The Reserve Bank of India delivers a hawkish hold

Was today’s no change to policy and hawkish statement a demonstration of the RBI’s independence as some are suggesting? Or is the backdrop simply not yet conducive to a cut? We believe it’s mostly the latter

| 4-2 |

Votes for no change vs easingOne more vote to ease than previously |

Surprisingly interesting meeting

On paper, this should have been a routine meeting with nothing much to report. India's headline inflation remains stuck in the top half of the Reserve Bank of India's (RBI) inflation target range (2-6%) at 4.8% year-on-year, and first quarter GDP growth for 2024 was another stratospheric 7.7% YoY. Federal Reserve rate cuts still seem a way off and until this week, Asian FX was on the back foot, and the INR was only holding its ground due to heavy RBI management.

But the loss of Prime Minister Narendra Modi's outright majority and the need to lean more heavily on coalition allies to run the country has increased talk of greater government spending, some slippage on reforms, and potentially even some chiselling away at the RBI's independence.

And that may be the light in which to read today's RBI statement, which pushed back at calls for imminent easing and doesn't suggest the RBI will be minded to ease until later on in the year.

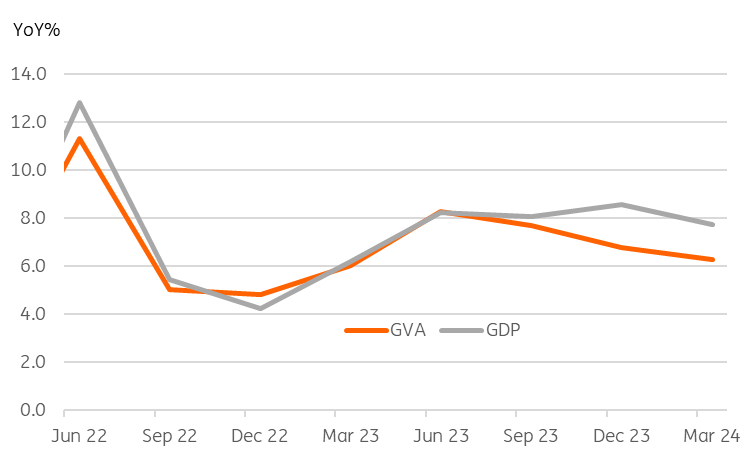

GDP versus GVA (YoY%)

Why is easing even being talked about?

With growth hovering in the high-7% range, and inflation only just below 5%, it may seem strange that anyone - including two MPC members - is arguing for a rate cut. It may seem just as strange that cuts are being advocated on the basis that the RBI's rate policy is currently damaging growth.

Those who make such arguments note that the gross value added (GVA) measures of economic output, a production-based equivalent of GDP, has been running much softer than GDP growth. Compared to the 7.7% GDP rate recorded for the first quarter of this year, the GVA measure recorded only 6.3% in the same period and has been consistently softer than GDP, which even some previous RBI governors have hinted was a slightly flaky statistic.

With some commentators pointing to high unemployment (despite the apparent strong growth) as a reason for disaffection at the polls, a boost to growth from lower rates might be seen as one way to repair some of that damage.

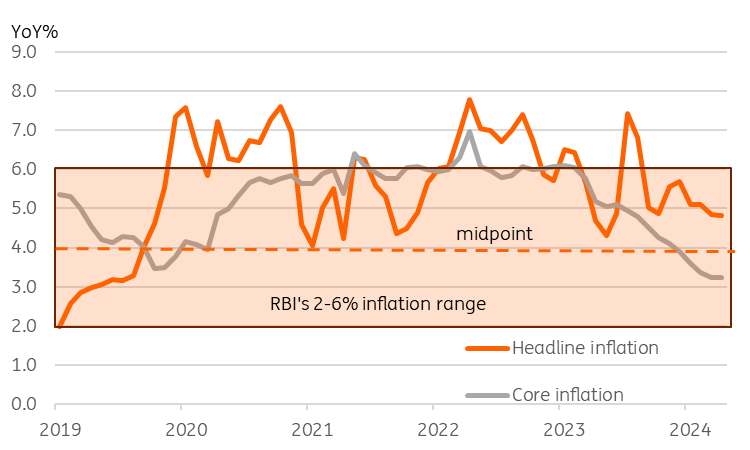

Headline versus core inflation

Core inflation is looking fairly benign

On the inflation front, headline inflation has been in the top half of the RBI's range for quite some time – although much of that is owed to elevated food prices, and core inflation looks much less concerning.

But as the RBI statement notes, some of these non-core influences are expected to persist, and only briefly for one quarter (the third quarter of this year) does it expect inflation to dip below the mid-point of their inflation target range.

The RBI also quite sensibly seems to view the risks of persistent shocks to food as asymmetric and biased upwards given climate change and the growing likelihood of meteorological shocks.

So, despite running one of the highest policy rates in the region, both in absolute terms and relative to inflation ("realised" real inflation is a rough yardstick for policy tightness), it looks as if the RBI wants to see a bit more evidence of inflation coming down and running closer to its target midpoint before it would consider easing rates.

We are not forecasting the RBI to cut until the fourth quarter of this year. But we could move this up to the third quarter if the Federal Reserve begins to ease before then, as this would also take some pressure off the INR.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap