Turkish inflation rises in December

Turkey's annual inflation rose as expected in December, ending 2023 at 65.7%. It's likely to remain elevated in the near term due to wage adjustments – particularly to the minimum wage – as well as slower normalisation in domestic demand and hikes in administrative prices

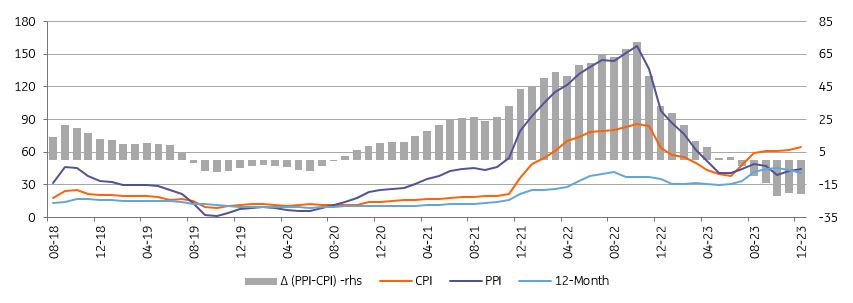

Turkey's monthly inflation came in slightly below of consensus at 2.93% month-on-month, with annual inflation for 2023 at 64.8% year-on-year versus the forecast 65% from the Central Bank of Turkey (CBT) in its latest inflation report. An increase from 62% a month ago came about on the back of higher food and energy prices. While there was an increase of 1.2% in December 2022, the average of December months in the 2003-based index for the last ten years has been 1.9%, indicating that the base effect was unfavourable for this year.

Inflation outlook (%)

On the other hand, October PPI stood at 1.1% MoM, translating into 44.2% YoY. The decline in annual PPI from close to triple digits at the end of last year shows an improvement in cost pressures despite a YoY increase in the TL equivalent of import prices lately due to commodity price developments and exchange rate increases.

Core inflation (CPI-C) came in at 2.31% MoM, inching up to 70.6% on an annual basis on the back of pricing behaviour, exchange rate developments, adjustments in administered prices and inertia in services. On a seasonally adjusted basis, headline inflation remained broadly unchanged in the last month of 2023 despite an increase in goods inflation. Services recorded the lowest monthly reading last year, offsetting the impact from the goods.

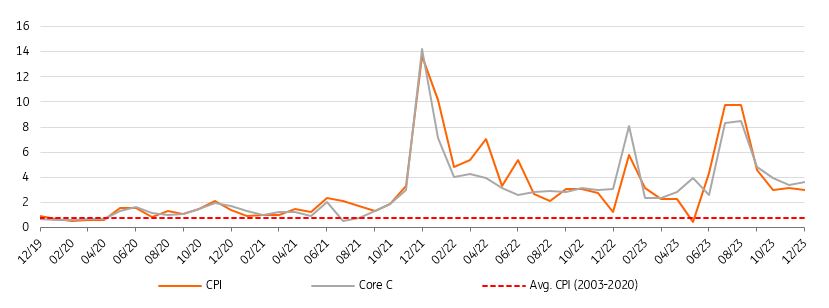

Monthly trend CPI (sa, MoM)

In the breakdown:

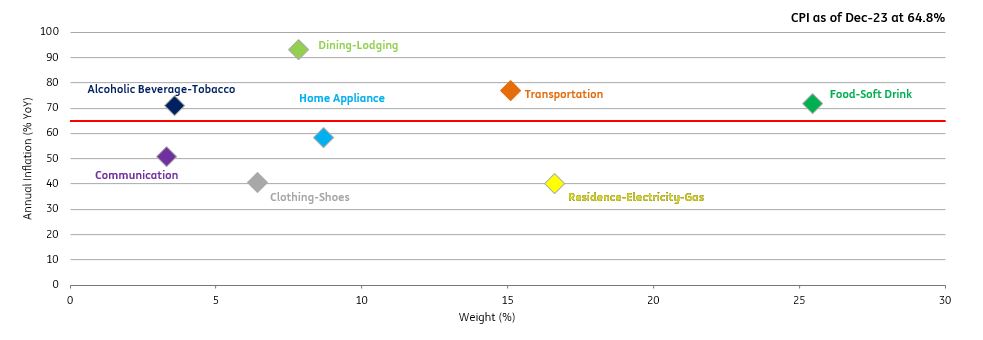

- Food turned out to be the major contributor, with 1.26ppt leading to a jump in the annual figure to 72% driven by unprocessed food (particularly fresh fruits and vegetables).

- Housing followed food with 0.69ppt due to the continuing impact of natural gas as prices – 25 cubic metres of which are provided free of charge – rose in line with the increase in consumption and continued to have an upward impact on energy prices. However, we saw a decline in the impact last month vs that seen in November. Accordingly, energy inflation maintained its recent uptrend and reached 27.2% from 21.2% a month ago. Rent was another area that pulled housing prices higher, though the moderation in monthly changes attracted attention.

- On the flip side, clothing due to seasonality and transportation stemming from a decline in gasoline prices slightly reduced monthly inflation in December.

As a result, goods inflation moved up to 55.5% YoY, while core goods inflation receded to 52.8% YoY. Annual inflation in services was significantly influenced by domestic demand, and wage hikes maintained an uptrend. It reached another peak at 90.7% YoY, attributable to the continuing rise in rent, catering and telecommunication services.

Annual inflation in expenditure groups

Overall, annual inflation rose as expected in December. We expect further increases in the near term, given the higher than-expected minimum wage hike and increases in administrative prices due to SCT and revaluation rate-related adjustments. Accordingly, we see inflation remaining elevated until mid-2024, with further increases above 70% on seasonal effects in January and unfavourable base effects in May. On the other hand, the second half of the year ahead will likely see a sharp downtrend – reflecting this year’s high base and further impact of tighter policy, pulling inflation to below 45% at year-end.

In its monetary policy strategy for 2024, the CBT summarised its planned policy actions:

- Targeting an increase in the share of TRY deposits to 50% in the banking system and sustaining the fall in the FX-protected deposit scheme. Accordingly, FX-protected deposit accounts converted from TRY deposits will not be opened or renewed as of 1 January, while banks will continue to be able to open and renew FX-protected deposits that are converted from FX.

- Maintaining reserve build-up strategy and uptrend in its international foreign currency reserves.

- Implementing further quantitative tightening and taking steps in the simplification process.

- Limiting its securities portfolio to TRY 200bn.

- Continuing to conduct swaps with banks, it plans to gradually reduce the amount of swap transactions.

At its December MPC meeting, the CBT raised the one-week repo rate to 42.5%, providing guidance that the tightening cycle would be completed as soon as possible. The central bank also reiterated that the monetary tightening required for the sustained price stability would be maintained as long as necessary. Accordingly, following one more hike in January, we expect the CBT to remain mute until the third quarter of next year.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap