Sliding sentiment adds to US growth concerns

Households were expecting President Trump to lead with tax cuts and deregulation, but instead we have austerity and the prospect of significant trade tariffs. This is prompting anxiety about household finances and job prospects with the concern being this translates into weaker spending

Households are worried about price rises and government job cuts

The Conference Board measure of consumer confidence has dropped to 92.9 in March from 98.3 in February, below the 94.0 consensus figure and leaving the index at its weakest level for four years. The bigger concern is the near 10-point drop in consumer expectations, which leaves that index at a 12-year low. As recently as November confidence was on the rise thanks to strong growth, record high equity markets and a sense that President Donald Trump would cut taxes and deregulate the economy which would keep growth and the jobs market robust. However, he hasn’t focused on those areas and instead we are seeing growing anxiety over President Trump’s government austerity and trade tariff led policy thrust.

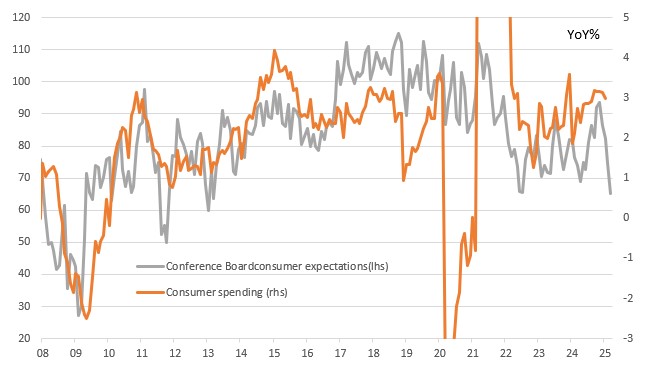

Federal Reserve Chair Powell has acknowledged the weakening confidence amongst households, but earlier this month he argued that “sentiment readings have not been a good predictor of consumption growth in recent years”. The chart below does indeed show the relationship isn’t perfect, but still hints at downside risks for consumer spending in coming months.

Consumer expectations suggests a spending slowdown is coming

Risks are skewed towards cooler spending growth

Government austerity and news headlines of government sector job losses and potential cuts to entitlements is prompting consumers to take a dimmer view of employment prospects and income expectations. Meanwhile, the prospect of significant tariffs is leading to worries about a loss of spending power and a lower quality of living. Recent declines in equity markets are also likely to have dampened the outlook for households.

While the outlook for growth is cooling, the economy is still adding jobs and the Fed remains wary of higher inflation from tariffs so there is little prospect of any imminent policy easing. However, we are closely following developments in the Cleveland Fed’s measure of new tenant rents that should translate into lower CPI housing inflation prints in late 2025, which will mitigate much of the inflation threat from tariffs. This should give the Fed the room for interest rate cuts in September and December with a third 25bp move in March next year.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap