Turkey: Services continue to drive current account improvement

The current account balance continued to improve in August, driven mainly by an improving services balances. Tourism and transportation revenues helped, as did a lower foreign trade deficit.

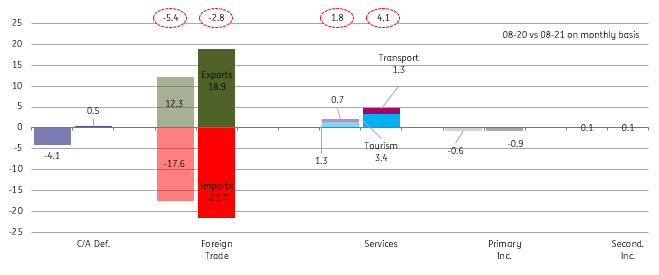

With a better than expected August figure at US$0.5 bn (vs US$-0.1 bn market consensus), the current account balance has continued to improve. This has been driven by (i) a recovery in tourism revenues, though remaining below pre-covid levels, and (ii) softer core and gold imports supporting an improvement in the goods balance despite the ongoing uptrend in energy bills. Accordingly, the narrowing trend in the 12M rolling figure has remained intact with a further drop to US$23.0bn (c. 3.0% of GDP) from US$27.6 bn a month ago.The Central Bank of Turkey revised the 2020 figure down to US$35 bn, from US$37.3 bn previously.

Breakdown of current account (US$ bn, on monthly basis)

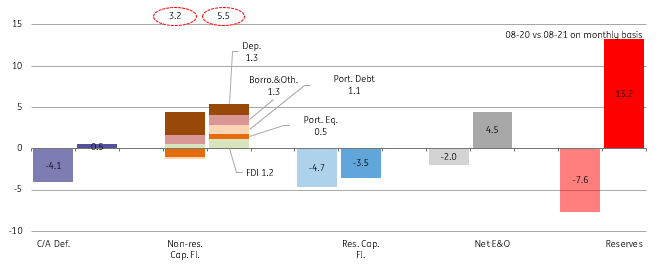

The capital account was stronger by US$8.3 bn in comparison to the inflows in recent months, driven by the IMF’s SDR allocation at US$6.3 bn. Including higher net errors & omissions at US$4.5 bn, the monthly c/a balance and capital account, official reserves saw further accumulation, by US$13.2 bn.

On year-to-date basis, we saw: i) some improvement in (gross) FDI flows at US$7.0 bn vs US$5.3 bn in the same period of 2020, ii) non-resident portfolio inflows standing at US$5.1 bn vs. outflows of US$15.4 bn in the equivalent period of last year, iii) accelerating unidentified inflows at US$13.5 bn vs US$8.8 bn outflows, iv) trade credits up by US$5.7 bn vs a US$4.4 bn decline in the first eight months of last year, v) a net US$2.8bn borrowing by banks and companies vs US$7.5 bn net repayment, vi) residents taking US$11.9 bn of their assets abroad vs US$0.4 bn brought to Turkey last year between January and August, and vii) regarding international reserves, an increase of US$27.2 bn on the back of the CBT’s swap arrangements, the export re-discount scheme, Euro bond issuance and IMF’s SDR deployment vs a drawdown of US$39.0 bn in the same period of 2020.

Breakdown of capital account (US$ bn, on monthly basis)

Overall, the current account remained on its narrowing path in August, driven mainly by improving services balances. This was thanks to the supportive impact of tourism and transportation revenues and a lower foreign trade deficit. While there is a consensus that external balances will remain on a narrowing track, with high foreign demand and a much better tourism season, the core trade deficit and particularly the pace of core imports will likely determine the extent of improvement in the period ahead. Regarding flow outlook, excluding the IMF boost, capital inflows were relatively sluggigh in August . September will likely see further weakness, with accelerating portfolio outflows following the CBT’s suprise move and dovish guidance as well as risk-off sentiment towards emerging markets in general.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap