Solid US spending points to cautious cuts

Consumers may be feeling less confident on the economic outlook amidst job worries, but for now are happy to continue spending. Financial pressures are building for many households, but strength in consumption from those at the top of the income spectrum is more than offsetting that story. This suggests the Fed will tread carefully with 25bp cuts

US retail sales weather the storm

US retail sales rose 0.4% month-on-month in September versus the 0.3% MoM consensus while the "control group" jumped 0.7% MoM versus the 0.3% market expectation. The latter measure excludes some volatile items such as autos, gasoline, food service and building materials and has a history of better tracking broader consumer spending trends. This is a nominal dollar increase, so we need to adjust for inflation (0.2% MoM) to generate "real" spending growth, which feeds through into GDP. That looks pretty robust at around 0.5% MoM and paints a stronger picture than that sugested by softening consumer confidence surveys.

Of course, the recent hurricanes can distort patterns – people buying lots of things ahead of a storm (batteries, flash lights, food etc) on the fear of not being able to buy items before the clean-up operation gets underway. Indeed, the biggest area of strength was from "miscellaneous" stores, which surged 4% MoM. Outside of this component there was also strength in clothing (+1.5% MoM), health & personal care (+1.1%) and food services (+1%). Weakness was concentrated in electronics (-3.3%) and furniture (-1.4%) with lower fuel prices leading to weaker gasoline station sales (-1.6%). Overall though, it points to ongoing resilience in the household sector.

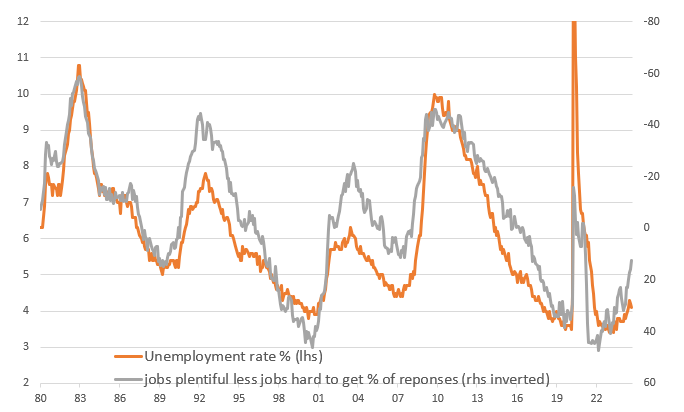

Deteriorating perceptions on the jobs market tend to lead moves in the unemployment rate

How long can high-income households offset weakness in spending from low-income households?

In that regard we know the top 20% of households by income spend more than the entirety of the lowest 60% of households by income. The top 20% are in fantastic shape – inflation has been less of a constraint, property and equity market wealth has soared and high interest rates benefit them – receiving 5%+ on money markets versus perhaps paying 3.5% on a mortgage, if they have one. This group is likely to continue to spend strongly.

However, it is a very different story for the lowest 60% by income with many more renters feeling the pain of sharp increases in housing costs in recent years while wealth gains have been far more modest, and soaring car loan and credit card borrowing costs have been painful. Loan delinquencies are on the rise and the proportion of credit card holders only making the minimum monthly payments has been soaring.

The question for consumer spending is how long those higher-income households can offset a moderation in spending growth from lower-income households. If the jobs market cools as rapidly as some of the hiring data suggests it might and unemployment fears rise further, it may not be all that long. Note the chart above that suggests there is a clear swing in the perception on job security and this tends to show up ahead of actual increases in the unemployment rate.

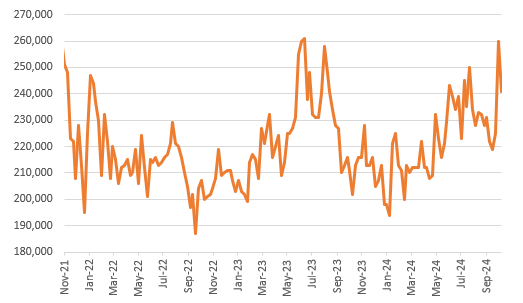

Initial jobless claims are trending higher

Labour market is cooling

Separately, initial jobless claims were 241k last week versus the 259k consensus and down from an upwardly revised 260k the previous week. Continuing claims were a little higher than expected though, rising to 1867k from 1858k and versus the consensus 1865k. As with the retail sales numbers, hurricanes are impacting the data here too, but the general trend is seemingly upward as the chart above shows. Hurricanes had a negative impact on industrial activity, which dissappointed in September. Output dropped 0.3% MoM versus the -0.2% expectation while August's growth was revised down to 0.3% versus the 0.8% rate initially reported. Manufacturing was particularly subdued, declining 0.4%MoM, which is likely due to a combination of Boeing strike action having knock-on effects amongst suppliers and hurricane disruption impacting output. We should get a rebound of sorts next month.

In general, the better-than-expected tone to the data is giving an excuse for Treasury yields to push a little higher. The next big release is probably going to be next week's Fed Beige Book – the central bank's own anecdotal survey of the state of the economy that last time around suggested just 3 of 12 regional Fed banks were experiencing an economic expansion – that was likely a major catalyst for the Fed to opt for a 50bp rate cut in September.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap