Turkey sees slow adjustment in its current account

Despite a higher-than-expected current account deficit in November, amid a wider primary income deficit, the improvement in the external imbalance on a 12-month rolling basis continued

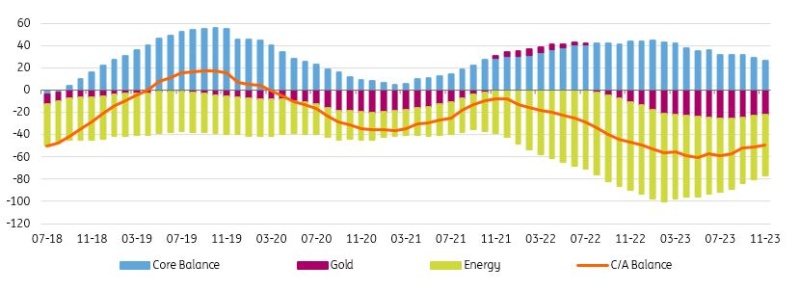

The current account posted a deficit of US$2.7bn in November, significantly higher than the market consensus of US$1.7bn. Accordingly, the normalisation in the 12-month rolling deficit continued, albeit at a slower pace, with a decline to US$49.6bn from US$50.9bn a month ago.

Current account (12M rolling, US$bn)

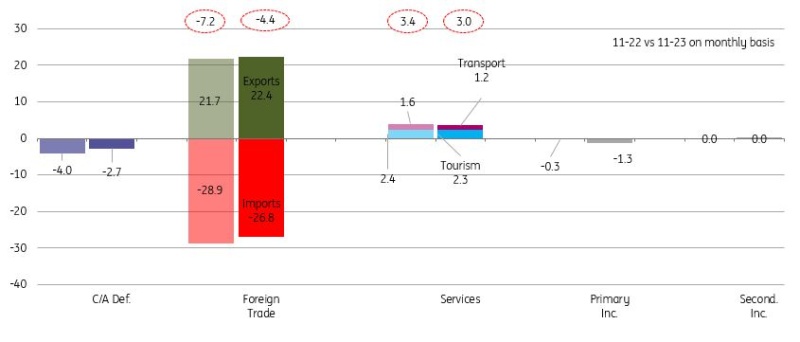

The breakdown of monthly data shows that the improvement in the trade balance, stemming from energy and gold, was the major driver of the decline, despite a narrowing core trade surplus. However, smaller services income, amid easing transport revenues and a higher deficit in primary income due to a sharp fall in investment income - limited the recovery in the external balance. Continuing pressure on the core deficit compared with the same month of the previous year supports the case for a tighter policy stance, while we will likely see the start of a recovery with the expected slowdown in domestic demand.

Breakdown of current account (monthly, US$bn)

On the capital account, net identified flows turned stronger with US$11.4bn of inflows. Errors and omission outflows, which came back in September and continued in October, were at US$1.9bn in November, amounting to US$7.1bn in the last three months. Despite the high monthly c/a deficit and large outflows via net errors & omissions, official reserves recorded a US$6.7bn increase on the back of reviving identified flows. In the first 11 months of 2023, registered capital flows (US$49.6bn) remained below the accumulated deficit (US$43.6bn) and net errors & omission outflows (US$10bn), leading to a reserve depletion of US$4bn.

In the breakdown of monthly data, large inflows were driven by non-residents’ movements. These items were:

- The Treasury’s US$2.5bn sukuk issuance

- US$2.6bn of external issuance from banks and corporates

- US$0.8bn of equity purchases from foreign investors

- US$0.8bn of inward FDI

- US$0.6bn of deposits placed by non-residents to the local banking system

- US$4bn of net borrowing both in the long- and short-term by local banks. Accordingly, the rollover rates for banks and corporates stood at 149% and 92% in November (vs 112% and 99% on a 12M rolling basis), respectively.

Breakdown of financing (monthly, US$bn)

Overall, after the peak in July when domestic demand pushed up imports significantly and the gold trade balance deteriorated, the current account has been on an improving trend, though this is currently slower than expected. The trend will likely continue in the period ahead with an ongoing tightening in financial conditions, and hence a visible deceleration in growth. However, a slower normalisation in domestic demand with fiscal spending related to earthquake reconstruction and higher than envisaged wage adjustments could increase upside risks on the current account. On the other side, a faster decline in gold imports and energy imports could be supportive of the pace of improvement in the external imbalance.

The capital account, on the other hand, has been quite weak, though the outcome in November showed a significant recovery amid higher net borrowing from the banking sector and eurobond issuance by both banks and corporates. Increases in bank deposits, which have been supportive of financial inflows, moderated in November. Given policymakers’ priority to replenish reserves, higher external financing needs require strength in capital inflows to continue.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap