Sticky UK services inflation not enough to unlock a November rate hike

UK inflation has come in a little higher than expected, but given the surprise isn't huge and some of it can be put down to volatile package holidays, we don't think there's enough here to tempt the Bank of England into resuming its rate hike cycle in early November

UK core inflation has come in fractionally higher than expected for September, but in reality, there’s not much here that’s likely to pressure the Bank of England into resuming its rate hike cycle in November. Remember what the Bank is chiefly interested in is services inflation, and this nudged up from 6.8% to 6.9%, though the volatile package holidays category seems to have done a lot of the leg work there. Importantly, this is also still a little below what the Bank had forecast in its most recent projections from early August (7%), and it’s also still a few tenths of a percentage point off the peak.

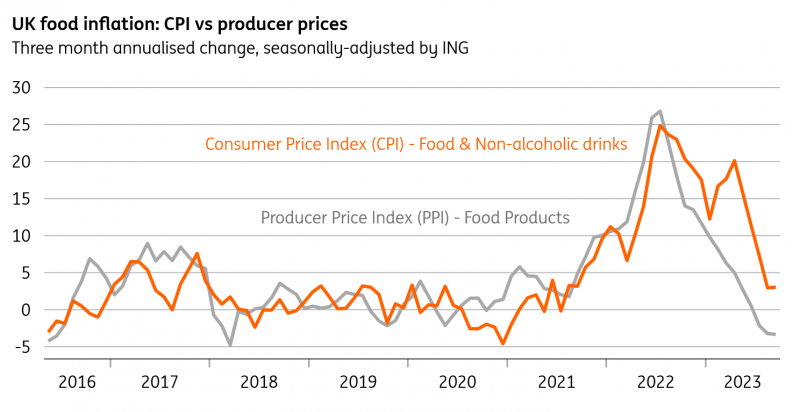

Elsewhere, the news was arguably a bit brighter. Headline inflation may have stayed at 6.7%, thanks mainly to another near-4% increase in petrol/diesel prices last month. But food prices fell across September, which is the first such month-on-month decline in two years. This is a trend that we expect to continue, given that producer price inflation (on a three-month annualised basis) has been pointing to deflation for a couple of months now.

Producer prices point to further food disinflation for consumers

Where next? We still think services inflation should start to come lower through the remainder of the year, perhaps ending 2023 at 6%. That’s not a huge improvement admittedly, but would echo survey evidence which suggests fewer firms are raising prices and those that are have been lifting them less aggressively. A survey from the Office for National Statistics told us last winter that the primary basis for raising prices was higher energy costs, and we expect the same to be true in reverse now gas prices have been much lower for quite some time.

For headline inflation, of course, October will see another step lower as last year’s steep increase in household energy bills drops out of the annual comparison. With food inflation slowing too, we headline CPI to dip to 5% or below in October and stay broadly unchanged until the end of the year, though this partly depends on what happens to oil prices.

With neither yesterday’s wage data nor today’s services inflation data containing any earth-shattering surprises, we think the Bank will be content with keeping rates on hold again in November.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Tags

Bank of EnglandDownload

Download snap