- Quick take

- 10 January 2020

- United States

US jobs: December dampener

Jobs growth was weaker than predicted in December, with 2019 being the weakest year for job creation since 2011. Add in the much softer wage number and today's report reinforces our sense that 2020 will merely be a respectable, rather than spectacular year for consumer spending

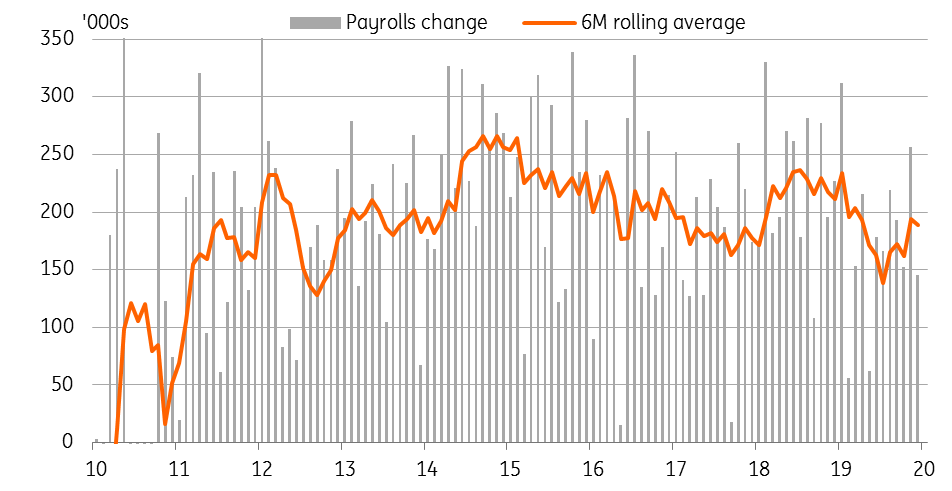

| 145,000 |

Increase in non-farm payrolls in December 2019weaker than the 160,000 consensus |

Jobs growth slows at year-end

The December US jobs report shows 145,000 jobs were created last month, which was a touch weaker than the 160,000 consensus, while there were a net 14,000 downward revisions to the previous couple of months.

The details have manufacturing jobs shrinking by 12,000 after the major swings seen in October and November relating to the recent strike action by GM staff. We continue to be concerned about the prospects for jobs here given the weakness in business surveys, such as the ISM.

Construction was up 20,000 and is likely to continue being a positive contributor given growing optimism in the housing market (NAHB home builder sentiment at record highs).

Private services gained 140,000 (strong retail, weak professional services), which was the smallest gain since July. Rounding it out, government employment rose 6,000.

Monthly US payrolls growth

Key job stats: Something for everyone

Jobs created in 2019: 2.11m (weakest since 2011) vs 2.68m in 2018

The last decline in payrolls was September 2010

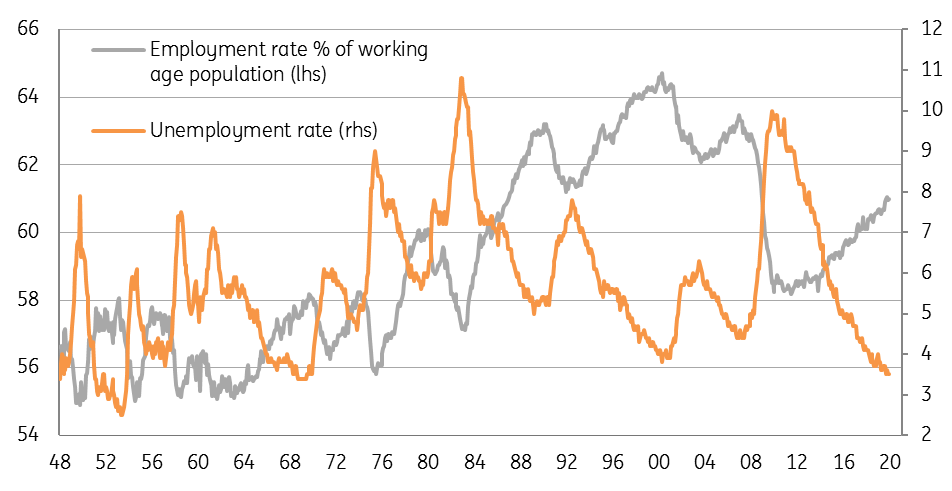

Unemployment rate lowest since December 1969

Wage growth of 2.9% year-on-year the weakest since July 2018

Unemployment is low, but employment ratio is too...

Weaker wage growth points to subdued spending

The clear disappointment is wages. Despite all the talk of a tight jobs market and companies struggling for staff with the right skill sets there is little evidence of labour costs being bid higher. Wage growth actually slowed to 2.9%, the weakest since July 2018. With employment gains likely to slow further in 2020, weaker real wages underline our view that softer consumer spending growth is going to be a key factor that leads to GDP disappointing in 2020.

Moreover, while the unemployment rate remains at its lowest level since December 1969, this doesn’t tell the whole story with regards to how “tight” the labour market is. After all, the proportion of the working age population that has a job is still below the rates seen in the depths of the recessions in the early 1990s and early 2000s. There is a significant chunk of the US population that is simply not engaged. If these people can be incentivised and re-skilled, this could be a resource that keeps the US expansion going for longer.

Fed to remain on hold

Overall, the report highlights the two-speed nature of the US economy where manufacturing continues to struggle and the service sector is performing relatively well. In aggregate, jobs continue to be created in decent numbers, but there is little wage inflation despite apparently tight labour markets. Today’s figure merely reinforces the message that with the Federal Reserve seemingly content with its current monetary policy stance, the prospect of any near-term interest rate moves appears remote.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more