Softer-than-expected Turkish inflation in April despite recent lira weakness

Following the accelerated pace of depreciation and worsening inflation expectations since the middle of March, there was an unexpected decrease in Turkey's April inflation figure

Turkey's inflation reading was 3.0% month-on-month in April, coming in below the consensus of 3.1% (and our call at 3.2%) thanks to relatively benign unprocessed food prices. As a result, the annual inflation rate, which has been declining over the past year, fell slightly to 37.9% from 38.1% in March. However, it remains above the Central Bank of Turkey's (CBT) forecast of 24% (with a forecast range of 19-29%). While inflation rose by 3.2% in April 2024, the five-year average for April in the 2003-based index was 3.1%, indicating no meaningful base effect this year.

PPI was 2.8% MoM driven mainly by food products, textiles and metals, while there was a drop in the annual change to 22.5% YoY vs a month ago. The 6.5% MoM and 3.9% MoM increases in the currency basket (50:50 EUR:USD) in March and April, respectively, showed an acceleration compared to previous months and signalled that the pass-through from exchange rates to prices has been more pronounced lately. However, the year-on-year lira increase remained relatively muted at less than 23%, implying that cost pressures have been contained. This has contributed to a more favourable trend in Turkish lira (TL)-denominated import prices along with benign commodity prices, given the large drop in April.

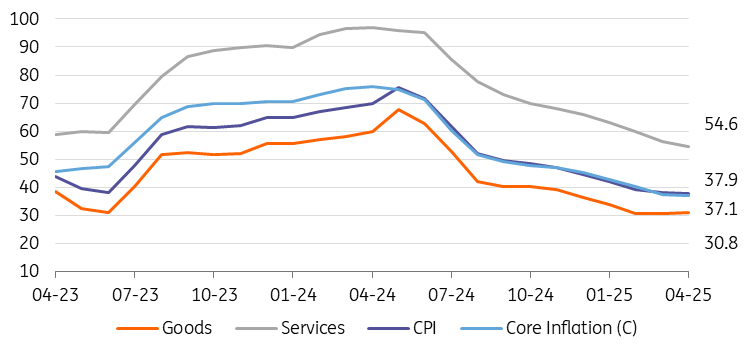

Core inflation (CPI-C) rose by 3.3% MoM, bringing the annual rate down to 37.1%. A preliminary assessment of seasonally adjusted data – set to be published by TurkStat and closely monitored by the CBT to gauge underlying trends – reveals that the acceleration in March headline and core numbers also continued in April, while the pace of increase in core was more evident.

Inflation outlook (%)

Breaking down the data, we can see that:

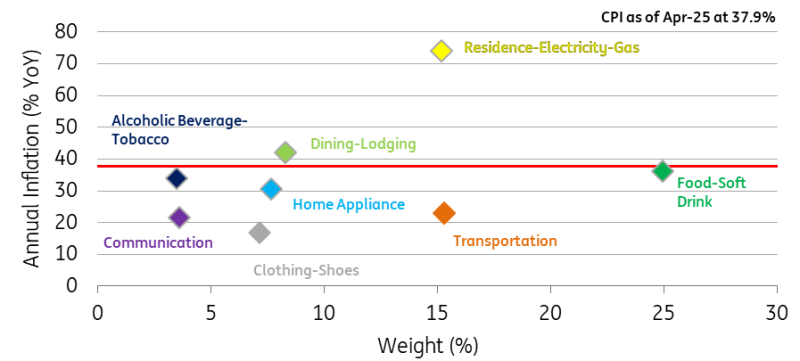

- Housing was the biggest contributor at 0.74 percentage points (ppt), driven by a 25% hike in household electricity prices.

- This was followed by transportation at 0.57ppt, on the back of automobile price adjustments following the currency weakness and higher prices in transportation services. The decline in oil prices, on the other hand, limited the inflationary pressures in this group.

- The food sector was once again another big contributor to the headline figure, adding 0.51ppt. Monthly inflation in this sector, however, remained below the level in the same month of 2024 thanks to the price drop in fresh fruits and vegetables. The benign food inflation contributed to a lower-than-expected April reading.

- Finally, clothing pulled the headline up by 0.37ppt. However, annual inflation in this group has remained low at 16.9%.

- Consequently, goods inflation inched up to 30.8% YoY, while core goods inflation – considered a better indicator of the trend – stood at 20.3% YoY.

- Services inflation, which is less affected by currency fluctuations but more influenced by domestic demand and minimum wage increases, continued to decline. It dropped to 54.6% YoY, marking the lowest level since summer 2022 thanks to further easing in rents.

Annual inflation in expenditure groups

Overall, in the absence of any further exchange rate shock, large wage adjustments, unexpected hikes in administered prices and a jump in commodity prices during the remainder of this year, we continue to expect inflation below 30.0%. While the deterioration in the inflation expectations is relatively contained after the March volatility, the CBT has prioritised financial stability after large reserve depletion. It has also announced:

- An across-the-board 200bp hike in FX reserve requirement ratios (withdrawing more than US$7bn from the banking system).

- Increased surrender requirements for exporters from 25% to 35% temporarily until end-July (with an additional c.$2.0-2.5bn support for the CBT reserves).

- The introduction of a higher monthly conversion target of 0.3 points for TRY deposit share of corporates for banks (having a share below 60%).

- A slight increase in the remuneration rate for banks.

- A higher preferential rate for corporates’ FX sales under surrender requirements.

- A higher reserve requirement rate for funds derived from FX repo transactions with residents of a maturity up to one year. These moves aim to encourage a switch from FX to TRY and start rebuilding FX reserves as evolution of reserves, in addition to inflation prints and residents’ portfolio choice, will be key for the appetite of Turkish assets.

The CBT will release its inflation report on 22 May, ahead of the 19 June MPC meeting. While the report will offer further insights into the CBT’s outlook and hint at future policy directions, we might see a slight upward revision in its inflation forecasts due to recent developments since the first report.

While the CBT currently funds banks mainly from the upper band and keeps the ON rate close to 49%, a change in funding composition towards 1-week repo auctions and the consequent fall in the effective funding rate towards the policy rate will provide evidence related to the timing of rate cuts.

Conditional on market stability and the return of reserve accumulation, we do not rule out a June rate cut given the ex-post policy rate at around 8ppt (compared with the policy rate) and 11ppt (if the current cost of funding is considered), while the gap will expand further with the decline in annual inflation.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap