UK PMIs point to brighter growth outlook but stubborn inflation

Unlike the eurozone, the UK's service sector is picking up steam. The issue for the Bank of England is that inflation is also proving sticky, and the PMI highlights the disruption in the Red Sea. Today's data adds to the case for the Bank of England to wait a little longer before cutting rates. We expect a cut in August

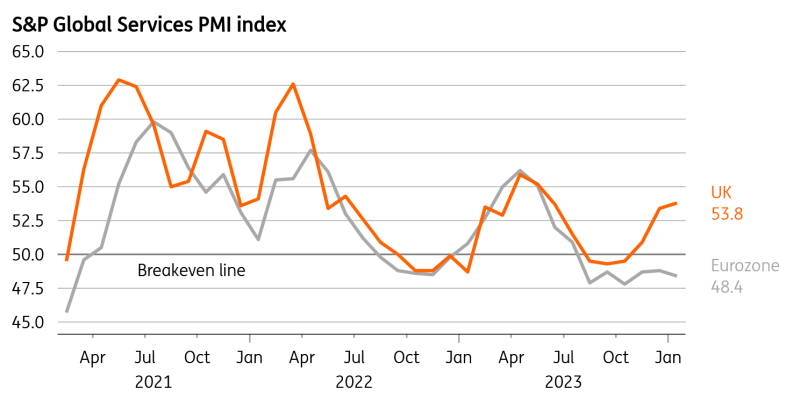

The UK service sector, which accounts for the lion’s share of economic output, edged further into growth in January, according to the latest purchasing manager’s index.

What’s particularly interesting is that this extends a recent trend whereby UK service sector growth is apparently accelerating at a time when the equivalent eurozone index is edging further into contraction (though Europe’s manufacturing sector appears to be bottoming out). Before last autumn, the UK’s services PMI had largely tracked what was happening in its closest neighbours.

This is another signal that the consensus among economists going into this year, which suggests the UK will underperform most major European economies in 2024, looks a bit too gloomy. While the recent sharp fall in market rates is good news for all economies, in the UK it makes a particular difference to the mortgage squeeze given the relatively high share of households due to refinance this year (around a fifth). Other economies, like France and the US, have a higher prevalence of much longer fixed-rate mortgage products. The anticipation of Bank of England rate cuts also looks highly likely to translate into more tax cuts in the spring, with the Chancellor set to be gifted with around £12bn extra “headroom” to spend whilst still meeting his fiscal rules.

The UK's services PMI has started to diverge from the eurozone

When it comes to rate cuts, the reality is that the BoE is putting relatively little weight on activity data right now. And on inflation, the press release from S&P Global contains a few sentences that policymakers won’t want to hear.

There are reports of increased input cost pressures following the Red Sea disruption. It’s worth emphasising though that the PMI is a diffusion index, so it tells us that more firms than before are reporting higher cost pressures, but it doesn’t say anything about the magnitude of the price rises. For now, we don’t think the Red Sea crisis will make a decisive difference to the UK inflation outlook. It may slow the decline in core goods inflation, but ultimately we still expect headline CPI to dip below 2% in April.

The PMI also notes ongoing wage pressures in the service sector, and this echoes the BoE's survey of Chief Financial Officers (CFOs) which suggests pay growth expectations have been stuck around 5% for several months now.

All of this serves as a reminder that the BoE won’t be rushed into rate cuts this year. Its new forecasts next week will reflect an inflation backdrop that is much improved since the last projections in November. But the committee will want to see more progress on services inflation and wage growth before acting, while a large tax cut package in March would probably be another reason to hold rates higher for a little longer.

Our base case is for an August start to rate cuts and 100bp of easing in the second half of the year. Markets have more-or-less aligned with this view too.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap