- Quick take

- 17 March 2022

- Manufacturing, Construction and Retail United States

US manufacturing posts solid growth

US manufacturing continues to perform well outside of the well-documented strains in the auto sector. Rising new orders and an increasing backlog of orders imply production will remain robust through the year while elevated oil and gas prices will stimulate more drilling and further boost industry's contribution to economic growth

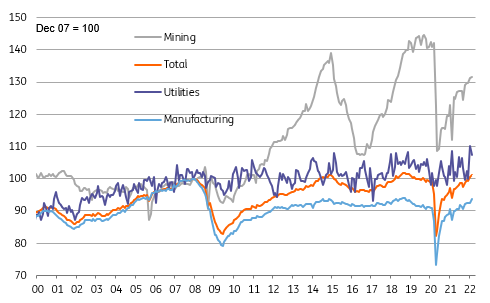

US industrial production rose 0.5% month-on-month in February, meeting expectations, but within the details a slightly stronger story emerges. Manufacturing output rose 1.2% month-on-month, ahead of the 1% consensus expectation, while oil and gas drilling was up 3.4% month-on-month in response to higher prices. Mining output overall was up 0.1%, but utilities output fell 2.7% due to more seasonal weather after a very cold January that prompted a 10.4% surge in demand as people tried to keep warm.

US industrial output levels by component

Stripping out the weather-related drop in utilities, this is a very solid report with broad-based strength. The one area of weakness was motor vehicles, where the supply chain strains focused on chip shortages are well documented. Output for vehicles and parts fell for a third consecutive month with year-on-year output at 0%. Excluding vehicles, US manufacturing was up 1.5% month-on-month, 7.9% year-on-year.

After another large monthly increase, oil and gas drilling is up 47.4% year-on-year, and given the spike in prices and renewed government enthusiasm for exploration, this component is likely to remain an important contributor in the months ahead. This will certainly be the case for March, with Baker Hughes numbers on US oil and gas rig count at 663 in mid-March versus 588 at the start of the year.

Overall, the US economy has clearly brushed off the effects of Omicron with consumers re-engaging and US industry performing strongly. Given the Federal Reserve’s bolder, more assertive stance with regards to normalising monetary policy, the odds of a 50bp rate hike in May will continue to build – although geopolitics underscores the Fed’s need to be “nimble”.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more