UK growth slows over summer after remarkable first half

The UK economy grew in August, but the pace of growth is slowing after a short-lived burst of activity earlier in the year

The UK economy had a remarkable run through the first few months of 2024, at least if the monthly GDP figures are to be believed. But those same figures now show that this strength was short-lived.

While monthly GDP increased by 0.2% in the month of August, that followed two months of no growth at all. Averaging that out and comparing the latest three months of activity to the three prior, growth now stands at 0.2%. That’s down from a hefty 0.7% in the spring.

That might sound worrying, but the reality is these figures have been extremely volatile over the past few months. When we look at what drove all that strength, which was concentrated specifically in January and March, much of it was in sectors that are less tradeable or less tangible, which are less obviously connected to the health of the consumer or the wider global environment.

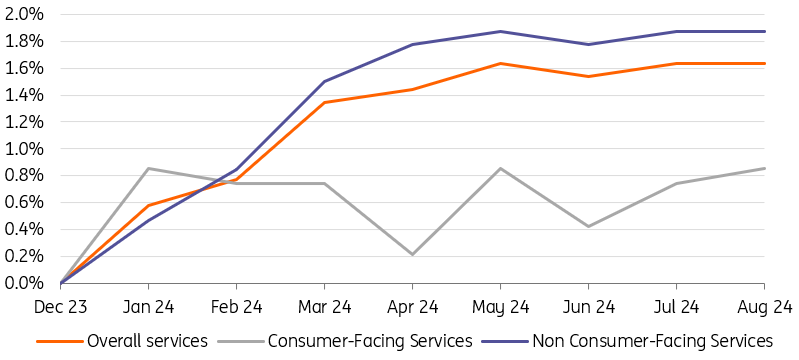

Consumer-facing services, which include retail and hospitality, have collectively grown by 0.9% since last December. That is respectable and above all reflects the UK’s sticky nominal wage growth, set against headline inflation that is now close to 2%, having taken longer to fall back than in other parts of Europe. Still, that growth rate is less than half the pace recorded in non-consumer-facing services, where output has increased by 1.9% since the turn of the year.

Growth more visible in non-consumer services this year

The bottom line is that the economy still seems to be growing at a reasonable pace, but the 0.6/0.7% quarterly GDP readings we became accustomed to in the first two quarters of the year are not going to be repeated in the second half of the year. We’re looking for 0.2% growth in the third quarter overall.

That has two main implications for policy. Firstly, it suggests the Bank of England was right to take those stronger first-half growth figures with a pinch of salt. It could have conceivably used those better figures as an opportunity to revise up its growth forecasts for the next couple of years, but it rightly has chosen not to do so.

That means next week’s services inflation figures will be more important. We think this should start to undershoot BoE forecasts, which is likely to accelerate policy easing. We expect cuts in both November and December.

Secondly, if the Treasury was hoping the stronger first-half growth would unlock some extra fiscal headroom in the forthcoming budget, then it is likely to be left disappointed. Remember the key here is what the Office for Budget Responsibility projects for the UK economy. And like the BoE, they are unlikely to take much inference from the GDP figures so far this year. Indeed, if anything the OBR forecasts already sit at the more optimistic end of the spectrum.

Take a look at our latest ING Monthly for our initial thoughts on the forthcoming budget.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap