Turkey: Accelerating growth momentum in the second quarter

Second-quarter GDP reflected strong consumption demand and continuing support from external demand. However, we see momentum loss in activity in the second half of this year on the back of deteriorating purchasing power and a less supportive global backdrop

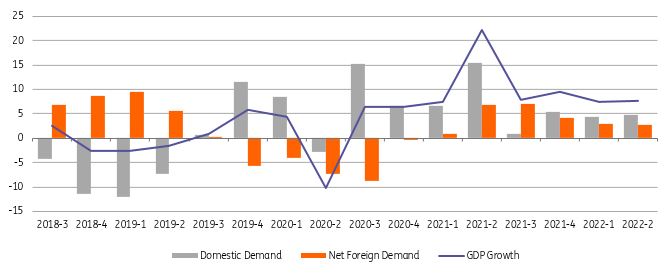

Second-quarter GDP in Turkey was 7.6% on a year-on-year basis, close to the market consensus (7.5%) and higher than our call (6.5%). The breakdown of year-on-year growth reveals continuing support from private consumption and net exports despite a marked drop in consumer confidence and a less supportive global backdrop with geopolitical challenges and the increasing tightening stance of global central banks, while investment activity has remained relatively subdued. The Turkish Statistical Institute also revised 2021 growth from 11% to 11.4% and first-quarter GDP expansion to 7.5% from 7.3%.

Quarterly growth (%, YoY)

The second-quarter GDP figure translates into a quarter-on-quarter growth rate of 2.1% after seasonal adjustments, showing significant acceleration over the first quarter at 0.7% which was the lowest quarterly reading since the first half of 2020. Like the first quarter, sequential performance is mainly attributable to private consumption and net exports, while capital formation and stock depletion were drags.

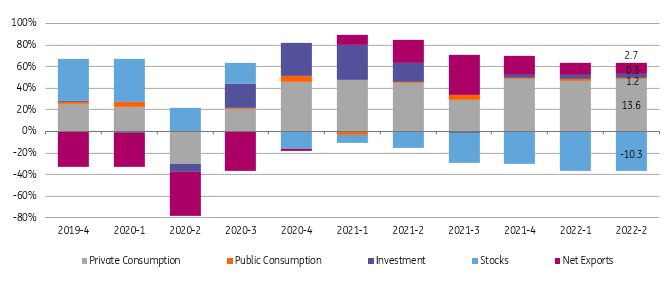

On the demand side, private consumption has maintained its strong pace with 22.5% YoY growth and turned out to be the major driver with a 13.6ppt contribution to the headline GDP expansion in the second quarter of 2022. The breakdown reveals a balanced outlook with strong support from both goods and services. This shows a continuation of robust household consumption driven by negative real rates, leading to fewer savings and supporting the consumption appetite.

Investment appetite on the other has remained relatively subdued in comparison to the strong performance realised last year, likely attributable to policy steps introduced to put a break on commercial TRY loan growth. Accordingly, 2Q investment growth stood at 4.7% YoY, translating into +1.2ppt contribution to the headline. In the breakdown, strength in machinery and equipment investments – which was up by 17.8% with a sequence of positive readings since the last quarter of 2019 – attracts attention, while construction investments have remained in the negative territory.

A closer look at the data shows that public consumption added 0.2ppt to the headline, inventory build-up shaved more than 10.0ppt off growth, while net exports raised the headline growth by +2.7ppt, the biggest contribution after household consumption. This is attributable to continuing strength in exports up by 3.9% YoY, despite 1.1% YoY growth in imports.

In the sectoral breakdown, all sectors with the exception of construction and agriculture lifted the headline growth signalling a continuation of a broad-based strength in economic activity. Among positive drivers, services, once again, was the biggest contributor, pulling the second-quarter performance up by 4.2ppt, followed by industry at 1.7ppt as indicated by industrial production data and the financial sector at 1.3ppt.

Drivers of growth (ppt contribution)

Overall, 2Q GDP reflected strong consumption demand and continuing support from external demand which were also the major drivers in recent quarters. However, we see momentum loss in activity in the second half of this year on the back of deteriorating purchasing power, concerns about policy sustainability, as well as a less supportive global backdrop with tightening global central bank policies and elevated geopolitical risks. Accordingly, we look for around 4.0% YoY growth this year, from 11.4% last year.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap