US employment costs reacceleration incentivises the Fed to be more hawkish

US labour costs accelerated in the first quarter, led by the government sector, while hikes to state minimum wage levels contributed to higher private sector labour costs. This is the Federal Reserve’s favoured measure on labour market inflation pressures and provides further ammunition to justify a hawkish shift at tomorrow’s FOMC meeting

Labour costs reaccelerate more than expected

We have seen a big jump in the US 1Q employment cost index of 1.2% quarter-on-quarter versus 0.9% in 4Q23, well above the 1% expected and above every single individual forecast in the Bloomberg survey. Not a good look as this is the Federal Reserve's favoured measure of labour costs, and given labour costs are the biggest cost input in a service sector-led economy, such as the US, it can help to keep price pressures elevated. This reinforces the prospect of hawkish messaging from the Fed tomorrow.

The details show the strength was primarily led by the government sector where wage and salary growth rose from 4.7% year-on-year to 5% YoY while for the private sector, wages and salaries remained at 4.3% YoY with overall compensation continuing to grow 4.1% YoY. In terms of QoQ rates, government worker compensation rose 1.3% versus 1.0% in 4Q23 while private industry compensation rose 1.1% versus 0.9% in 4Q 23. It is likely that a decent hike in minimum wages in around half the US states was the primary driver. The increase in minimum wage to $20/hour for California fast food workers will hit in 2Q.

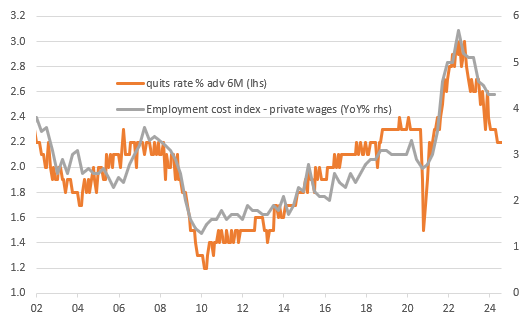

A slowing quits rate still indicates a cooling later in the year

The encouraging thing for the Fed is that the quits rate, published within tomorrow’s job opening report, continues to point to a broader moderation in labour costs in coming quarters. It peaked at 3% of all workers quitting their jobs to move to a new employer in early 2022, but this has slowed markedly over the past 18 months. This suggests that the new jobs on offer are not especially attractive (either through the role on offer or the pay rate) and more people are choosing to stick with the job they have. In turn, if employers are seeing less turnover in staff, there is perhaps less incentive to offer bumper pay awards to retain staff. Essentially, the numbers still point to the labour market price pressures gradually easing through the rest of the year.

Slowing quits rate suggests easing wage pressures... eventually

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap