South Korea GDP contracts more than expected, increasing odds of recession and rate cuts

Domestic political turmoil pushed South Korea’s economy into contraction. US tariffs and delays in policy support increase the odds of a technical recession in the current quarter, leading to a Bank of Korea rate cut in May and larger fiscal support

| -0.2% |

1Q GDP (QoQ)-0.1% (YoY) |

| Lower than expected | |

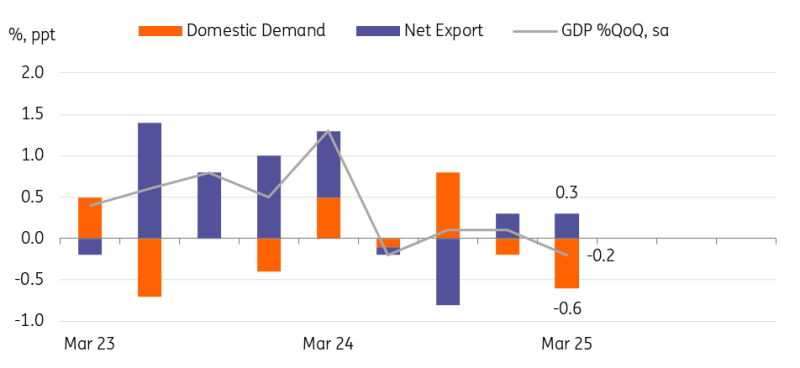

Domestic demand contracted more than expected

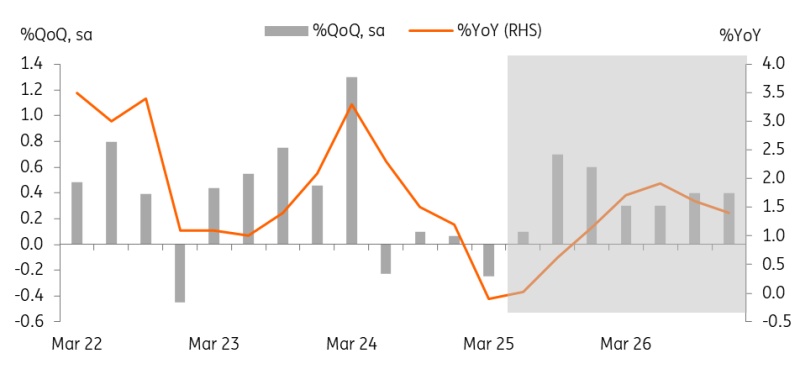

South Korean GDP contracted more than expected in the first three months of the year. Althought the Bank of Korea flagged the possibility last week, the 0.2% quarter-on-quarter drop was a shock to the market in light of the BoK holding its key interest rate unchanged at its April meeting. Markets had expected GDP to grow a mere 0.1% (ING expected 0.2%). In the year-on-year comparison, the GDP dropped 0.1% (vs 1.2% in the fourth quarter of 2024).

Domestic demand remained weak in 1Q25

Details were grim, with all expenditures contracting

On the expenditure side, both private and government consumption contracted by 0.1%, mainly due to increased uncertainty about the domestic political environment and natural disasters. The main drag was investment spending. Construction investment dropped the most -- by 3.2% -- and equipment investment fell 2.1%. Ongoing restructuring efforts in the construction sector and the slowdown in semiconductor investment were behind the drop. Thus, domestic demand dragged broader growth down by 0.6 ppt. On the other hand, imports (-2.0%) dropped faster than exports (-1.2%), making net exports a positive, adding 0.3ppt to the growth.

Recession risks increase, but it's still not base-case scenario

We still believe the Korean economy is likely to avoid a technical recession. However, the possibility is clearly growing.

In the second quarter, domestic growth is expected to rebound, but only marginally. Political uncertainty has eased since the beginning of April. Also, spending tends to increase during important election periods. The rise in capital goods imports in recent months points to a recovery in equipment investment. Lastly, reconstruction following the wildfires in the south of the country is expected to boost spending temporarily this quarter.

However, consumer sentiment rose only marginally in April, raising concerns about the fragility of the recovery. On the external demand front, the threat of tariffs seems to have peaked following the recent softening of President Trump's tariff policy towards China. Yet we believe tariffs already imposed are likely to weigh on exports this quarter. Even if some tariffs are eased or lifted, this won’t prompt a sudden increase in exports.

With regard to the tariff negotiations, we're cautious about reaching an agreement in the short term. This is highly uncertain as the US position on certain sectors has changed rapidly on several occasions. In addition, as the Japan-US talks showed, negotiations are linked to defence policy, on area in which it's taking longer than expected to find a middle ground. Moreover, with a new administration likely to take office in early June, it is questionable how much bargaining power the current government will be able to exert.

Policy support is crucial for the recovery in 2H25

Given the weakness of growth in the first quarter and the possibility of a similarly weak second quarter, macroeconomic policy will play an important role in supporting growth. The BoK kept its policy rate on hold at its April meeting due to concerns over the Korean won. However, we expect the BoK to cut rates in May and by a total of 75 basis points by the end of the year.

In terms of fiscal policy, we expect the current government proposal of 12 trillion won to increase slightly once passed before the presidential election. We see a greater chance of another supplementary budget after the election, with the size being much larger than the first one. However, the time lag and the focus on lower multiplier spending items will limit the positive fiscal impact to this year.

Lower GDP outlook for 2025 and 2026

The contraction in the first quarter will reduce annual GDP growth significantly. Even if we don’t expect a contraction in the second quarter for now and recovery in the second half of 2025, Korean GDP is expected to grow a 0.4% YoY (vs 0.8% ) in 2025 and 1.6% (vs 1.7%) in 2026. Growing risks from US recession and delayed policy support at home are the main reasons for the downward revision. Depending on tariff negotiations and the domestic political situation, there are risks to consider on both sides.

We have lowered our GDP forecasts

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap