Turkey’s current account deficit widens in July

Despite Turkey's large current account deficit, official reserves increased in July on the back of strong net errors and omissions inflows and a surplus in the financing account

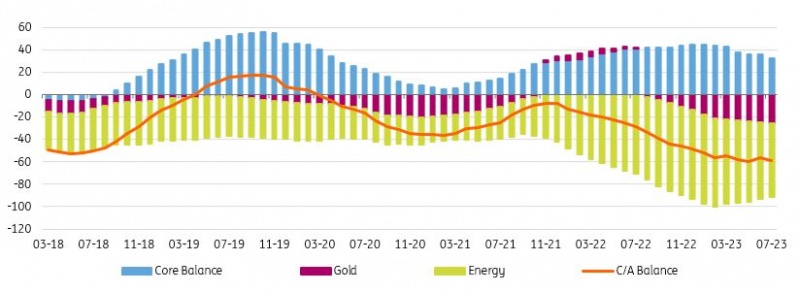

After some relief in June with a surplus of $0.7 billion, Turkey's current account dove into deficit again in July with $-5.5 billion – much higher than both the consensus and our call of $4.5 billion. The 12M rolling deficit widened to $-58.5 billion, which translates to around 5.8% of GDP.

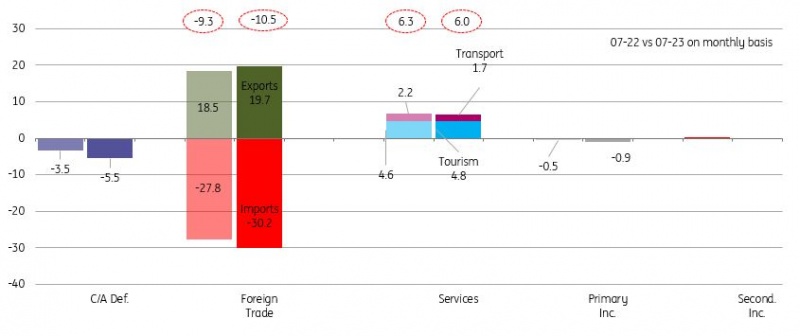

Breakdown of current account (monthly, US$bn)

A quick glance at the data points towards core trade and gold balance being the major drivers in the deterioration of gold deficit, despite lower energy bills due to a recent drop in oil prices. Services income, on the other hand, showed a slight decline on the back of moderating transport revenues, while (net) tourism revenues maintained strength and reached another peak on an annual basis of $39.6 billion.

Current account (12M rolling, US$bn)

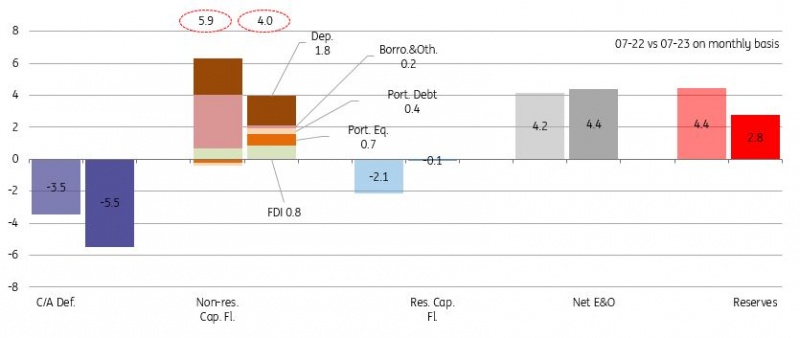

The capital account saw net identified inflows at $3.8 billion. Net errors and omissions stood at $4.4 billion and reached $12.6 billion in the two months following elections, reversing outflows from two months prior to the elections. With the monthly current account deficit and large inflows via net errors and omissions, official reserves recorded a $2.8 billion increase. However, given the weakness in the flows, reserves financed more than half of the current account deficit in the first seven months of this year.

In the breakdown, resident flows were quite negligible. For non-residents, $4.0 billion inflows were attributable to i) $0.7 billion gross FDI, ii) foreign investors’ $0.7 billion equity purchases, iii) $1.8 billion deposits placed by non-residents to the local banking system, iv) US$0.9bn increase in trade credits, and v) US$0.4bn eurobond issuance by banks. Regarding rollover rates, we saw a moderation in both banks and corporates to 58% and 73% in July (vs 85% and 108% respectively on a 12M rolling basis).

Breakdown of financing (monthly, US$bn)

From January to July this year, domestic demand pushed imports upwards and the deterioration of the gold trade balance weighed on the current account – despite a narrowing energy deficit and the supportive impact of a decline in both energy and commodity prices, alongside continued strength in tourism revenues. Since the elections, there has also been a gradual tightening in financial conditions.

This backdrop – with a visible deceleration in growth – should lead to an improvement in the current account moving forward. However, the outlook still remains challenging as the decline in global leading activity indicators increase the risk of a slowdown in exports. For the capital account, total flows have improved since the elections, with strong net errors and omissions. An ongoing pivot to a more conventional policy stance will likely be crucial for recovery in investor confidence and identified flows.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap