UK inflation shock raises chance of June rate hike

UK inflation came in way higher than expected in April, which undoubtedly puts pressure on the Bank of England to hike by another 25bp in June

UK inflation has come in higher than pretty much anyone, including members of the Bank of England's committee, expected in April. Headline inflation came in at 8.7%, higher than the 8.2% consensus. Core inflation picked up from 6.2% to 6.8%. This undoubtedly makes life harder for policymakers and no doubt raises the chance of yet another 25bp rate hike in June.

Of course, April's headline figure was still much lower than it was in March. That's a well-telegraphed effect of last April's 50% surge in electricity/gas prices dropping out of the annual rate. By July, when consumer bills are set to fall by roughly 20%, utilities will be contributing almost nothing to the overall inflation rate – and by October, will be a net drag.

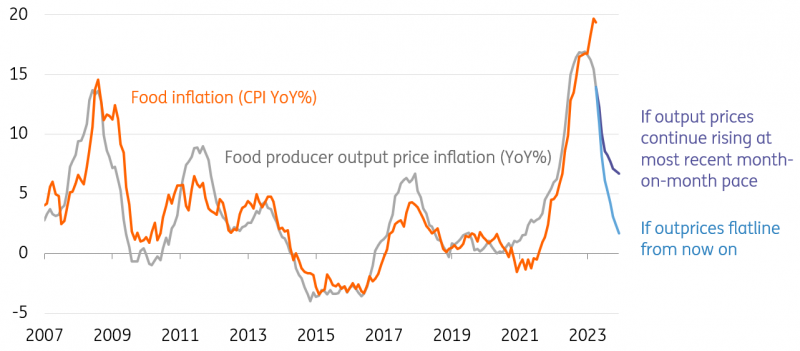

Instead, it's food prices that are now the biggest headache. We're now in an unusual situation where food inflation – at around 19% YoY – has diverged noticeably from the relevant producer output price measure. The latter has undoubtedly peaked on a year-on-year basis. Assuming the most recent month-on-month increases in output prices were to continue through the remainder of this year, it implies that food inflation should be back to the 6% area or below by Christmas.

In practice, we doubt the deceleration will be that aggressive, but there are nevertheless good reasons to think that food will be contributing less to overall inflation by the end of the year.

Consumer and producer food inflation is diverging

Ultimately though, what matters for the Bank of England is services inflation, and that edged up to 6.9% from 6.6% previously – higher than expected. Much of this seems to be down to firms making more widespread changes to prices that are typically reset on an annual basis. Some of this was expected, for example, telecoms prices typically change this time each year. But there were some surprises, including rents which rose by 1.4% on the month, which was the highest month-on-month increase in more than a decade.

There are good reasons to think services inflation is at its peak, and we think the fall in gas prices should alleviate one major source of cost pressures in the sector. Nevertheless, this latest data raise the chance of another rate hike next month.

It's not a foregone conclusion, not least because we still have another set of data before the meeting, and remember the jobs/wages data has been moving in the right direction, as have broader survey measures of price-setting behaviour. If nothing else, market pricing, which on the back of this data is now pricing more than three additional hikes from the BoE, looks too aggressive.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap