Soft March data strengthens case for Polish rate cut in May

The March data from industry and construction fell short of market expectations, indicating a more cautious approach from businesses in the face of elevated uncertainty about the global growth outlook. The labour market is less hot as well, with wage growth continuing to moderate. Altogether, the data adds to arguments for a rate cut in May

March data from industry and construction surprised to the downside

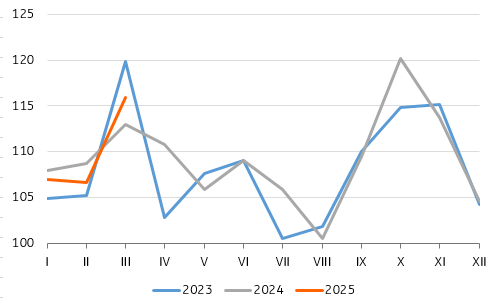

Despite a low reference base from last year, when activity in manufacturing was subdued ahead of Easter, industrial output turned out softer than expected, expanding by 2.5% year-on-year (ING: 4.5%; consensus: 3.7%). Still, many export-oriented manufacturers reported solid output growth, most likely reflecting stock building ahead of the tariff increase in the US, which could boost production in Europe.

The outlook for manufacturing remains uncertain due to a complete overhaul of US foreign trade policy. The March manufacturing PMI indicated some positive signs, such as an increase in new orders (including export orders) and stronger production. However, this could potentially be attributed to frontloading ahead of anticipated higher tariffs. In the 90-day window before the proposed high American tariffs come into effect, we may see various producers stockpiling inventories. Nonetheless, the looming threat of a potential trade war and disruptions in global supply chains continues to cast a shadow over manufacturing in the medium term. Past experience shows that the confidence channel is quite strong when it comes to the risk of tariffs.

Disappointing annual growth in industrial production despite low reference base

Industrial ouput, 2021=100, NSA

Construction output was also much weaker than projected, shrinking by 1.1% YoY (ING: +10.5%; consensus: +5.7%) last month. The data brought mixed signals in terms of the start of the public investment cycle. The main negative impact came from civil engineering, which fell by 4.9% YoY after some encouraging signs in January and February, and in 4Q24. The poor reading, despite favourable weather conditions, suggests that funds from the EU (cohesion and RRF funds) are being disbursed slowly to the final beneficiaries. The second sub-sector that reflects the public investment cycle, special construction works, has been growing since the beginning of the year. Overall, we think the construction sector should benefit from the public investment cycle in the coming months.

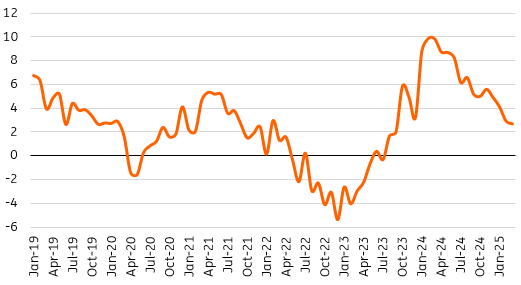

Wage growth continues to slow down

Labour market data points to easing wage pressures as employment continues to decline. Growth of average wage and salary in enterprises slowed to 7.7% YoY (ING: 7.5%; consensus: 7.7%) from 7.9% YoY in February, matching market expectations. With CPI inflation at 4.9% YoY, real wage growth slowed to 2.7% YoY. At the same time, the decline in employment maintained its pace at 0.9% YoY in March (ING: -0.8%; consensus: -0.9%). The number of posts declined by 8,000 from February, compared to a drop of 10,000 in March 2024.

Wage growth easing further

Real wage growth in enterprises, %YoY

Call for NBP rate cut in May even stronger

March figures from the real economy indicate that, irrespective of the final form of future trade policies and tariff levels, the heightened uncertainty regarding the global economy's condition over the medium term may dampen business and household confidence, potentially leading to lower investment and consumption growth. Although domestic demand is still anticipated to be the primary driver of economic growth in Poland this year, we have downgraded our 2025 GDP growth forecast from 3.5% to 3.2% and foresee increasing downside risks for economic growth above 3% next year as well.

Risks to GDP growth are skewed to the downside, with wage growth continuing to slow. Core inflation in the first quarter of 2025 was lower than the National Bank of Poland had anticipated in its March economic projection. Also, the dollar exchange rate is weaker, and crude oil prices remain relatively low. This combination of factors should be sufficient for the Monetary Policy Council to cut rates as early as May.

In our view, the key unknown is the scale of monetary easing, as policymakers will likely debate whether to implement a 25bp or 50bp cut. We believe there are arguments for a more decisive adjustment in the policy rate, especially if headline inflation moderates below 4.5% YoY in April. By the end of the year, NBP rates could be eased by 125bp.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap