Swiss National Bank raises rates by 50bp

The SNB has just joined the hawkish camp by raising its rate by 50 basis points to -0.25%. This indicates a willingness to take the lead and keep the initiative given the expected rate hikes by the ECB. Over the year, the SNB should nevertheless be less aggressive than the ECB.

Surprise rate hike

While the consensus was that the SNB would keep its key rate unchanged in June, the central bank surprised everyone by raising its rate by 50 basis points. The key interest rate has thus been raised from -0.75% to -0.25%. According to the press release, this rate hike is aimed at countering inflationary pressures, as inflation in Switzerland reached 2.9% in May, its highest level since the summer of 2008, which is higher than the SNB's objective of having inflation between 0 and 2%. After years of fighting deflation, inflation is now too high and the SNB has decided to act quickly.

This rapid change in monetary policy is also explained by the situation in the foreign exchange market. While the Swiss franc was considered by the SNB to be overvalued for years, which pushed inflation down, the SNB now believes the franc is no longer highly valued. By deciding to raise rates before the European Central Bank, the SNB is indicating that an appreciating Swiss franc is no longer a problem for them. On the contrary, it is acceptable because the appreciation of the Swiss franc allows inflation in Switzerland to remain more moderate than in neighbouring countries and avoids a real depreciation, given the inflation differential between Switzerland and neighbouring countries. Remarkably, SNB Governing Board Chairman Thomas Jordan indicated that the SNB was prepared to intervene in the foreign exchange market if the situation required it, both by buying currencies as the SNB has done for years, but also by selling in the event of too great a weakening of the Swiss franc.

The September meeting will be more open

In our view, today's decision indicates a willingness by the SNB to take the lead. While the ECB announced last week that it would raise rates by 25 basis points in July and by 25 or 50 basis points in September, the SNB did not want to wait until its meeting on 22 September to raise rates itself and have to catch up with the ECB's 75 basis point rate hike. Raising rates now, therefore, means that it does not have to rush into major rate hikes later on and retains the initiative. This gives the SNB room to manoeuvre in deciding what to do in September, depending on data developments and the global economic and geopolitical situation. Following today's rate hike, the September meeting is therefore more open.

The SNB has revised its inflation forecast upwards, which is now based on the assumption of a policy rate of -0.25%. It now expects an average of 2.8% for 2022, 1.9% in 2023, 1.6% in 2024, and 2.1% in the first quarter of 2024. It therefore believes that inflationary pressures will remain, but will fall below the 2% mark in 2023 and 2024. The SNB also states that it "cannot be ruled out that further increases in the SNB policy rate will be necessary in the foreseeable future". Given the inflation forecasts and the economic environment, we believe that a further 25bp rate hike is to be expected this year, but we think it unlikely that the SNB will go further than that this year. In our view, once the policy rate moves to 0%, any further rate hikes would be for 2023. The SNB should therefore be less aggressive in its rate hikes than the ECB.

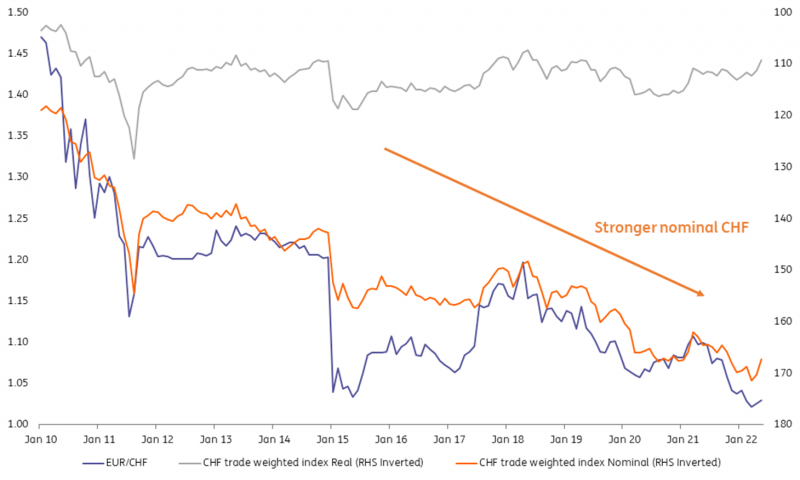

FX: The SNB could now be buying Swiss francs, not selling them

Today’s SNB statement marks a sea-change for the Swiss franc. For over a decade, the SNB had been battling deflation and battling Swiss franc strength. Various descriptions of CHF over-valuation had been used over the years and the SNB had accumulated over CHF800bn in FX reserves in fighting that strength.

Yet today the SNB’s statement has changed markedly. Gone is the reference to the highly valued Swiss franc and the need for FX intervention to redress it. Instead, the SNB has inserted a telling phrase: ‘To ensure appropriate monetary conditions, the SNB is also willing to be active on the FX market as necessary’. We take this to mean that the SNB will now sell EUR/CHF to ensure that the trade-weighted CHF appreciates by roughly 4% per annum. Why do we say 4%? This because the SNB told us in late April it wants to keep the real CHF stable and 4% nominal appreciation in the trade-weighted CHF is required to offset the low inflation in Switzerland relative to trading partners.

Expect now the SNB to use its substantial FX reserves to guide EUR/CHF lower over the next 12 months. We have a 12m target at 1.00. That target could be lower if the dollar were to be stronger than we forecast, driving USD/CHF higher and the trade-weighted CHF lower than our current projections. In that case, the SNB would need a lower EUR/CHF to offset the higher USD/CHF. The SNB selling FX reserves will now have some interesting implications for asset markets, where the SNB has been the front-runner in diversifying FX reserves into corporate debt and equities. These flows stand to go into reverse.

We expect now the SNB to use its substantial FX reserves to guide EUR/CHF lower over the next 12 months

Euro government bonds on notice for SNB intervention

The spectre of the SNB selling out of some of its FX reserves, and so of its foreign bond holdings, has not escaped the attention of the rates market. It held 37% of its reserves in EUR as of Q1 2022 and another 39% was invested in USD. On account of the greater fragmentation and lower liquidity of the EUR bond market, we would expect euro government bonds (EGB) to see the greatest impact, but the effect should be felt in core markets globally. This would add to the angst caused by a series of surprise rate hikes, including the 50bp move by the SNB today.

The average maturity of the SNB’s bond holdings suggests the 5Y sector of foreign bond curves will be the hardest hit. We also infer that roughly a third of the EUR bonds it holds are investments in semi-core markets (e.g. France, Belgium) making this sector one of the most vulnerable in the event of FX intervention. In summary, the surprise SNB hike and potential for FX intervention add to the upside to developed market yields globally. We also see a risk of it exacerbating the sovereign spread widening if it decides to sell out of its semi-core or bond holdings.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap