Three scenarios for the Bank of England as rates left on hold

While we get the sense the Bank of England would still prefer to tighten policy sooner than later, heightened uncertainty and a higher probability of a Brexit delay mean the next rate hike could still be some way off

While the Bank of England unanimously opted to keep rates unchanged at its December meeting today, an increased air of caution is evident throughout the latest statement. Most notably, the Bank noted that Brexit uncertainty has 'intensified considerably,' and as a result of this and softer global growth, now expects momentum to slow further during both this and the next quarter.

We agree. Despite some better numbers on Thursday, the retail sector is facing a tough Christmas period as consumers grow more cautious. This negative sentiment could grow if individuals become more nervous about job security as the perceived risk of 'no deal' rises, while at the very least, firms are likely to hold off on near-term hiring/investment decisions.

That all said, the core message from the Bank of England seems to be unchanged. Policymakers still see inflationary pressures building as wage growth rises, and we get the sense policymakers still have a mild preference to tighten policy again sooner than later if they can.

This implies that current market expectations (no rate hike until May 2020) could prove too pessimistic, although of course what happens next still relies almost solely on Brexit. The three main scenarios for the Bank's next steps are:

Against the odds, Brexit deal approved in time for March

Admittedly this is getting increasingly unlikely by the day, but if Parliament ultimately rejects all other viable options (e.g. a second referendum or Norway-style model), or if the risks of ‘no deal’ focus minds of lawmakers, then there is still a very small chance that MPs may ultimately decide to back a version of Theresa May’s deal.

If this were to happen – or if an alternative solution were found that enabled the UK to avoid ‘no deal’ and leave the EU as scheduled in March 2019 – then we don’t think the Bank of England would hang around for long before hiking rates.

A hike could happen as soon as May, depending on how heavily the economy stalls during the first quarter.

Brexit delayed – BoE hike pushed back

If Parliament rejects Theresa May's deal in January, which seems highly likely, then there will inevitably be a push amongst MPs for either a softer Norway-style deal, a second referendum, or even a snap election, to break the deadlock.

In all three cases, some form of Brexit delay – most likely via an article 50 extension – would become much more likely. Remember that UK Parliamentary rules mean the EU Withdrawal Act needs to be laid down 21 sitting days before coming into force, which in other words means that any deal needs to be approved by MPs by 26 February.

A Brexit delay would result in a much more prolonged period of uncertainty for businesses and consumers. For the Bank of England, this could easily push the timing of the next rate hike much further back into 2019.

No deal – hike or cut?

Even though it seems there is no majority in Parliament for ‘no deal’, this remains the default option given that March 29 is written into UK law as the current exit date.

In this scenario, the Bank of England has implied interest rates could go in either direction. On balance though, we suspect 'no deal' would cause a substantial hit to confidence (in addition to significant disruption to supply chains), which makes it much less likely the Bank would decide to hike interest rates in this scenario. That said, our feeling is that policymakers may be inclined to wait a little longer to get a better steer on the true economic impact before deciding whether or not to ease policy.

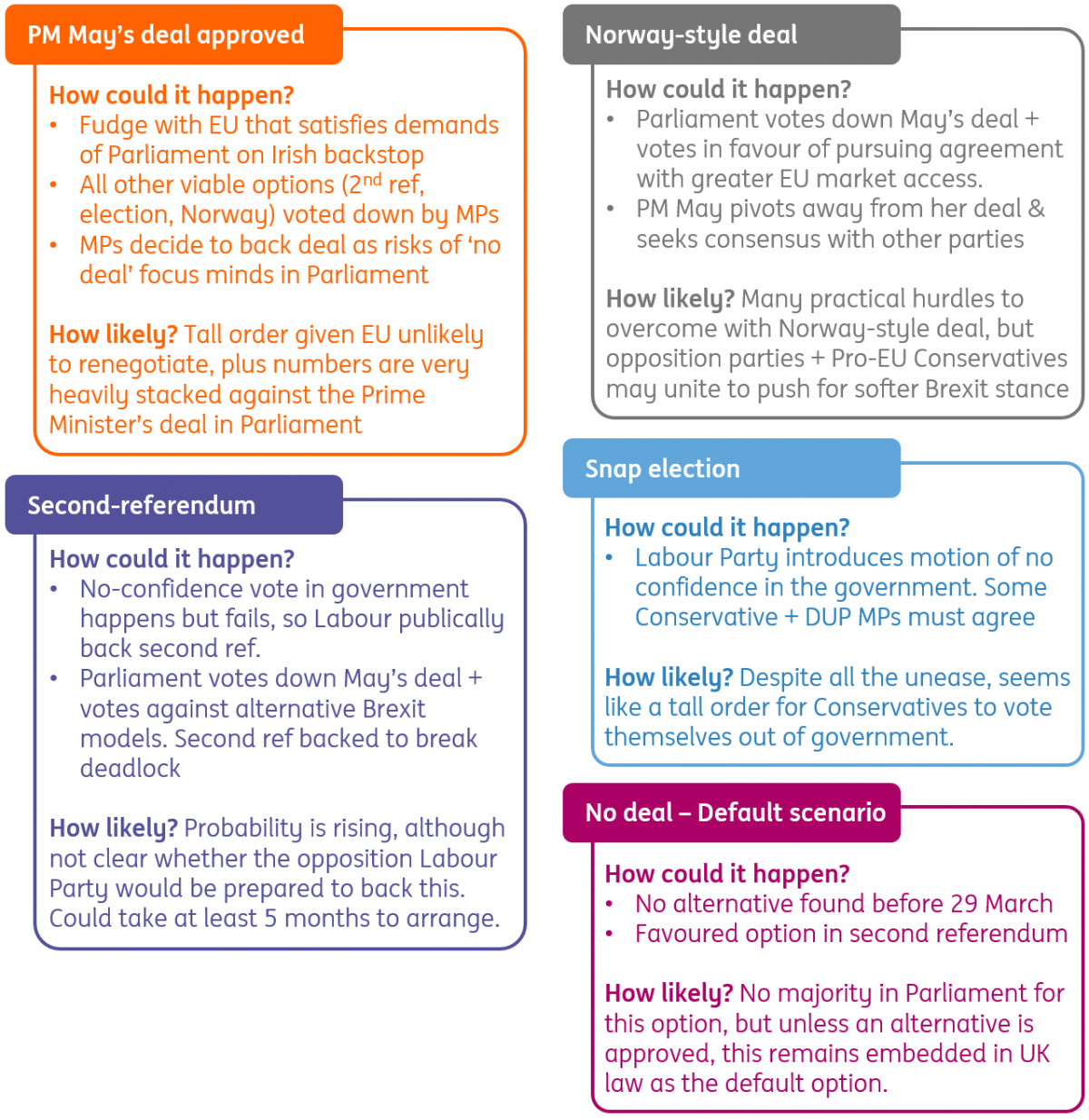

What next for Brexit? Five possible scenarios

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap