Russian GDP forecast for 2021 upgraded on strong 9M21, but still cautious for 2022

Consumption was the key driver of the 2Q21 economic recovery and remains that in 3Q21, with August employment and retail trade above expectations ahead of the likely spike in September. We upgrade our 2021 GDP growth to 4.3%. Yet moderating lending, sluggish non-oil production, tight budget draft and Covid risks keep us at a cautious 2.0-2.5% for 2022

Consumption is relatively strong in 3Q21

August activity data is positive on the consumer side. Although retail trade growth of 5.3% year-on-year was below our expectations, it was still higher than consensus expectations and July's 5.1% YoY.

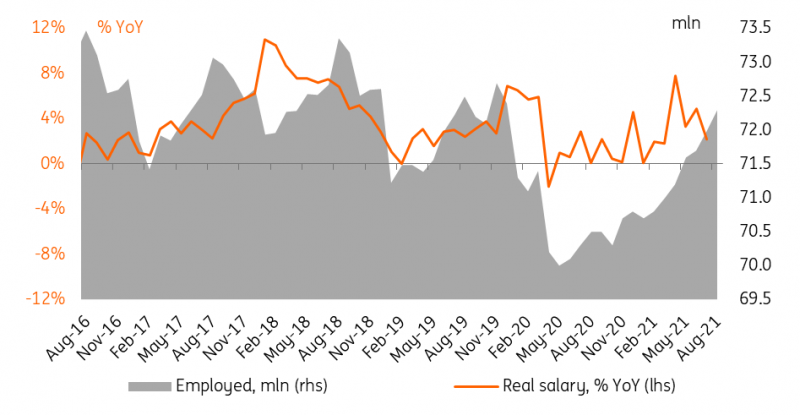

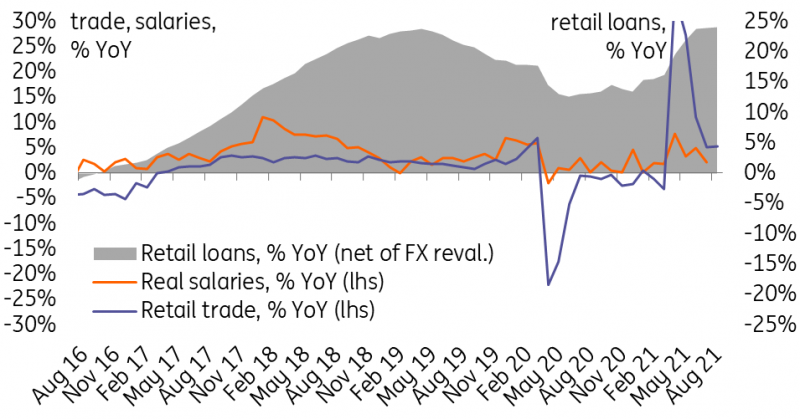

The fundamentals behind this growth were strong, with the employment number reaching a new high of 72.3 million people (the highest level since December 2010) and real wage growth remaining in positive territory (Figure 1). We attribute the underperformance vs our forecast of 6.5% to an acceleration in outward tourism, which does not suggest a weakening in the households' financial position. The banking sector indicators suggest stabilisation of both lending and deposit growth (Figure 2).

For September we expect a spike in the local consumption rate to the double-digit area thanks to the RUB700bn of additional social payments disbursed by the government in August-September ahead of the Parliamentary elections. This will be supportive of GDP growth, challenging our conservative 3.8% projections for this year. At the same time, strong consumption is contributing to the easier transmission of producer inflation into CPI that spiked to 7.3% YoY in September and is likely to support Bank of Russia's cautious approach to monetary policy.

Figure 1: Employment and real wages keep growing

Figure 2: Consumption and retail loan growth stabilised

Producer trend is less upbeat outside the oil and gas sector

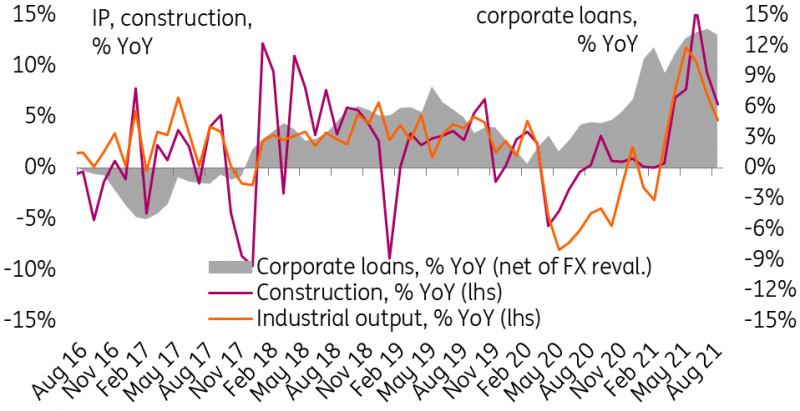

The producer side, on the other hand, is not as inspiring, with industrial production decelerating to a below consensus 4.7% YoY and construction growth to 6.2% YoY (also below consensus) amid stabilisation of corporate lending growth. The slowdown in industrial production took place despite the easing in OPEC+ restrictions to oil output and points to a cautious mood in manufacturing. The slowdown in construction is taking place amid the exhaustion of the subsidized mortgage programme and postponement of the sovereign fund-financed projects till 2022.

Figure 3: Producer activity keeps moderating

GDP growth in 2021 supported by strong consumption, but constraints for 2022 are significant

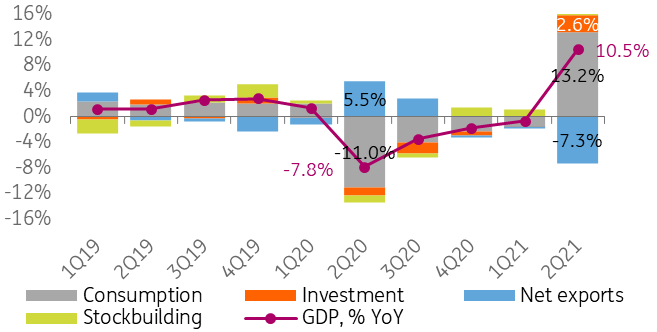

Looking at the structure of 1H21 GDP growth, which was also released last week, it appears that consumption was the key driver of the robust recovery and is likely to remain so in 3Q21. On another positive note, investment growth was also strong at 12.8% YoY, adding a noticeable 2.6 percentage points to 2Q21's GDP growth of 10.5% (Figure 4). Based on the data and newsflow for 9M21, we upgrade our GDP growth projections for this year from 3.8% to 4.3%, assuming 4.5% growth in 3Q21 and 3.0% in 4Q21.

At the same time, looking into 2022, our take is on the conservative side of the market consensus and the official projections. We see the following risk factors to growth in the medium term:

- Acceleration in CPI in 2021 to around 7% and a possible outperformance of the official 4.0-4.5% forecasts for 2022 are negative for income and may prevent the Bank of Russia from easing its approach to monetary policy.

- With unsecured lending reaching 10% GDP, a historical high for Russia, and the CBR taking steps in tightening the macroprudential framework, retail lending is unlikely to serve as a material support factor to consumption.

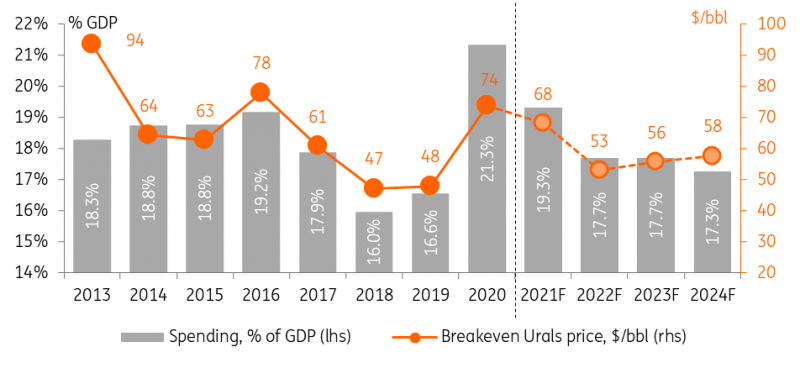

- The announced budget draft for 2022-24 suggests further tightening in fiscal spending and a decline in the budget breakeven oil price (Figure 5). In addition, the recent proposal to raise the required threshold for the liquid FX portion of the sovereign fund from the current 7% to 10% of GDP suggests that any local investments from the National Wealth Fund other than the currently discussed US$12bn per year (0.6% GDP per year) into general infrastructure and Gazprom's projects are unlikely.

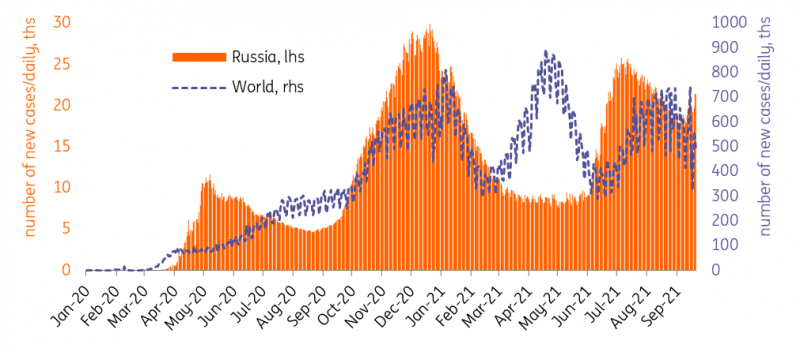

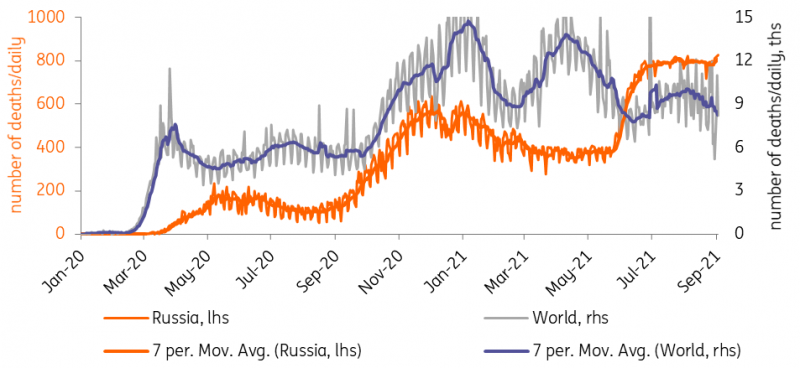

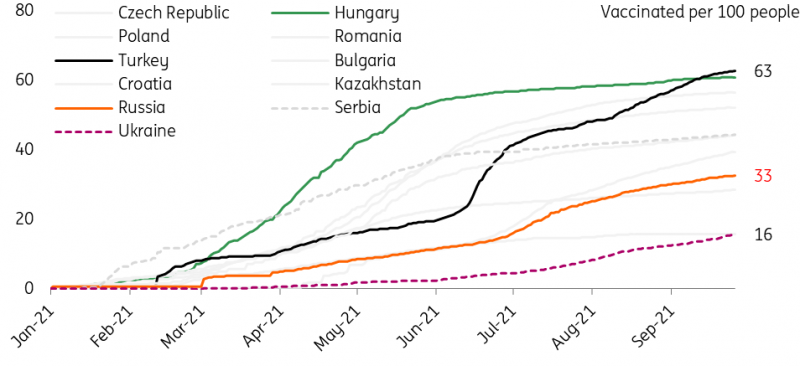

- Covid-related lockdowns, though not a base case, should also be considered as a risk. Currently, Russia is facing a new wave of Covid-19 infections (Figure 6), characterized by a historical high mortality (Figure 7), while the vaccination rate is at a sluggish 33%, despite the availablity of vaccines for the Russian citizens. In this environment the government may come to a situation when it will need to tighten the vaccination requirement or reintroduce some form of mobility restrictions. The potential negative effect on the GDP growth in the case of lockdowns is likely to be much smaller than at the start of the pandemic (1% of annual GDP per each month of strict lockdown), but still non-negligible.

Figure 4: GDP recovery in 2Q21 assured predominantly by consumption, but investment recovery was also noticeable

Figure 5: Budget draft for 2022-24 appears tight

Figure 6: Russia is facing a new wave of Covid infections...

Figure 7: ... amid high mortality...

Figure 8: ... and low vaccination rate

Based on the strong 1H21 and 3Q21 GDP performance we upgrade our 2021 expectations from 3.8% to 4.3%, however the moderation in lending, relatively tight signal from the monetary and budget policy, as well as Covid-related risks keep us at a cautious 2.0-2.5% expectation range for 2022.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap