Turkish GDP growth sees further deceleration in third quarter

Turkey’s economic activity has lost further momentum in the third quarter thanks to tight financial conditions, while its growth composition improved further on the back of a higher contribution from net exports

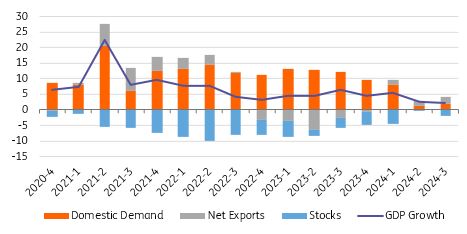

GDP growth in the third quarter came in at 2.1% on a year-on-year basis, below the market consensus (2.6%) and our call (2.4%), and driven by gross fixed capital formation. TurkStat, on the other hand, revised second-quarter GDP expansion down to 2.4% from 2.5%. Accordingly, nine-month GDP growth stood at 3.2%.

On a seasonally adjusted basis, following TurkStat’s downward revision for the second quarter, the sequential growth in this period turned to negative -0.2% quarter-on-quarter. Third-quarter GDP, on the other hand, recorded a negative QoQ growth rate of -0.2%. This shows further weakness as Turkey is now in a technical recession. Its feeble sequential performance is attributable to government consumption turning negative as well as further weakness in private spending and a negative contribution from inventories.

Quarterly Growth (%, YoY)

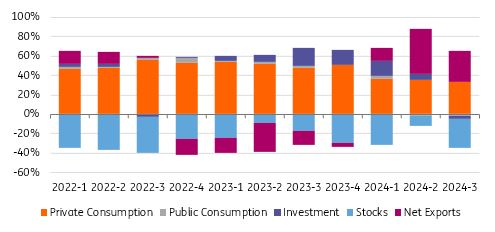

When we look at the breakdown on expenditures in the third quarter and compare them with the same period of 2023:

- Private consumption has remained sluggish with a 3.1% YoY rise (lifting the headline GDP by 2.2ppt), given that the expansion was 7.0% YoY in the first quarter and 1.5% YoY in the second quarter.

- Investment appetite weakened from 9% YoY in the first quarter to 0.8% YoY in the second quarter, turning negative with -0.8% YoY growth. This translates into a -0.1ppt contribution to the GDP expansion and was mainly driven by a continuing contraction in machinery equipment (8.6% YoY) after diving into negative territory in the second quarter. However, construction investments have remained robust with strong 9.4% YoY growth following 8.4% YoY a quarter ago.

- Public consumption, which has positively contributed to the headline GDP in recent years, has been losing steam in the last two quarters and fell by a -0.9% YoY, dragging third-quarter growth down by -0.1ppt. This reflects that expenditure and revenue-side measures taken after local election in fiscal policy have created impact

- Inventory build-up shaved 2.0ppt off growth.

- Finally, net exports continued to support the headline growth with a 2.2ppt contribution. This is mainly attributable to a contraction in imports.

In the sector breakdown, construction turned out to be the biggest contributor (0.5ppt), followed by agriculture (0.4ppt). Further deceleration in the services sector and declining contribution to the headline GDP in recent quarters also attracted attention.

Drivers of the growth (ppt contribution)

We expect Turkey's economic activity to remain soft in the last quarter, given tighter financial conditions leading to ongoing normalisation in domestic demand – although some recent indicators, such as capacity utilisation, real sector confidence, retail and construction sector indices, showed a recovery in November. The Central Bank of Turkey's recent communication suggested that we are nearing a gradual rate-cutting cycle, implying a December move as a real possibility. We see a tight monetary stance prevailing in the period ahead and forecast GDP growth this year at 2.8%.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap