Russian CPI slows in April, but no further relief seen till year-end

Russian CPI slowed by 0.3 ppt to 5.5% YoY in April and is likely to remain around that level until November-December, when the high base effect will become strong enough to overcome the persistent upward price pressures that are still present in the key consumer segments. Bank of Russia is likely to keep tightening at the coming meetings

| 5.5% |

April CPI, % YoYdown from March's 5.8% |

| As expected | |

Inflation off its peak, but not out of the woods

The April CPI result of 5.5% year-on-year is in line with our forecast (consensus was split between 5.5% and 5.6%) and points at a deceleration from the March peak of 5.8% YoY, however, we are not in a rush to take the numbers as a sign of sustainable relief.

- Higher base effect (in April 2020 the YoY CPI rate jumped 0.6 percentage points vs. March reacting to the pandemic/lockdown shock) is the sole factor of this slowdown.

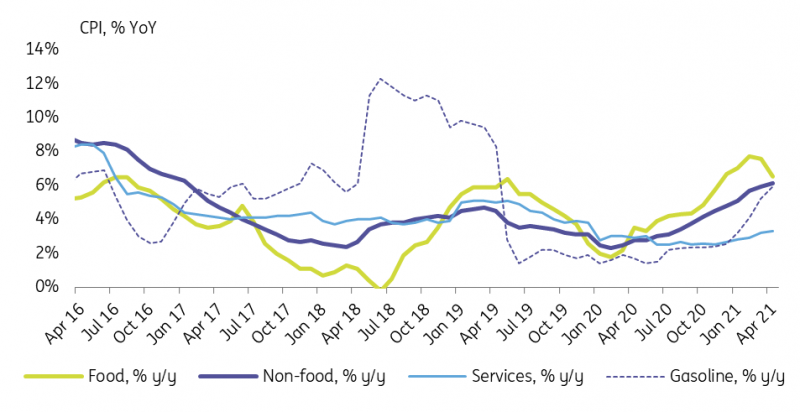

- Food segment was the only one to show deceleration (Figure 1), and even within it only volatile fruits and vegetables, as well as cereals and beans showed a noticeable slowdown, while the remaining major food groups, such as bread, meat, fish, dairy, and sugar kept showing price growth rates close to that of the previous month.

- Non-food products and services failed to take advantage of the higher base effect and kept posting higher annual growth rates (Figure 1), and their contribution to the overall CPI growth increased from 3.0 ppt in March to 3.1 ppt in April (Figure 2), according to our estimates. The key drivers in this acceleration were gasoline (which is now up 5.9% YoY, higher than the overall CPI growth, despite the government's measures), construction materials, reflecting housing and home improvement boom, and various services including medicine, local recreation, and insurance.

Figure 1: Inflation eased only in the food segment and only thanks to high base effect, in other segments prices keep accelerating

Figure 2: Upward price pressure in non-food products and services is gaining weight, which is important for CBR

Inflationary risks going forward include global agro inflation, local PPI, and elevated household expectations

For the coming months we expect inflationary pressure to remain elevated for several reasons.

- First, the global agriculture prices (Figure 3) remain a risk factor, with wheat, sugar and sunflower oil back in high double- digit growth on a combination of strong demand and supply concerns. Should the global price growth continue, it should prevent local food prices from showing disinflation.

- Second, the elevated PPI and corporate inflationary expectations (Figure 4) are another risk factor for the local consumer prices, especially given that last year's corporate profits were down 24% YoY according to Russian accounting standards, suggesting limited room for the producers to absorb input price growth in all the key consumer segments.

- Third, the local CPI does not yet fully reflect services in the Covid-affected areas, such as foreign tourism, given the still persistent restrictions for travel to Russians' most popular resort destinationas such as Turkey and Egypt (the latter is expected to be reopened for charter flights in May). Potential reopening of those may somewhat ease the local consumption pressure on prices but is unlikely to ease the overall inflationary risks for the consumers.

- Finally, the elevated CPI expectations by the households (Figure 5), propelled by actual price growth in socially-sensitive items as well as high government and media attention, are also a risk factor, which may prevent disinflation in the coming months.

Figure 3: Global food prices remain a risk

Figure 4: Local PPI and corporate pricing expectations keep edging higher

Figure 5: Households' inflationary expectations are also elevated, keeping CBR on its toes

CPI to stay around 5.5% YoY till November, year-end forecast of 4.5% at risk

The April CPI reading and its composition suggest elevated CPI risks in the near term. We would not exclude some minor uptick in May, followed by CPI staying around 5.5% YoY until November, despite the favourable base effect. Only at the year-end the higher base effect should be strong enough to assure annual inflation falling to 4.5% YoY in December and potentially to 4.0% in 1Q22. At the same time, we acknowledge that given the risk profile those expectations look optimistic.

The pace and structure of the CPI growth, with higher contribution of non-food and services CPI, amid acceleration of retail lending and slowdown in retail deposit growth, should keep the Bank of Russia concerned with the monetary component of inflation. We reiterate our call that the key rate, currently at 5.0%, has a 50 basis point upside this year, which may be realised in the next 2-3 board meetings.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap