UK services inflation rises but underlying story is improving

Don’t be fooled by the latest rise in UK services inflation. It’s largely down to base effects and faster price growth in categories the Bank of England is less bothered about. The underlying story is slowly improving and we think that means faster rate cuts through the winter, even if we’re expecting no change at tomorrow’s meeting

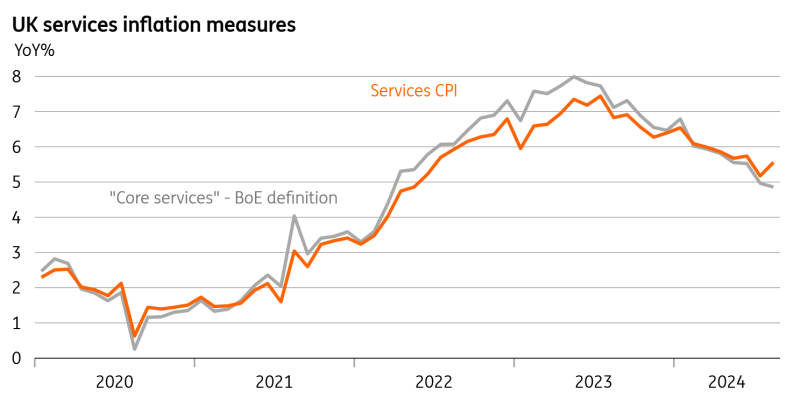

Beneath the surface of the latest UK CPI report, there are signs that the inflation story is slowly but surely moving in the right direction. That might sound weird, given that services inflation rose from 5.2% to 5.6% in August. Remember this is the guiding light for the Bank of England when it comes to rate cuts, and although today’s move was widely predicted, it looks like it is moving in the wrong direction.

Appearances can be deceiving. The fact is that the recent nudge higher in services inflation is largely thanks to base effects and higher inflation in price categories the BoE appears to care less about. We’ve calculated a measure of “core services” inflation, based on something the Bank put in its May Monetary Policy Report.

That excludes volatile categories like airfares, package holidays, and rents, arguably less relevant for monetary policy decisions. If our maths is correct, that’s now fallen to 4.9% from 5.5% just two months ago.

The BoE's 'core services' inflation measure actually fell in August

Admittedly there is nothing in these latest numbers that’s likely to move the dial at tomorrow’s rate decision. Overall, services inflation is, despite the recent pickup, still slightly below the BoE’s August forecasts, but only just.

For now, the committee seems happy with one rate cut per quarter for the time being, even if it hasn’t said so explicitly. That suggests the next cut is likely in November, and tomorrow we doubt we’ll get any clear signals on what the Bank intends to do thereafter.

Remember that the Bank’s hawks are concerned that price and wage-setting behaviour might have changed in such a way that negates the need for substantial rate cuts. And while we don’t think that’s the majority view on the committee right now, so long as services inflation and wage growth remain sticky, they seem content with moving slowly.

Still, there are good reasons to think the inflation story should continue to improve into year-end. Officials aren’t likely to be fazed by headline CPI, which could inch closer towards 3% later this year, thanks to a diminishing drag from lower energy prices. It's currently at 2.2%. Remember that the energy regulator has already announced that the household price cap on electricity/gas prices will rise by roughly 10% in October.

Strip that out, however, and we think services inflation will dip below 5% at the start of next year. The Bank of England’s survey of businesses is showing consistent falls in both expected and realised wage/price growth. Coupled with the ongoing cooldown in the jobs market, we think the broad consensus at the BoE will shift in favour of faster rate cuts through the winter. We expect back-to-back rate cuts from November onwards, taking the Bank Rate down to 3.25% by next summer.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap