push the April unemployment rate up to 14%, but with more job losses likely in coming weeks, it will peak even higher

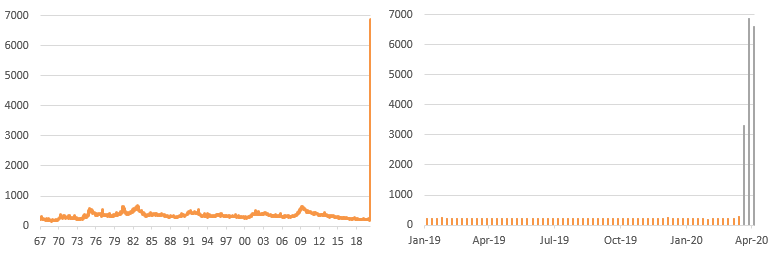

| 16.8m |

The number of jobless claims in the past 3 weeks |

Jobless claims came in at 6.606m for the week of 4 April after an upwardly revised 6.867m for 28 March. This was well above the 5.5mn consensus expectation and highlights the fact that there has been no real let up in the pace of lay-offs as the Covid-19 containment measures spread and intensify across the country. Continuing claims also climbed, but we have to remember that these come with an extra week of lag – for 28 March they came in at 7.455m.

US weekly initial jobless claims

With employment plunging and unemployment surging we should be prepared for a new post-war record high in the unemployment rate. It hit 10% at the peak of the Global Financial Crisis and 10.8% in 1982. With employment having fallen 16.8 million over the past three weeks based on jobless claims (since the data were collected for the March employment report) we estimate that the US unemployment stands today at around 14%. This is versus 4.4% in March and 3.5% in February. In all likelihood millions more of undocumented migrant workers can be added to this number.

That said, we remain hopeful that the fiscal stimulus, with initiatives to encourage employers not to lay-off staff – will start to bear fruit and keep unemployment below the 20% figure Treasury Secretary Mnuchin feared ahead of the package agreement.

When we finally get through the crisis and we can head on the path towards “normality”, unemployment will not fall as rapidly as it spiked. There is likely to be a rolling withdrawal of the restrictions, a process that gets underway in Austria and the Czech Republic next week, meaning a slow return to business as usual. Many companies will not make it through the crisis due to the plunge in demand and others will restructure and come out requiring a smaller workforce. As such the need for additional fiscal support for affected households and businesses seems a virtually certainty.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap