Improvement in Turkey’s deficit loses momentum

The improvement in the current account deficit in March was attributable to the continuing recovery in the foreign trade deficit. But the downward trend that started after the peak last July has lost momentum, with only a slight decline in the 12-month rolling deficit over the previous month

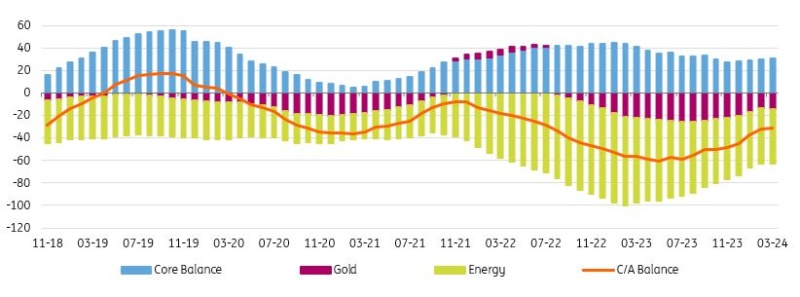

The current account in March posted a deficit of US$4.5bn, while the improvement in the 12-month rolling deficit, which followed a faster pace in the first two months of the year, lost momentum with a modest decline to US$31.2bn (translating into c.2.8% of GDP) from US$31.9bn a month ago.

Current account (12M rolling, US$bn)

In the breakdown, compared to the same month of last year, we see:

- A continuing recovery in the energy balance with a fall in the deficit to US$3.8bn from US$4.6bn.

- The core trade balance has moved into surplus at US$0.1bn from a slight deficit of US$0.5bn.

While these two items determined the improvement in the current account, the widening gold trade deficit, slightly lower services and primary income limited the extent of the decline.

Breakdown of current account (year-to-date, US$bn)

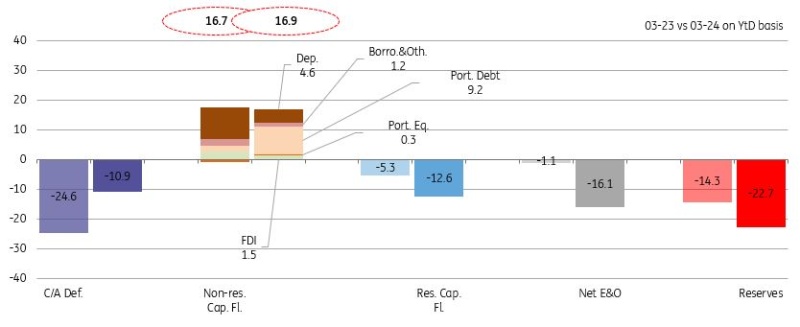

On the capital account, net identified flows remained weak with a mere US$3.8bn of inflows, falling short of the current account deficit again, following mild outflows a month ago. Errors and omissions outflows recorded significant outflows ahead of the March local elections at US$9.6bn, similar to what we saw during the financial volatility of December 2021 (US$10.6bn) and before the May 2023 presidential election (US$9.6bn). With the monthly current account deficit and weak flow outlook, official reserves recorded a US$10.3bn.

In the breakdown of monthly data, non-residents’ movements drove the inflows with:

- US$2.3bn deposited by foreign entities in the banking system

- US$0.7bn of trade credits

- Continuing Eurobond issuances of banks at US$1.2bn and

- Net borrowing at US$1.4bn. In March, rollover rates stood at 121% for the corporates and 161% for the banking (vs 97% and 123%, respectively on a 12-month rolling basis).

- Non-debt creating foreign inflows, standing at US$0.7bn thanks to (gross) FDI at US$0.4bn and purchases in the equity market at US$0.2bn.

- Residents’ movements drove the outflows with portfolio investments at US$1.5bn, and outward FDI at US$0.6bn.

In the first quarter of 2024, no-resident inflows remained broadly unchanged in comparison to the same period of 2023 at around US$17bn, while asset acquisitions of locals abroad increased which contributed to a decline in net identified flows (US$4.3bn US$11.4bn last year). Outflows via net errors and omissions jumped to US$16.1bn vs US$1.1bn last year. Despite a strong recovery in the current account balance from US$-24.6bn to US$-10.9bn, official reserves plunged by US$22.7bn vs the US$14.3bn decline last year.

Breakdown of financing (year-to-date, US$bn)

Overall, the improvement in the current account deficit in March was attributable to the continuing recovery in the foreign trade deficit, though the downward trend that started after the peak last July has lost momentum. The provisional customs data released by the Ministry of Trade reveals that the foreign trade deficit increased by around 13% to US$9.9bn in April. The data implies a temporary increase in the current account as the impact of the recent central bank tightening on the balancing of demand factors is likely to be supportive for the external outlook. Additionally, the ongoing recovery in global economic activity is expected to have a favourable impact on Turkey's exports and thus on the c/a balance. On the flip side, the rise in global commodity prices, particularly energy prices, may limit the slowdown in imports. On the capital account, the turnout was relatively weak in the first quarter, though recent data shows a re-acceleration of inflows due to the increasing appetite for Turkish assets from foreign investors on the back of the clear messages of the CBT and the government regarding the continuation of tight monetary and fiscal policies.

On the fiscal side, the Minister of Treasury and Finance, Mehmet Şimşek, announced a package of measures, which include cutting purchases of goods and services and investment spending to control the widening in the budget deficit and to help disinflation while he signalled additional actions in the period ahead. Accordingly, the government targets a budget deficit-to-GDP ratio this year close to the level realised in 2023 (5.2%) or lower. Simsek’s signal of increased support from fiscal policy for disinflation hints that the government prioritises spending freezes to control the fiscal deficit rather than revenue-boosting actions in the short term, and hence, there will not likely be a significant correction in electricity and natural gas prices until inflation is on a notable downward trend.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap