Soft US PPI and rising jobless claims keeps rate cuts on track

US weekly jobless claims rose substantially more then expected while PPI undershot by a significant margin, reinforcing the argument that the Fed will likely be in a position to start making monetary policy slightly less restrictive before the end of the year. We still look for a September start point for rate cuts and expect them to cut more than once

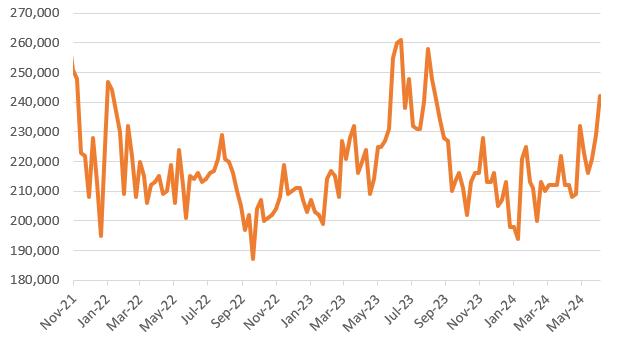

| 242,000 |

New initial jobless claims |

Rising jobless claims risks higher unemployment than the Fed is forecasting

It has been a topsy-turvy 24 hours for financial markets. Treasury yields plunged in the wake of the soft CPI report, but retraced a little as markets digested the more hawkish-than-anticipated Fed dot plot of projections for the Fed funds target rate. We are now back firmly in a lower yields situation following more soft US numbers this morning.

For starters we have a big increase in initial jobless claims of 242k versus the 225k consensus, up from 229k the previous week while continuing claims rose to 1820k (consensus 1795k and previous 1790k). These are the highest initial claims numbers since August last year and provide more evidence of a cooling labour market, which presents upside risk to the Fed’s assessment that unemployment will hold at 4% between now and year-end.

Weekly initial jobless claims

Soft PPI boost chances of a second consecutive 0.2% MoM core PCE deflator

At the same time the PPI report shows producer prices significantly undershooting expectations with headline PPI falling -0.2% month-on-month rather than rising 0.1% as expected while core PPI was flat on the month rather than rising 0.3% as expected. This makes it look even more likely we will get a second consecutive 0.2% MoM or below core PCE deflator – looking at the details medical care, airline fares, portfolio management fees and insurance look OK and these metrics feed through from PPI rather than from CPI, so we could be talking a potential 0.1% MoM for the May core PCE deflator.

While the Fed signalled yesterday it felt the most likely outcome was just one rate cut this year, Chair Powell acknowledged this is not a “plan” and they can “adjust” to the data flow. We believe they will end up having to do so. If we do indeed see more 0.2% MoM or below on core inflation prints, unemployment breaking above 4% and consumer spending cooling further that should give the Fed confidence to start moving monetary policy from "restrictive" territory to "slightly less restrictive" territory from September.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap