US jobs market reverting to pre-pandemic norms

Job openings improved, but the trend is still softening. At the same time the soft quits rate suggests the jobs market has normalised and means that inflation pressures emanating from the jobs market should continue to cool, keeping the door open for rate cuts later this year

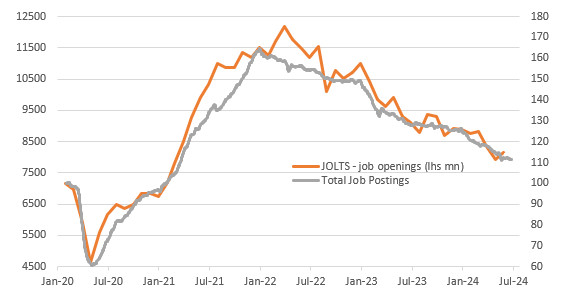

Job openings rise, but the trend is softening

Job openings rose to 8140k in May from a downwardly revised 7919k in April. This is above the 7946k that was expected. We use the Indeed job website’s total job postings numbers as a guide when we put our forecast for job openings together and as the chart below shows, the series tends to fluctuate around where Indeed’s numbers are. The trend remains one of shrinking vacancy numbers with the US economy tending towards pre-pandemic levels and likely hitting that point before the end of this year.

Job openings versus Indeed job postings

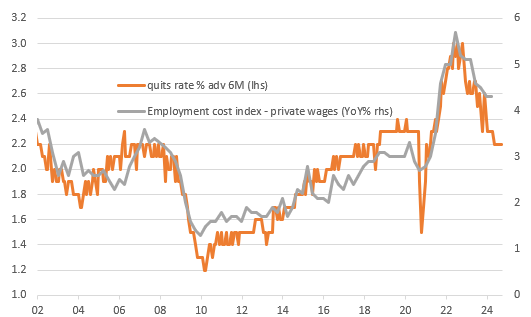

Quits rates points to slower wage growth and inflation

The quits rate was the big warning signal of an impending spike in labour costs that ensured inflation took off in 2021 and remained elevated ever since. As firms looked to rehire as the economy re-opened, firms were having to pay up to attract staff and this incentivized workers to move to new employers. In turn, as companies experienced higher staff turnover we saw bosses being more prepared to raise pay to retain staff. However, the swing sharply lower in the quits rate suggests that the jobs market is cooling with firms less willing to pay up to recruit staff or workers themselves becoming more reluctant to move. This is already prompting a slowdown in employment costs that we think will intensify through the second half of the year, as suggested in the chart below, and help to slow inflation pressures in the economy more broadly.

Quits rate & employment costs YoY%

Data still on track for a September rate cut

This all follows on from some tentatively dovish comments from Fed Chair Jerome Powell, who has been speaking at the ECB’s Forum on Central Banking in Sintra, Portugal. He acknowledged that the economy and jobs market has been strong, but that inflation is showing “signs of resuming its disinflationary trend” together with a “rebalancing in the labour market”. He refused to be drawn on the timing of any potential rate cut, but markets are now pricing around a 75% chance of a cut at the September FOMC meeting and we agree.

If we get another couple of 0.2% month-on-month or below core inflation prints, unemployment breaking above 4% and more evidence of cooling consumer spending growth, we believe the Fed will start to move monetary policy from restrictive territory to “slightly less” restrictive territory in 25bp increments down to around 4% by mid-2025.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap